The FSA Spy market buzz – 9 May 2025

Invesco gets contrarian; Popes and the S&P 500 performance; Jim Cramer’s certainty; Negative yields; AI is everywhere; Natixis considers the next decade; Google’s search woes and much more.

“Both funds have significant flexibility so they are not predetermined to underperform or outperform in any given market environment; instead returns are really driven by their respective managers’ decisions and actions,” said Dobrescu.

“Interestingly, both funds underperformed in last year’s covid-19 driven sell-off,” she said.

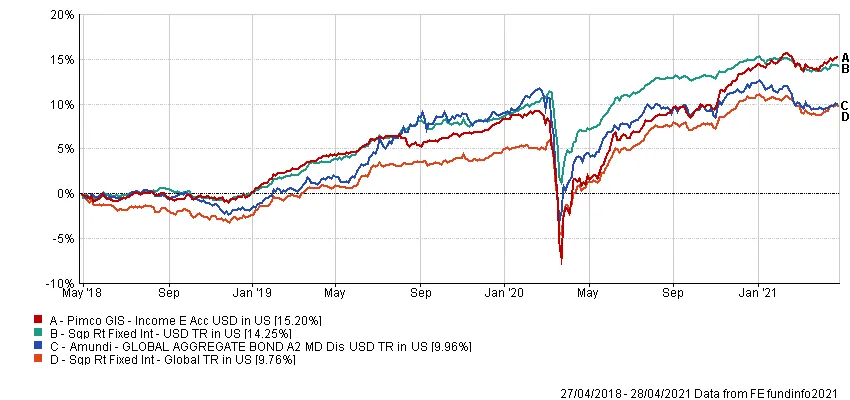

However, the Pimco fund has recovered to a larger extent since then, and is up 0.71% compared with a -2.42% decline by the Amundi fund.

The Pimco’s longer-term performance is also among the category’s best, and with modest volatility.

It has generated a 15.20% three-year cumulative return, outperforming the Amundi product (9.96%, which is more or less the same as its global fixed income sector average and its US fixed income fund peers (14.25%), according to FE Fundinfo.

“The Pimco strategy has been as or more resilient in other times of stress, too, such as late 2011 and the summer of 2013. And with a comparatively modest high-yield stake, it sailed through the fourth-quarter 2018 sell-off with top-quartile returns,” said Dobrescu.

The Amundi fund suffered especially during 2018’s market dip.

In addition to modest losses in the foreign-exchange sleeve, it was hurt from exposure to Petrobras and Pemex in the second quarter, as well as from a roughly one percent exposure to Argentina (which the team subsequently reduced).

However, in 2019’s credit rebound, Amundi did better than Pimco, thanks to its overweight to financials, as well as to its long exposure to US duration.

Its sharp drawdown in 2020’s sell-off was largely a result of its emerging markets currency exposure (particularly the Mexican peso) and to its overall higher credit sensitivity compared with the index, according to Dobrescu.

In fact, “the Amundi fund has historically been more volatile and has also experienced larger drawdowns than the Pimco strategy,” she said.

Dobrescu attributes this to a combination of factors: bigger bets on duration, foreign exchange and emerging markets, whereas the securitized debt that the PIMCO fund typically favours has been less volatile.

Discrete calendar year performance

| Fund / Benchmark |

YTD* |

2020 |

2019 |

2018 |

2017 |

2016 |

| Amundi |

-2.42% |

3.40% |

10.79% |

-2.02% |

6.20% |

1.25% |

| Bloomberg Barclays Global Aggregate |

-3.03% |

9.20% |

6.84% |

-1.20% |

7.39% |

2.09% |

| Pimco |

0.71% |

5.66% |

8.11% |

-0.66% |

6.39% |

7.36% |

| Bloomberg Barclays US Aggregate |

-2.65% |

7.51% |

8.72% |

0.01% |

3.54% |

2.65% |

Conditions in the high yield market

Conditions in the high yield market

Despite headwinds, ESG continues to perform

Despite headwinds, ESG continues to perform

Tap into Japan’s post-pandemic growth trends

Tap into Japan’s post-pandemic growth trends

Thematic investment series: Innovative transformation cuts across “old” and “new” economy companies

Thematic investment series: Innovative transformation cuts across “old” and “new” economy companies

M&G Episode Macro shines after tough year

M&G Episode Macro shines after tough year

Accessing Asian 5G innovation: three key portfolio themes

Accessing Asian 5G innovation: three key portfolio themes

Nuveen broadens income sources via private capital and real assets

Nuveen broadens income sources via private capital and real assets

The future of mobility

The future of mobility

Taking a thematic approach to harness disruption

Taking a thematic approach to harness disruption

Invesco gets contrarian; Popes and the S&P 500 performance; Jim Cramer’s certainty; Negative yields; AI is everywhere; Natixis considers the next decade; Google’s search woes and much more.

Part of the Mark Allen Group.