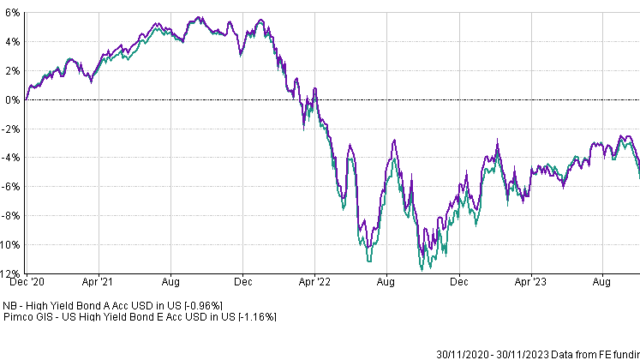

Fixed income was pounded during 2022 and higher US Treasury yields have translated into under/whelming returns in 2023. But US high yield has been a relatively positive part of the asset class. Short duration and high yields have translated into positive returns during the past year compared with mostly negative returns across the global fixed income universe, according to Isaac Poole, global chief financial officer, Oreana Financial Portfolio Advisory.

Oreana Financial thinks that high yield could come under some pressure in 2024 as lower quality credits are forced to refinance at materially higher yield levels. Against that backdrop, FSA asked Poole to consider US high yield bond strategies, and he chose the Neuberger Berman High Yield Bond fund and the PIMCO GIS High Yield Bond fund.

| Neuberger Berman | PIMCO | |

| Size | $2.12bn | $1.76bn |

| Inception | 2010 | 2006 |

| Managers | Joe Lind, Chris Kocinski | Andrew Jessop, Sonali Pier |

| Three-year cumulative return | -0.96% | -1.16% |

| Three-year annualised return | -0.91% | -0.99% |

| Three-year annualised alpha | 2.17 | 2.07 |

| Three-year annualised volatility | 7.14% | 7.06% |

| Three-year information ratio | 0.71 | 0.71 |

| FE Crown fund rating | ** | *** |

| OCF (retail share class) | 1.31% | 1.45% |

Investment Approach

The PIMCO strategy focuses on fundamental bond analysis and tilts toward higher rated credit quality. The investment universe is reflected by the benchmark ICE Bank of America Merrill Lynch US High Yield Constrained Index.

The bond-picking approach is supported by a broad analyst pool. While the focus is on US high yield, the managers are able to use non-US and other securities where they find attractive opportunities, for example, bank loans. The portfolio traditionally has had a focus on noncyclical industries that can provide downside protection during downturns.

The team tends to hold some liquidity in cash or government debt, which supports the fund’s ability to take advantage of market dislocations and add alpha by doing so. The portfolio can hold lower quality debt – below B rating – but the clear fundamental focus on resilient industries reduces the risk while supporting returns.

The Neuberger strategy is a value driven approach with a clear focus on credit selection. There is a strong tilt towards protecting to the downside, and the fund tends to invest in BB and B rated bonds.

The fund can still opportunistically add lower rated credit, although the focus on downside protection means the funds tends to avoid distressed credits. The portfolio can also invest in senior secured bank loans but tends to avoid non-US debt.

The portfolio can be riskier than the benchmark ICE Bank of America US High Yield Constrained Index but the combination of a top-down view with fundamental security analysis results in a disciplined, repeatable process.

The strategy has focused on sectors with strong pricing power and has also added some higher credit quality names through 2022 to help manage downside risk.

Both the PIMCO and the Neuberger funds have a clear, repeatable process that is reflected in their respective portfolios. The focus on fundamental analysis is critical in managing high yield portfolios, and both strategies do this very well.

The focus on downside protection in Neuberger has help during downturns, and although PIMCO has tended to participate more in the credit rallies, it also improved its downside protection in recent years. Both funds stand out in terms of their process and ability to repeatably deliver on investor expectations.

Fund characteristics

Sector overweights:

| Neuberger Berman | PIMCO |

| Gas distribution | Aerospace / defence |

| Sovereigns | Lodging |

| Real estate / homebuilders / building materials | Healthcare |

| Aerospace / defence | Packaging |

| Capital goods | Media cable |

Top five holdings:

| Neuberger Berman | PIMCO | ||

| Ford Motor Credit | 2.0% | Medline Industries | 0.8% |

| TransDigm | 1.9% | American Airlines | 0.7% |

| Charter Communications | 1.8% | Imperial Dade | 0.6% |

| American Airlines | 1.7% | Intelsat Jackson | 0.5% |

| Carnival | 1.5% | Venture Global | 0.5% |

Performance

The PIMCO strategy has a long history of solid performance, consistently sitting among the top quartile of its peers. The strategy has tended to do well during credit rallies, and increasingly has been risk managed to provide some protection during selloffs. Credit selection and the focus on noncyclical industries have helped improve the downside capture profile. While the fund suffered from the pain felt across the asset class in 2022, it has performed reasonably well through 2023.

The downside protection of the Neuberger fund as a focus has helped the strategy during credit selloffs, although 2022 was a challenging year as the fund lengthened duration as the Fed starting hiking rates. Even so, the credit quality held up and the portfolio did not experience any defaults, although they did participate in the asset class sell off. The portfolio is 2.82% higher year to date.

In general, the asset class has performed relatively well compared with the broader fixed income universe in recent years. Neuberger modestly outperformed PIMCO in 2022, but PIMCO has recovered some of that in 2023. This is in line with the focus on downside protection from Neuberger and PIMCO’s tendency to participate in upside outcomes. PIMCO has been more volatile on average than Neuberger.

Overall, the performance of both funds is in line with expectations given the processes they follow.

Discrete calendar year performance

| YTD* | 2022 | 2021 | 2020 | 2019 | |

| Neuberger Berman | 7.17% | -12.40% | 3.85% | 4.55% | 13.19% |

| PIMCO | 8.91% | -13.04% | 3.50% | 4.42% | 13.85% |

Manager Review

The previous leader of the PIMCO strategy, Andrew Jessop, retired in mid-2023, and the portfolio has been taken over by Sonali Pier, assisted by David Forgash. Both are experienced investors and will continue the focus on fundamental driven bond selection, and are supported by around 50 analysts.

Joe Lind and Chris Kocinski have been leading the Neuberger strategy since 2018 and 2019 respectively. Both are very experienced high yield investors and are supported by a stable, experienced team of around 25 research analysts and traders.

Indeed, both strategies have very experienced managers and are supported by a impressive analyst pools. The managers are committed to their respective investment processes. There has been some turnover at both funds from a lead manager perspective, but so far there doesn’t appear to be any indication that those personnel changes will impact the investment outcomes.

Fees

The fee for the Neuberger fund is lower at 1.31%, compared with 1.45% charged by the PIMCO fund.

Conclusion

Both funds have a clear process and are underpinned by a robust fundamental analysis and credit selection process. They have also performed reasonably well this year, delivering positive returns, albeit with PIMCO slightly edging Neuberger in terms of year-to-date performance.

Poole thinks either of these funds would be a good core exposure for investors looking to invest in US high yield. However, he believes that the near-term economic risk is skewed to the downside and high yield spreads may not be adequately compensating investors for that risk.

In that case, investors may want to consider underweighting any exposure to the asset class. Neuberger’s focus on downside protection could provide an edge– but for buy and hold investors, PIMCO could provide access to more upside after a recession plays out.