Asian high yield has endured a difficult few years to put it mildly due to macro headwinds and idiosyncratic risks in China’s property sector. After a brief rally during the first quarter this year, high yield continued its downward trend during the second quarter.

The consensus among asset allocators at the moment is that spreads for high yield do not sufficiently compensate investors for the recession risk, which both the yield curve and money supply are hinting is likely to materialise.

The ICE BofA US High Yield Index Option-Adjusted Spread was last quoted at 3.85% versus 10.87%, for example, when the coronavirus crisis first hit in March 2020.

There is also the spectre of China’s property sector, which continues to be plagued by difficulties, most recently with Country Garden, historically viewed as one of the more stable developers, which skipped a coupon payment on its offshore bonds.

Most high yield fund managers, who are typically able to allocate between 20% and 30% of net assets outside their core mandates, have responded by allocating more to investment grade, where the default risk is much lower.

Notwithstanding these difficulties, there are some green shoots in the asset class. One of the most notable trends in the past few years has been the extent to which China real estate’s weighting in the index has fallen considerably.

High-yield fund managers point to opportunities in Macau gaming, India renewables and Indonesian corporates among other areas.

High-yield fund managers also point out that the fundamentals for issuers are a lot more attractive than they have been in previous cycle as many of them took advantage of the abundance of liquidity following the coronavirus crisis to lock in funding at reasonable yields, while extending maturities at the same time.

Against this background, Isaac Poole, chief investment officer at Oreana Financial Services, selected the Fidelity Funds – Asian High Yield Fund and the Pimco GIS Asia High Yield Bond Fund for this week’s head to head.

| Fidelity | Pimco | |

| Size | $1.78bn | $2.59bn |

| Inception | 2007 | 2020 |

| Managers | Peter Khan, Tae Ho Ryu, Terrence Pang | Stephen Chang, Abhijeet Neogy, Mohit Mittal |

| Three-year cumulative return | -13.95% | -10.05% |

| Three-year annualised return | -13.41% | -9.43% |

| Three-year annualised alpha | 3.98 | 3.56 |

| Three-year annualised volatility | 16.35 | 11.98 |

| Three-year information ratio | -0.62 | -0.37 |

| FE Crown fund rating | * | * |

| OCF (retail share class) | 1.39% | 1.55% |

Investment approach

The Fidelity fund relies on bottom-up credit selection to search for hard currency assets that provide good income.

“Fidelity is able to access a deep capability from within the broader Fidelity group, which provides an impressive top-down view and has in the past taken concentrated positions. This can result in significant alpha but does open the strategy up to drawdown, such as was the case with a bet on China property,” said Poole.

Poole also notes that the Fidelity fund has been reducing its overall risk over the past year including increasing its exposure to investment grade credit and Indonesia, Japan and Korea on the one hand and reducing its exposure to China real estate on the other hand.

Regarding the Pimco fund, Poole notes that the fund is “undeniably a Pimco approach”, as it combines both top-down macro and bottom-up credit analysis.

“This is also reflected in a much higher exposure to investment grade and non-Asia bonds for Pimco versus Fidelity. Importantly, both funds have a clear process and philosophy that is reflected in the portfolio positioning.”

isaac poole, oreana financial services

Poole also notes that the fund suffered due to its exposure to China real estate, although this was not to the same extent as many of its peers.

The fund is primarily invested in hard currency assets, while it relies on macro views to make decisions regarding geographic exposure and duration. It also often relies on independent credit rating and research capability to generate alpha.

Poole notes that both funds have clear and repeatable investment processes, although the Pimco fund has resulted in a better risk-return profile, albeit it is still negative over the past three years.

“This is also reflected in a much higher exposure to investment grade and non-Asia bonds for Pimco versus Fidelity. Importantly, both funds have a clear process and philosophy that is reflected in the portfolio positioning,” said Poole.

Fund characteristics

Sector allocation:

| Fidelity | Pimco | ||

| Banks & Brokers | 22.39% | Real Estate | 12.6% |

| Consumer Cyclical | 18.82% | Gaming | 12.4% |

| Sovereign | 14.67% | Banks | 8.3% |

| Property | 11.96% | Electric Utility | 6.8% |

| Utility | 9.6% | Financial Other | 6.6% |

| Cash | 6.54% | Metals & Mining | 5.3% |

| Industrial Other | 3.5% | Diversified Manufacturing | 2.8% |

| Basic Industry | 2.75% | Technology | 2.6% |

| Insurance | 2.44% | Metals & Mining: Coal | 2.2% |

| Energy | 2.07% | Transportation Services | 2% |

| Transportation | 1.51% | ||

| Technology | 1.5% | ||

| Communications | 1.1% | ||

| Other Financials | 0.54% | ||

| Consumer Non-Cyclical | 0.28% | ||

| Capital Goods | 0.01% |

Top 5 holdings:

| Fidelity | Weighting | Pimco | Weighting |

| Sands China | 4.94% | Standard Chartered | 2.2% |

| Industrial & Commercial Bank of China | 4.24% | Sands China | 2% |

| Wynn Macau | 3.49% | Periama Holdings | 2% |

| NWD Finance | 3.35% | NWD Finance | 1.7% |

| Huarong Finance | 3.17% | Melco Resorts Finance | 1.4% |

Performance

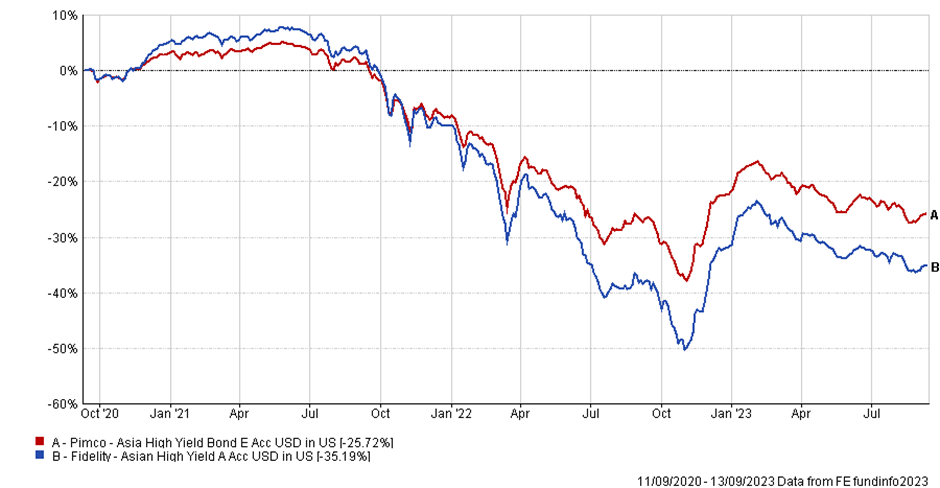

Unsurprisingly, given the performance of Asia high yield over the past three years, both funds have struggled.

Both 2021 and 2022 were difficult years for the Fidelity fund due to their overweight position to China real estate and some exposure to Sri Lankan government debt. Volatility was also heightened, partly as a result of the fund’s lower average credit rating, Poole notes.

“The recovery in late 2022 was solid though, although this has stumbled somewhat in early 2023. The fund’s concentrated sector bets leaves it open to significant alpha generation, but this also can add to risk within the portfolio,” said Poole.

The Pimco fund is only three years old and its genesis came at a difficult time for Asia high yield, although Poole notes that the fund managed to outperform many of its peers and the benchmark in 2021.

2022 was a different story due to the fund’s penchant for China property and Sri Lankan government debt, although Poole notes that this was at least partly mitigated by the fund’s views on duration.

“There has been no hiding for Asia HY over the past three years. Both funds suffered from Chinese property and Sri Lankan government debt,” said Poole.

“But Pimco did manage to blunt some of the pain by relying on its considerable macro capability and risk management through higher exposure to IG compared with Fidelity. Even so, volatility has been elevated and the overwhelming pain from negative beta has only marginally been offset.”

Discrete calendar year performance

| Fund | YTD* | 2022 | 2021 | 2020 | 2019 |

| Fidelity | -5.43% | -23.97% | -14.22% | 6.99% | 11.95% |

| Pimco | -4.9% | -14.81% | -11.12% | n/a | n/a |

Manager review

The Fidelity fund has been co-headed by Tae-Ho Ryu and Terrence Pang since July 2020 when the pair took over the previous head of Asia fixed income.

“Both are experienced investors, although this is their first time as lead managers. However, they are supported by a well-resourced Asia credit research team. The team has experienced more analyst turnover than is ideal over the past three years, but this has not deteriorated to capability in the team, particularly as senior members have been added to bolster risk management and bottom-up research,” said Poole.

Meanwhile, the Pimco fund has been led by Stephen Chang since it was formed alongside two co-managers Abhijeet Neogy and Mohit Mittal. Chang has 26 years’ experience including as head of Asian fixed income at JP Morgan.

The trio are supported by a 10-member Asia Pacific credit research team, although Poole notes that it has experienced high turnover over the past three years.

“There has been a lot of turnover in Asia HY it seems, but both funds are well supported by capable lead managers and an analyst pools,” said Poole.

“Stephen Chang at Pimco has a longer experience in markets and Asia fixed income, while Fidelity has two managers that are somewhat less experienced in lead roles. This does leave them with something to prove after taking over the fund recently and it has been a baptism of fire which they have so far navigated reasonably well.”

Conclusion

Overall, Poole notes that while the Pimco fund has an edge in terms of the experience of the managers, this is counterbalanced by the fact the Fidelity fund appeals to investors looking for concentrated bets that might later pay off.

Poole also notes that Pimco’s fees are relatively high, while Fidelity’s are close to the average for the asset class.

“That said, Asia HY is an asset class that is ripe for alpha and so fees can be expected to be somewhat higher,” he said.