After a tough start to the year, more fiscal stimulus and a looser monetary policy have brightened China’s prospects. Though numerous challenges remain, we believe Chinese equities offer attractive investment opportunities. China’s current slowdown, rising inflation and supply chain problems will likely mean near-term volatility for Asian markets, but this should not derail the structurally positive forces at work in many emerging market economies.

Currently, the biggest risk to Chinese growth is Beijing’s zero-Covid policy, which is offsetting the positive effects of cautious policy easing and supply chain disruption. Its property sector is another challenge. Developers’ liquidity problems are likely to further hamper homebuilding, but Beijing’s policy response has been swift and has included mortgage payment holidays and efforts to revive suspended projects and ease developers’ funding shortages.

China – More encouraging news flow

Since May, China has been fine-tuning its Covid containment measures, including reducing quarantine periods and responding with rapid, targeted lockdowns. A more effective booster campaign and effective vaccines are needed to allow China to exit its zero-Covid regime.

We expect the medium-term policy direction to be more pro-growth and pro-business. Beijing has announced measures to support the economy and has ammunition to do more.

The manufacturing sector is back in favour under China’s ‘dual circulation’ policy, which promotes high-value manufacturing and hard tech production while focusing on import substitution and technological self-sufficiency.

China’s commitment to both monetary and fiscal support should help growth to revive. We expect more easing aimed at sectors where the government has effective control. Such measures should

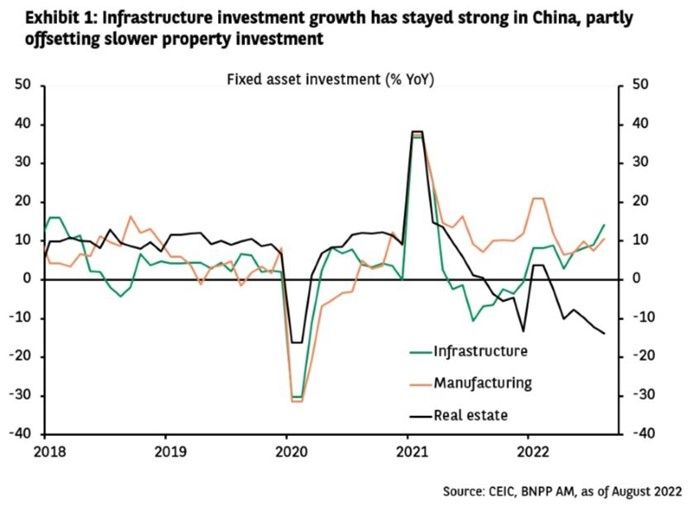

- Support construction and the property market

- Boost spending on, for example, bridges and roads, but also IT, artificial intelligence, data hubs, environmental projects, and electric vehicles (see Exhibit 1).

Equity market technicals are particularly favourable, in our view. Given the large valuation discount between Chinese and US equities, we believe long-term investors should capitalise on the recent market uncertainty to increase their exposure to China.

Our Greater China equities team is sticking with selected high-quality growth companies that have resilient fundamentals amid the macroeconomic downturn.

We favour companies with strong pricing power and are seeking long-term investment opportunities in sectors best positioned to benefit from structural changes:

- Technology & green innovation

- Consumption upgrading

- Industry consolidation.

Asia & EM – Domestic demand growth

We believe the growth path into 2023 will depend on the policies of individual governments on Covid control, market reopening, and responses to inflation.

China’s slowdown, rising inflationary pressures and supply chain disruptions will likely lead to near-term volatility in Asia. Yet these factors are more likely to dent than derail the structurally positive forces in many emerging market economies.

The key driver of Asia’s post-Covid recovery – external demand – is losing steam. Amid weaker global growth, it is crucial to focus more on domestic demand opportunities.

Within Asia, Asean markets (mainly Singapore and Thailand) have led the region’s economic reopening this year thanks to their higher Covid vaccination rates. Domestic mobility has started to normalise in Indonesia and the Philippines. South Korea and Japan recently announced further border openings.

On the back of the reopening tailwind, real imports are strongest in India and Asean. Moreover, healthier balance sheets and rising corporate confidence in India bode well for business investment.

Indonesia and the Philippines are more domestic demand-oriented by nature and are benefiting from a rise in consumption. Structural reforms in the Philippines should support private investment, providing an additional driver for domestic demand strength.

We believe the changes in consumer behaviour after Covid will prove structural over the long term, leading to a stronger emphasis on boosting domestic consumption and investment in some major Asian economies. Examples include China’s focus on consumption and quality growth, and India’s long-term strategic policy shift towards lifting domestic demand and productive capacity.

Attractive valuations in Asia and EM

Asian and EM equities have now priced in much of the weaker global conditions. Current earnings per share estimates for 2023 are above those for 2022. Modest valuations, light investor positioning and good fundamentals are buffers against near-term volatility.

Our long-term strategy for Asean post-Covid focuses on four major themes:

- Foreign direct investment growth

- Urbanisation

- Consumer upgrades

- E-commerce and digitalisation.

Our Asia & Global Emerging Markets team is selective and focused on structural trends, strong business models and high-quality companies with low debt that can generate sustainable returns with sound or improving environmental, social and governance profiles.

We expect to see more divergence in stock performance as the market focus gradually returns to fundamentals and sustainable growth.

Zhikai Chen is head of Asian and global emerging market equities and David Choa is head of Greater China equities at BNP Paribas Asset Management.