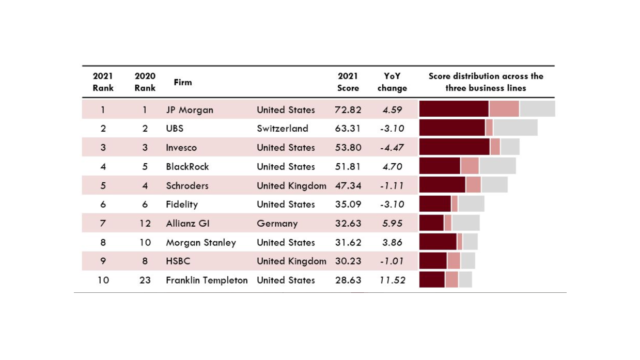

JP Morgan Asset Management (JPMAM) topped the overall rankings for the second successive year, scoring highly in all three categories (outbound, inbound and onshore) of China operations, and heading the list for outbound investment activity.

It has been a double victory for the US firm, with the Z-Ben recognition coming a few days after Broadridge Financial Solutions announced that it had clinched the top spot of its China rankings from UBS Asset Management.

In particular, JPMAM continued to expand its outbound footprint in 2020, launching two further mutual recognition of fund (MRF) products, as well as offerings through the qualified domestic institutional investor (QDII) and qualified domestic limited partner (QDLP) channels.

The second half of the year saw $12.72bn of QDII quota issued to foreign firms – exceeding the $10bn annual target that SAFE had planned. QDLP also received top ups, leading to market anticipation that broader outbound reforms may be on the horizon.

JPMAM came second behind Invesco for onshore activities, which include mainland presence through fund management companies and wholly foreign-owned entities (WFOEs), and third behind UBS (1st) and Blackrock (2nd) for inbound operations such as transactions through the stock connect and qualified foreign institutional investor (QFII) schemes.

Scores lower down the order have been increasing, but not at the same pace as the top ranks, so leaders continued to strengthen their positions, according to Z-Ben.

“Leading firms are active across both onshore and cross-border businesses, [and] it just became even tougher to break into the top tier,” the Shanghai-based China asset management consultants noted.

Shifting positions

Nevertheless, there were significant changes in the top 25.

New entrants include Amundi (21st), as it enjoyed onshore and offshore progress through setting up a wealth management venture and a wholly-foreign owned enterprise (WFOE), and Power Corporation of Canada (24th) which bolstered its onshore and inbound capabilities through expanding its WFOE.

Notable drop-outs from the top 25, were Winton as others closed the AUM gap and Manulife, which saw “relative inactivity”, according to Z-Ben.

The US share of the top 25’s scores increased from 42% in 2020 to 44% in 2021 as firms in the top ten made gains. France saw the largest growth of any country, to 5% from 2% of the total as it included a second firm (Amundi), in addition to BNP Paribas, in the top 25.

However, the share of the top 25 from Europe and Asia fell by two percentage points and one percentage point, respectively.

Z-Ben weights onshore activities highest, and Invesco Great Wall was a winner, increasing its AUM by 57% in 2020, to end the year at $58bn. The foreign partner has long taken a controlling role in the venture and continued to work to formalise this through an increase in its shareholding, noted Z-Ben.

Meanwhile, the first wholly-foreign-owned fund management applications were submitted – one of which, Blackrock’s, was approved. There was also a raft of new Sino-foreign joint ventures across both bank wealth management and advisory.

UBS again headed rivals for its inbound activities, enjoying significant growth in its Greater China fund suite, which ended 2020 with over $30bn in AUM. This rise also featured a major focus on onshore assets and has been driven by strong performance among its equity funds, according to Z-Ben.

Indeed, there was strong foreign portfolio investment in China securities in general last year.

Overseas holdings of onshore equities and bonds exceeded $1trn in 2020, and index inclusion and asset owner demand led to flows that were fixed income heavy, according to Z-Ben.

The top 10 foreign asset managers in China