Spy shared a much-needed beer with a high-net-worth private investor this week who happens to have built, and then subsequently sold about a decade ago, a decent sized asset management firm. He said to Spy, he has used his wealth to invest in almost anything but asset management for the last 10 years, but for the first time was now looking at the industry again with interest because “it has become interesting again”. Passive may have had all the running but the case for active had become more and more compelling. He even felt, rather surprisingly, that margins had reached an interim nadir. Spy will raise a glass to that.

Capital Group has added to its suite of ETFs, notes Spy, bringing its total ETF range to nine strategies. This time the American giant has added fixed income to the line-up, with the new funds all trading in New York. The firm has launched the Capital Group Short Duration Income ETF, the Capital Group Municipal Income ETF and the Capital Group US Multi-Sector Income ETF. These are all active strategies, not passive ones. “Now is a good time for financial professionals and investors alike to consider active fixed income ETFs,” said Mike Gitlin, head of fixed income for Capital Group. Spy would happily concur that active management of fixed income risk and opportunity, with rates all over the place, is not a bad idea at all.

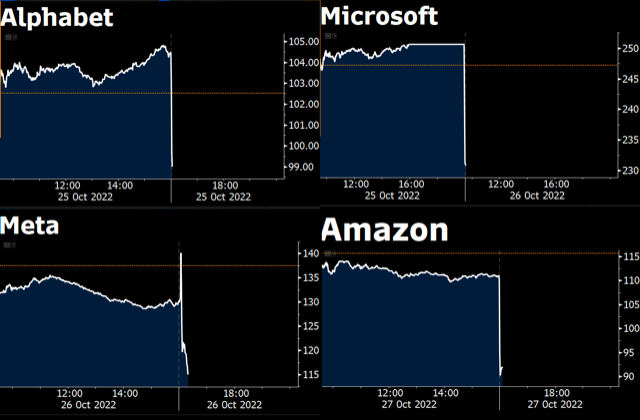

Spy is doing a whip around. Anyone got a spare few hundred bucks to give to poor Mark Zuckerberg. The Facebook tech titan has lost about $100bn of his net worth in this year’s rout and must be feeling a little light in his wallet. The FANGMAN stock complex lost another $270bn in market capitalisation yesterday after the Zuck’s Meta issued guidance on revenue that was, to put it mildly, disappointing. Meta has lost a quarter of its value, $90bn. Third quarter revenue growth for big tech looks a little ugly. Year on year, growth was only: Amazon +15%, Microsoft +11%, Apple +8%, Google +6%, Netflix +6% and at the back in the naughty corner, Meta / Facebook -4%. It was not all horrendous, Tesla grew 56% year-on-year. Still, a picture tells a thousand words; this was the market reaction.

Is it forward thinking wisdom or a rather desperate play by Hong Kong? The regulator has announced it wants to legalise retail crypto trading in the SAR and allow Hong Kong to become a crypto trading hub. With crypto having suffered a massive price wipe-out over the last 12 months and thinner trading volumes driven only by deeper-pocketed institutions, legalising the retail trade may not make that much difference. Licensing these trading platforms may bring some revenue to the regulator as they will need to pay fees, of course. Gary Tiu, an executive director at crypto firm BC Technology Group, was quoted as saying, “Introducing mandatory licensing in Hong Kong is just one of the important things regulators have to do. They can’t forever effectively close the needs of retail investors.” Does the retail investor have needs, or do the platforms need retail investors, wonders Spy?

What’s in a name? Quite a lot, especially when it comes to naming funds. Spy is watching an initiative by the Securities and Exchange Commission which is trying to crack down on misleading marketing by asset managers. The rule would require funds to prove that 80 per cent of their holdings match their fund names. This hardly seems controversial to Spy but you would think the SEC was asking fund managers to give up their firstborns, such is the pushback and lobbying against the proposed rule from the industry. There are some valid concerns, for example, the potential reallocation of a stock from one major index to another, growth to value perhaps, may force selling simultaneously causing dislocation, but these concerns could surely be dealt with by timing rules. The real issue is fund managers, finding spurious reasons for including utterly out of scope stocks in a strategy, in order to juice returns, by deliberately breaking their investment mandate. ESG is particularly rife with this problem.

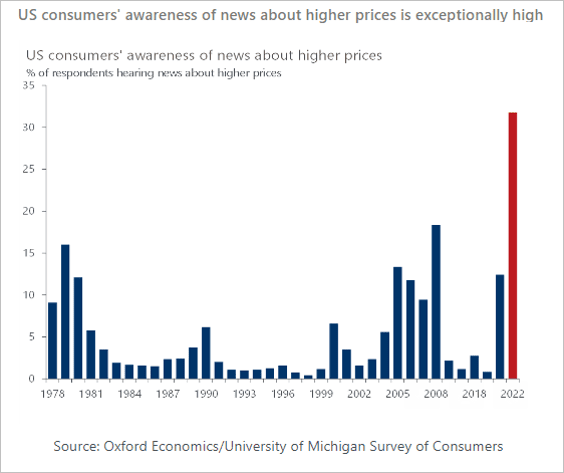

Spy is beginning to feel sorry for central bankers. Raising interest rates is doing close to nothing to stem inflation expectations. When consumers start to expect prices to go up and it becomes entrenched in their thinking, it is very, very hard to shift. From Chile to the United States, the EU to South Africa, Australia to southeast Asia and everywhere in between rates are rising but so are prices. Going back 44 years, American consumers have never been so aware of inflationary pressures according to an Oxford Economics / University of Michigan Survey. And that affects behaviour.

Is Credit Suisse the canary in the coal mine? The massive job cuts, 9,000 of them, announced by the bank may herald the start of job trimming across the industry. It is possible that big tech, fintech and start-up tech may all be entering a phase of “right-sizing”, too. Spy had the chance to chat to one recruiter this week, who said he had a “remarkable number” of CVs flowing across his desk at the moment.

Spy’s trusted band of photographers in Hong Kong have been out spotting trams with asset management advertising. First up is Capital Group promoting its fixed income capability. Those with eagle eyes will spot a Fund Selector Asia Award, nestled in the imagery too.

BNP Paribas is promoting an Asian sustainable cities bond.

Finally, First Sentier is continuing its campaign of listed property and infrastructure.