The FSA Spy market buzz – 6 June 2025

Animal spirits run wild; Franklin Templeton is taking credit; EM banking revolution; Not all luxury is equal; Death of search and the AI machine; George Soros on wins and much more.

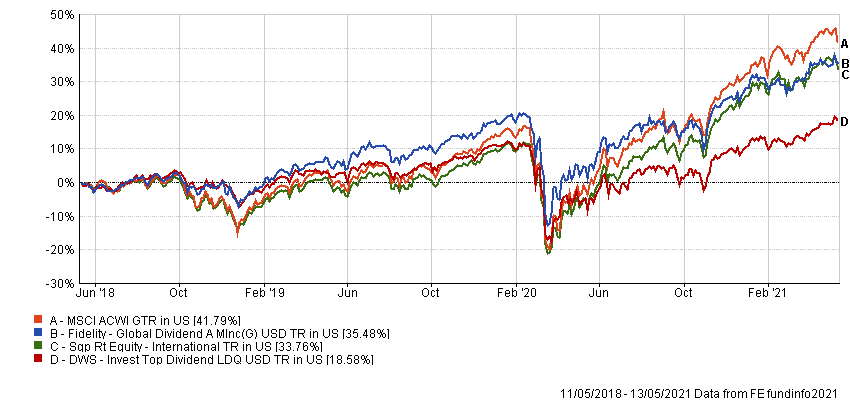

The DWS and Fidelity products are designed to outperform on the downside and will likely lag peers and the broader market during bull markets, when growth stocks or non-dividend paying companies outperform and when lower quality firms or smaller capitalisations are in vogue, according to Schumacher.

“Looking at the track records of the funds, they have demonstrated their ability to keep volatility in check and offer downside protection during periods of market stress,” he said.

Over the trailing five-year period ending April 2021, the standard deviation, measured in euro, clocks in at 10.3% for DWS and 10.4% for Fidelity, meaningfully below the peer average of 12.7% and the MSCI World Index’s 13.7%.

During this period, DWS captured only 73% of the losses the index suffered in down markets, while Fidelity did even slightly better with a downside capture ratio of 71%.

“Their quest for quality and robust companies made them thrive when markets shivered, for example during the fourth quarter correction in 2018, and more recently during the corona pandemic sell-off in the first quarter of 2020,” said Schumacher.

“Although both funds are known for their defensive strength, the portfolio of DWS at the end of April 2021 was more value conscious than Fidelity, which in turn offers a better-quality portfolio as evidenced by a higher ROE and lower debt/total capital ratio,” he said.

The differences in sector exposure, with notable allocations of DWS to reviving energy stocks and mining companies, helped it outperform Fidelity by 90 basis points in the year to date.

“The two funds do not differ much in terms of volatility profile, since they are keen to manage volatility and downside risks effectively,” said Schumacher. Longer term DWS has been less volatile than Fidelity, but Fidelity’s volatility has been lower over the short term.

A comparison of the rolling three-year volatility of returns since the inception of Fidelity Global Dividend in 2012, shows that DWS Top Dividend has achieved a lower standard deviation in 79% of those three-year periods.

“One of the drivers of DWS’ lower volatility was its allocation to mega caps, which has been consistently higher than Fidelity. These companies tend to be more resilient during periods of market volatility,” said Schumacher.

Another factor is the allocation to defensive sectors such as consumer defensive, healthcare and utilities, which was typically higher for DWS than for Fidelity. Finally, the cash buffer of DWS helped it to dampen volatility.

Although DWS’s volatility profile has been superior long term, Fidelity’s volatility has been a tad lower over the past three years, according to Schumacher.

“We have seen a gradual deterioration in the quality of the portfolio of DWS, with its ROE declining since 2015,” he said.

Thomas Schuessler, manager of the DWS portfolio, increased the exposure to cheaper names in the universe, which he found in more cyclical sectors. In contrast, Dan Roberts of Fidelity continued to emphasize the quality of his portfolio holdings, becoming more vigilant on financial leverage.

“This has helped the Fidelity fund to navigate better through more turbulent periods recently, including the coronavirus-driven market sell-off,” said Schumacher.

Discrete calendar year performance

| Fund/Sector |

YTD* |

2020 |

2019 |

2018 |

2017 |

2016 |

| DWS |

7.45% |

-0.63% |

16.80% |

-6.38% |

13.65% |

3.54% |

| Fidelity |

6.51% |

7.90% |

23.49% |

-4.81% |

16.24% |

1.14% |

| Equity – international | 6.52% |

14.89% |

24.01% |

-10.85% |

21.55% |

4.54% |

Unmasking the dividend opportunity

Unmasking the dividend opportunity

From “FAANG” to “MAMAA” to “Magnificent 7” – what’s in a name?

From “FAANG” to “MAMAA” to “Magnificent 7” – what’s in a name?

How can a sustainable approach also ensure you don’t compromise performance?

How can a sustainable approach also ensure you don’t compromise performance?

Fixed income – making ground in ESG as ETFs see rapid growth in AUM

Fixed income – making ground in ESG as ETFs see rapid growth in AUM

Investment Ideas for 2021: Explore the untapped potential in China Small Companies

Investment Ideas for 2021: Explore the untapped potential in China Small Companies

Healthcare’s innovation shifts into high gear

Healthcare’s innovation shifts into high gear

Taking a thematic approach to harness disruption

Taking a thematic approach to harness disruption

Accessing Asian 5G innovation: three key portfolio themes

Accessing Asian 5G innovation: three key portfolio themes

Appetite for thematic investments grows amid rates and inflation concerns

Appetite for thematic investments grows amid rates and inflation concerns

Who’s afraid of higher interest rates?

Who’s afraid of higher interest rates?

Animal spirits run wild; Franklin Templeton is taking credit; EM banking revolution; Not all luxury is equal; Death of search and the AI machine; George Soros on wins and much more.

Part of the Mark Allen Group.