The Japanese stock market may seem overbought as it approaches all-time highs, but any correction would be a good opportunity to buy the dip.

This is according to a research report by Swiss private bank Julius Baer, which argued that several factors are supportive of the long-term opportunity for Japanese stocks.

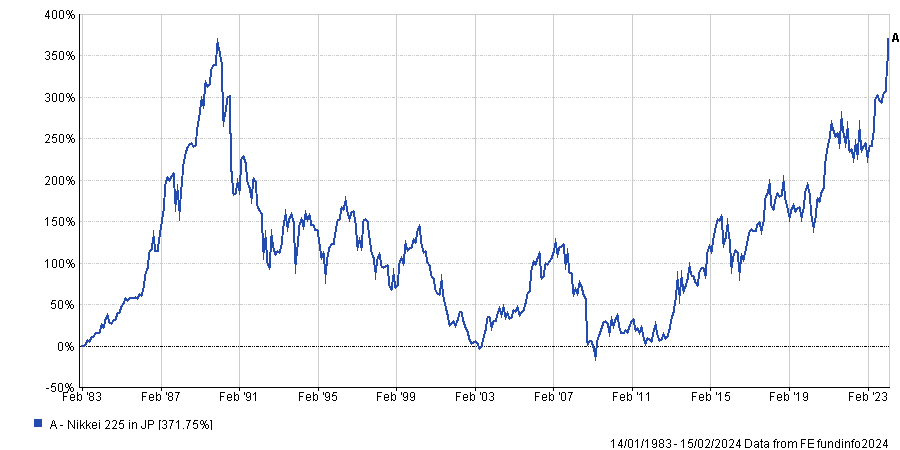

Inflows into Japanese funds have been increasing over the past year alongside the rise of its equity market. The Nikkei 225 is up 37.77% in local currency terms (about 24% in US dollar terms) over the past year, according to FE fundinfo data, and looks on track to breach its previous all-time high set in 1989.

Much of the recent rally in Japanese stocks has been driven by investor enthusiasm for the corporate governance reforms being pushed by the Tokyo Stock Exchange (TSE).

One of the latest initiatives has been the publication of a list of Japanese public companies that have disclosed information on implementing strategies to improve their cost of capital and valuations – to be refreshed monthly by the TSE.

“It is clear that the pressure is on for listed companies to conform,” a report from Julius Baer said. “This can be seen from the jump in the percentage of companies that have disclosed initiatives from 31% to 40%.”

“We expect that this will keep rising as the TSE piles on the pressure with a monthly refresh of this list.”

The bank flagged the many large cap stocks that have not disclosed initiatives already trading at greater than a 1x P/B ratio.

“While they are not in a hurry, we expect that the culture will eventually make all of these large caps unveil measures. This should prove positive for their share prices,” the report said.

Although the reforms have been a tailwind for all value stocks in Japan, the bank expects companies with “explicit disclosures” to gain more interest from investors.

Unwinding of cross-shareholdings a good sign

Another positive factor has been the genuine unwinding of crossholdings in Japanese companies. In the past, cross-shareholdings were a way Japanese companies shielded themselves from hostile takeovers and kept good relations with their business partners.

But these crossholdings are to blame for the slow pace of reform by Japanese companies, the report said.

The TSE in 2022 raised the minimum free-float share ratio required for a company to maintain its listing and cross-shareholdings were barred from being considered free-float shares.

The report said that the pressure from the TSE on cross-shareholdings seems to be succeeding.

“Nomura securities estimated that companies excluding financial institutions sold $47.8bn of publicly traded shares starting from 1 April 2023 through the second week of December 2023,” the report highlighted. “That is 45% more than the previous five-year average.”

The report also pointed to Toyota, Japan’s largest stock by market capitalisation, saying that it is “leading the charge”.

The car manufacturer reduced its multi-billion dollar stake in Denso, and Denso has also stated its intention to sell its shares in companies associated with Toyota.

“We think this unwinding of crossholdings will pick up speed,” the report said. “The pace will build up until a point where many companies have to unwind to prevent a selling effect.”

However, the report flagged some of the major risks to their bull-case on Japan. It suggested that any disorderly unwind of yield-curve-control and an exit of negative interest rate policy could upend markets and the country’s currency.

Central bank policy aside, if the yen strengthens excessively, its manufacturing companies will be negatively affected, the report said.

This is because, despite investment into diversified manufacturing outside of the country, Japan is still a major exporter at 75% local production.