Jason Pidcock, investment manager for Asian equity income and manager of the Jupiter Asian Income fund, has been increasing his exposure to Taiwan in recent months to such a degree that it now counts as the second largest country in terms of allocations for the fund.

On the face of it, this would not be too extraordinary for an Asian income fund except for the fact that Pidcock (pictured) is well-known for his top-down approach to stock selection with geopolitics featuring highly in his decision making.

Pidcock does not view this as contradictory however, noting that the risk of a conflagration in the Taiwan Strait is currently low and the pace of change in the technology industry because of the AI revolution means that now is the time to overweight the sector.

“So far this year, we don’t expect any severe political risk to hit Taiwan. What we’re getting in Taiwan is large-cap stocks that are world leaders and they’ve got extremely strong balance sheets; they’re all in a net cash position and they’re willing to share their profits with their owners, that is, pay dividends,” he said.

“They are large and liquid so if we changed our mind, we could get out, but we don’t actually think Taiwan is going to be at the forefront of geopolitical risks for 2024, or at the very least until the US election in November of this year.”

According to its most recent factsheet, the fund’s largest two holdings are Taiwanese companies: Mediatek, which is equivalent to 7.6% of net assets, and Taiwan Semiconductor Manufacturing, which counts for 6.9%. The fund also has Hon Hai Precision Industry in its top five holdings.

Regarding the changes to the technology sector, Pidcock takes the view that the world is on the cusp of the biggest replacement cycle ever seen as existing laptops, smartphones and other devices are rendered obsolete by AI. He began increasing his weighting to the sector, notably in January.

“We already thought after a cyclical dip last year, we would see an upturn in profits this year and then dividend increases would fly off the back of that. But because of AI, we now think over the next couple of years, the replacement cycle for tech will be the biggest the world has ever seen.”

Hedge inflation with gold

Pidcock’s other major trade in the last few months has been to increase his weighting towards Newmont Corporation, a gold mining company, as he takes the now slightly contrarian view that monetary policy is likely to be loose for quite some time.

“We think central banks are going be a little bit soft on inflation. Jerome Powell actually said 2% is a target they will reach over time. He doesn’t seem in any hurry to reach that target. What that means is if we do get a bit of an economic pick-up and inflation does remain sticky, we just do not think most major central banks around the world will be willing to countenance the idea of raising interest rates,” he said.

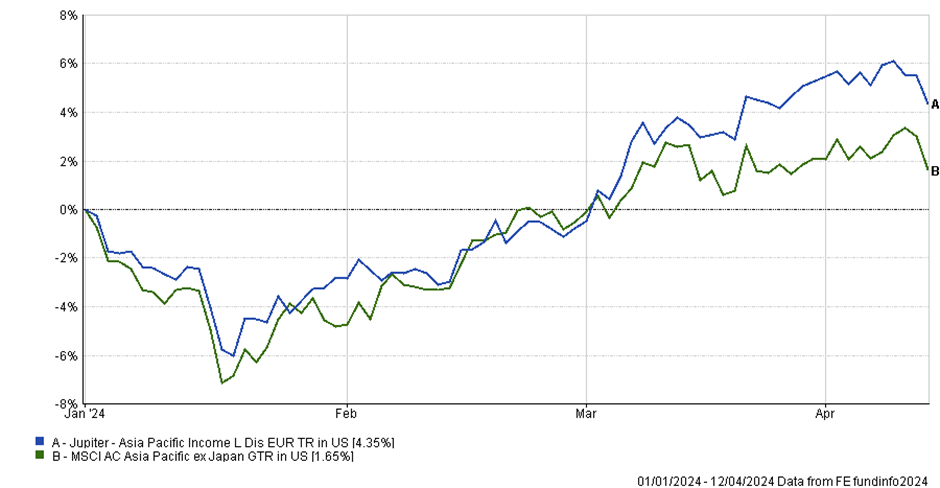

Unsurprisingly, overweighting technology and a gold mining company have been successful trades, which has allowed the fund to outperform the benchmark so far this year (see chart).

Old-fashioned

Pidcock is a self-described “old-fashioned” fund manager insofar as he has a laser focus on returns. The fund is a top quintile performer on a one-year, three-year and five-year basis, according to FE fundinfo.

The fund is not marketed as the greenest or most ESG-focused, although it does score fairly well based on most metrics, largely because corporate governance is an important component of its stock picking criteria, and the fund does not have any holdings in heavily polluting sectors such as cement, chemicals or steel.

Pidcock also notes that in 30 years investing in Asia he has never put on a currency hedge or used any derivatives. If he has a view that a currency is likely to be very weak, he will simply avoid that market, while the fund also skews towards hard currencies.

Overall, the fund is heavily concentrated, with holdings typically around 30 stocks. Cash rates vary between zero and 3% and the turnover of the portfolio is typically no more than 20%.

It is an income-focused fund, which means that any stocks need to have a dividend yield at least 20% more than the benchmark.

The fund focuses on large-cap stocks with a market cap of more than $3bn, although the vast majority of the portfolio have a market cap in excess of $10bn.

Australia overweight

Pidcock is also well-known for his bullish outlook on Australia, the fund’s largest weighting, which is unusual for an Asia-focused fund.

He is fond of citing the fact that Australia is one of the top two performing stock markets globally since 1990. It was the best performing stock market, he notes, until the fourth quarter of last year when a rally in the S&P 500 meant the US overtook it.

He also notes that the country has more favourable demographics than many emerging markets, noting crucially that a lot of immigrants to Australia are wealthy and therefore net contributors to the economy immediately.

Having been overweight India for a while, the fund now has a neutral stance as Pidcock believes that valuations have become stretched, particularly in the mid-cap space.

Defensive sector allocation

In terms of sectors, the fund is fairly defensively positioned, being overweight consumer staples and underweight consumer discretionary. He noted that that was largely a result of Covid-19, although as that became consensus, the trade has been slightly unwound.

Surprisingly, the fund has zero weighting towards healthcare currently, which Pidcock thinks is a result of the fact that top-line growth had not necessarily disguised some of the risks in the sector.

“People can look at the top-line story and say spending on healthcare keeps going up as a percentage of GDP so money will be spent in this sector. The trouble is there are risks within the sector,” he said.

“The risk to the pharmaceutical companies is that drugs become quicker to get cleared because AI helps prove their efficacy more quickly. And you can get small startups coming out with blockbuster drugs, a bit like the more orthodox tech sector, where in the 1990s, you suddenly had these guys in their bedrooms coming up with something that they could bring to the market much quicker than they could in the past and stealing market share away from the bigger players.”