Many of the top performing concentrated, bottom-up portfolio managers who have ignored factor tilt for the past decade have benefitted from an inherent growth style tilt, says T Rowe Price’s Peter Bates.

But after a decade-long period of growth stock outperformance, the best performing fund managers of the past decade are struggling to find their footing in a new macro environment with higher rates.

“I think the unwinding of the growth trade showed that a lot of successful managers in the 2010s were really just on the right side of a factor,” Bates said. “It’s not clear that they were adding alpha; they were almost adding beta-driven returns, not alpha.”

Having been with the $1.4trn US investment giant T Rowe Price for almost 20 years, Bates is the manager of the firm’s Global Select Equity strategy, built specifically to avoid factor tilts.

He said: “If I want to build a product that offers durable steady performance for clients, I have to manage the factor tilts between growth momentum factors and value factors like interest rates or inflation.”

“I want to do that because I want my stock-picking to drive my performance, not being right on which factor is hot.”

“So many other strategies out there, especially concentrated ones, are inadvertent factor bets,” he said. “Clients think they’re buying something that offers conviction stock-picking when it’s really just buying a factor.”

It is not easy running a concentrated equity fund without unintentionally tilting the portfolio towards style or macro factors, but asset allocators are now waking up to the risks, Bates said.

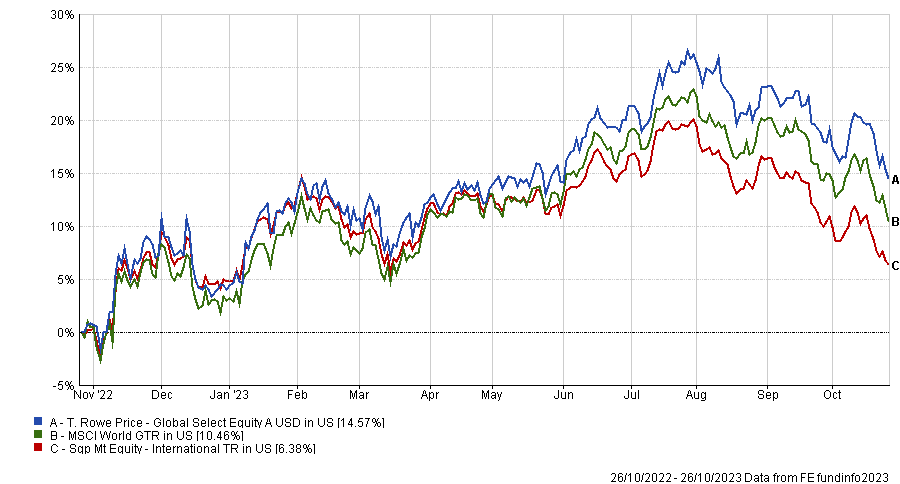

After a strong debut year in 2021 with top-quartile returns, the T Rowe Price Global Select Equity fund was roughly in line with the global equity benchmark with second quartile returns in 2022.

But based on its 2023 year-to-date performance, the strategy is on track to beat more than 90% of its international equity fund peers in the Hong Kong and Singapore mutual fund market.

Most of the top-performing funds of 2021 suffered severely during the global market sell-off in 2022, with some falling as much as 50% peak to trough. However the lack of extreme downside last year has been beneficial for Bates’ strategy.

He said: “If you want to compound value, part of what I’m offering is: I will probably never be the best investment in your portfolio. But I will also never be the worst and I think over time I can be the best.”

Avoiding significant factor-driven drawdowns in performance is of paramount importance to Bates, who learned from his experience as an analyst covering industrials during the 2007 recession that being susceptible to macro factors brings an uncontrollable risk to stock-picking.

“If you understand the compounding, the best way to make money is avoid losing,” he said. “I think the best way to control that and to consistently build alpha is by controlling these macro variables that can kind of overwhelm your performance if you’re wrong.”

So while the foundation of his portfolio is built from bottom-up fundamental analysis, the manager is obsessed with ensuring factor tilts don’t drown out the alpha generated from his stock-picking.

“Some portfolio managers don’t have alpha,” he said. “They just make a big directional bet on the macro and hope they’re right. I want to avoid that downside case and almost earn my alpha with stock picking.”

Investing in both deep value and high growth

The managers’ style-agnostic approach to portfolio construction is clear when looking under the hood of the fund. The concentrated strategy has just 35 stocks – but one can find companies ranging from high-growth tech darlings to deep-value insurance spinoffs.

For example, the fund holds Corebridge Financial, a life insurance business that spun out of AIG, a stock that most investors would describe as deep value.

So while life insurance is not the most exciting sector to be invested in, with the prospect of higher interest rates for longer, the environment for the sector has drastically changed, according to Bates.

He said: “For life insurance companies that have sold a bunch of annuities to guarantee a 4% or 5% rate of return, with higher rates they can now easily invest and make 7% or 8% without taking a lot of market risk. That’s a different story.”

“Corebridge is trading at 0.5 times book, and 4 times earnings, they’re overcapitalised, and management is paying special dividends and returning capital to shareholders.”

One reason markets have valued the company so cheaply is due to the perceived risks around its commercial office portfolio. The sector is facing somewhat of an existential crisis after Covid-19, but the pessimism priced into the company is overdone, in Bates’ view.

Nvidia still looks attractive

Also in the fund’s portfolio is chipmaker Nvidia, which has doubled or tripled year-to-date, drawing a lot of criticism from those who worry the hype around artificial intelligence (AI) is leading to a speculative bubble.

Bates on the other hand, argues that since the company has grown its earnings so incredibly fast over the past year, the upwards move in the stock is warranted.

Sceptics of the company argue that there is excess compute power and that the market is going to shrink next year because although everyone is racing to buy GPU chips today, there will be a glut in chips going forward at some point.

Bates however believes that AI is just “the tip of the iceberg”. He thinks there is going to be “massive investments” for the next five years or more and that the market will continue to grow at its current pace.

Despite record demand for Nvidia’s GPU chips year-to-date, there is still a shortage and both startups and US tech giants alike are scrambling to gain priority on delivery of the prized AI training chip. Taiwan Semiconductor Manufacturing Company Mark Liu chairman recently warned that Nvidia’s AI GPU shortage could persist for years.