Sipping a triple strength rum cocktail yesterday evening, Spy worked out that there were a mere 307 hours or 18,420 minutes until the American election and the rest of us will discover which lunatic we will be saddled with the for next four years. For, objectively, both candidates are about as flawed as each other, but in different ways. The Kamala cackle or the Trump whine: not exactly a joyful choice. It would not be such a tragedy if American leadership affected only Americans but, sadly, the occupant of the White House affects the rest of us, and we don’t get a vote. After a recent trip to the US, Spy can indeed confirm that the Americans themselves are as divided as can be. From taxi drivers to bar tenders, Spy heard passionate arguments in favour, and against, both candidates. Either way, half of America is going to be bitterly disappointed with the outcome.

Spending just a week in finance will give any rookie an idea of just how interconnected our world really is, reckons Spy. On 30October, a joint venture between Albilad Investment Co and CSOP, will see a Saudi Arabian ETF debut on the Riyadh stock market that invests exclusively in MSCI Hong Kong China Equities. The fund has already raised assets of more than HK$10bn ($1.29bn).This launch will surely increase the ties between the Middle East and China, which have been deepening of late with numerous mutual cross border investments. Nearly a year ago, the world’s largest Saudi Arabia-focused ETF launched in Hong Kong. Spy will watch with interest to see if the assets grow.

Rumours have been swirling this week that Allianz may merge or sell part of its AllianceGI asset management arm to give the business greater scale, according to a story from Reuters. The manager currently has about €555bn ($600bn) under management which, although substantial, does not put it in the mega league of European managers such as Amundi and BNP Paribas/Axa Investment Management. Allianz also owns Pimco, but the move is not expected to affect that business which is run on a stand-alone basis.

Spy was in the mood of J.R.R Tolkien this week: “We meet again, at the turn of the tide. A great storm is coming, but the tide has turned.” These words from The Lord of Rings seemed apt reading a report from Morningstar that hundreds of US and European funds labelled “ESG” have either closed, been merged or renamed. In the third quarter alone, 102 funds that had sustainable objectives were closed or merged. This means that in total, 349 funds have been affected by the trend this year. In 2023 the total number was 351, which if the trend continues, will surely be surpassed by the end of December this year. This pace of change is almost certainly being driven by anti-greenwashing rules being rolled out across Europe and the extremely poor definitions from regulators of what truly constitutes a sustainable or ESG investment. It is not all bad news for the sector: globally, nearly $3.3trn is held in about 7,600 ESG labelled funds.

The Brics were meeting in Kazan, Russia this week, with numerous countries of the “global south”, including Malaysia and Brazil, queuing up to get involved. It seems India and China were playing nicely and had forgotten their border squabbles and were friends again. This is rather important as, combined, the two countries are home to 2.9 billion people or 35% of the world’s population and more importantly represent 20% of global GDP. From a snappy investment acronym out of Goldman Sachs in 2001 to a multipolar geopolitical world in 2024, this is truly life imitating art.

Long time readers of Spy know that he has become increasingly astounded at the amount of debt the American government is taking on. It was an additional $850bn in the last three months alone. Some may excuse this largesse as the last desperate throw of the dice by an administration facing a tight election. However, it does not seem to matter who is in charge, Uncle Sam’s credit card keeps getting tap-tap-tapped. And then along comes The Economist with a useful front cover which, if history is anything to go by, is not the best harbinger of dollar stability.

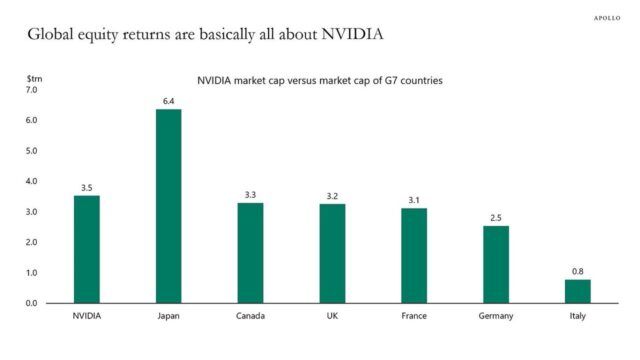

Is Nvidia truly worth more than the entire collection of Canadian, British, French, German or Italian stock market listings, respectively? Factually, yes. Out of the G7, only Japan manages to outdo the chip darling’s market cap. Spy does wonder whether those stock markets are too cheap or Nvidia is too expensive.

The world’s favourite Marmite (Vegemite, Bovril – take your pick) James Bond-ish villain, Elon Musk, was basking in Tesla’s good results and particularly optimistic outlook yesterday. The shares jumped 22%, adding more than $100bn in market cap and boosting the billionaire’s substantial fortune. The EV maker sold 462,890 vehicles globally in the third quarter and predicted sales could jump a whopping 20 to 30% next year. For those people who despise Musk’s pugnacious politics and public commentary, Tesla’s extraordinary success must be a source of great irritation.

Spy’s quote of the week comes from Louis Navellier, “With economic uncertainty diminishing… and political uncertainty diminishing… the stock market is poised to rally, provided that World War III does not materialise.” Ah, there’s the rub!

Spy’s photographers have been out and about in Singapore and spotted a new campaign by Capital Group. The US manager is promoting its Global Corporate Bond Fund in Raffles Place.

Until next week…