Sheldon Chan, portfolio manager at T Rowe Price, said that the investment manager is currently seeing demand among clients for investment grade only mandates in Asia, such is the asset class’ appeal right now.

Nearly all asset managers are overweight investment grade credit at the moment as last year’s sell-off has created attractive entry points, although there is less appetite currently for high yield given the fact that spreads are widely seen as insufficient despite the risk of a hard landing receding.

Chan said that the situation was more nuanced than a straightforward dichotomy between investment grade and high yield would suggest, although he said that overall investment grade was viewed as more attractive at the moment among distributors.

“I think when you’re trying to think about IG versus high yield, the answer may be different depending on which region or which specific credit asset class you’re talking about. So if you’re in the US or Europe, you may be looking at a slightly different backdrop versus what you have in the rest of EM or in Asia,” he said.

“High level conceptually though, the ability to lock in pretty decent yield levels given where Treasury yields are and to do that without much credit risk does push people towards looking at that IG space. Thinking about some of the conversations we’re having with clients, we are seeing interest for IG only mandates across the Asia EM space.”

Overall, Chan is bullish on Asia in particular, noting the favourable structural tailwinds a number of countries, especially in southeast Asia and south Asia, benefit from, as well as the progress their governments have made in managing their fiscal policy in the last several years.

“What stands out as a feature of the Asia credit asset class is number one that it is the higher quality segment within EM. If you look at the macro fundamentals, a large portion of the Asia credit universe is coming from economies that are very well anchored when it comes to their external fiscal metrics. But importantly, the corporate issuers are basically coming from IG-rated sovereigns. That’s reduced a lot of volatility in the sovereign curve and it helps the corporate issuers access the market,” he said.

He singles out Indonesia in particular for the progress the government has made in sticking to their fiscal framework, while he also noted that even with the slowdown in demand for commodities, the country stands to benefit due to its large nickel and copper deposits, which would be important in the green energy and EV transition.

Chan co-manages the Asia credit bond strategy at T Rowe Price, which is benchmarked against the JP Morgan Asia Credit Index Diversified. According to its most recent factsheet, the fund has delivered a 4.3% return this year versus 3.65% for the benchmark. On a three-year basis, this trend is reversed as the fund has delivered a -2.66% return, worse than the -1.55% return recorded by the benchmark.

Chan attributes the underperformance relative to the index over a three-year time horizon due to the impact of the troubles in China’s property sector and to a lesser extent the impact of the Fed hiking cycle, which hurt the fund more given its structural bias towards the least efficient parts of the market.

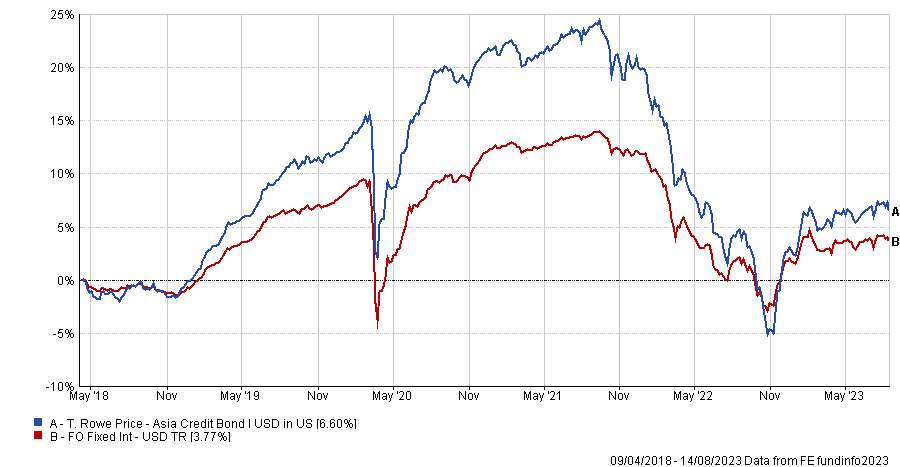

Regarding the impact of China’s property sector, Chan notes that the fund is by no mean alone and indeed its performance stacks up well compared to most of its peers during this period (see chart).

“When you talk about a large industry, $150bn of debt, widely held across the community, bonds trading very quickly from par to 50 cents and below, it’s hard to trade out of that. We took the decision in early 2022 to cut the positions but by then a lot of the losses had been incurred,” he said.

Regarding the upturn in performance versus the benchmark this year, Chan attributed this to the fund timing China’s reopening rally well as this began to fizzle out towards the end of January, around the same time that T Rowe Price began reducing its positioning.

“By the end of January, when we looked at a lot of valuations we saw in China credit, I’d make the argument that you basically recovered about 90% of the 2022 drawdown,” he said.

“So in January and February we actually started to reduce some of our China positioning again to take profit from the positions that did well in January and I think that actually has left us with a higher quality portfolio.”

According to the fund’s factsheet, its largest holdings comprise sovereigns such as the Republic of Indonesia as well as a number of financial issuers such as United Overseas Bank and Bangkok Bank.

Overall, the fund is actually underweight financials compared with the benchmark, although Chan notes that the fund does make concentrated bets in some of the banks that tend to be franchise leaders in their countries.