With the US economy surprisingly resilient in the face of Fed tightening and as a peak in interest rates approaches, investors are coming around to the idea that bonds are back.

However, these bonds are not cheap, according to Sriram Reddy, Man GLG’s head of client portfolio management.

It is for this reason the firm is running some of its lowest allocations to US bonds in their global portfolios since launch, he told a recent media roundtable in Singapore.

“While all-in yields are relatively attractive, spreads – compensation you’re getting for corporate default risk – are no longer extremely cheap at this point in time,” he said.

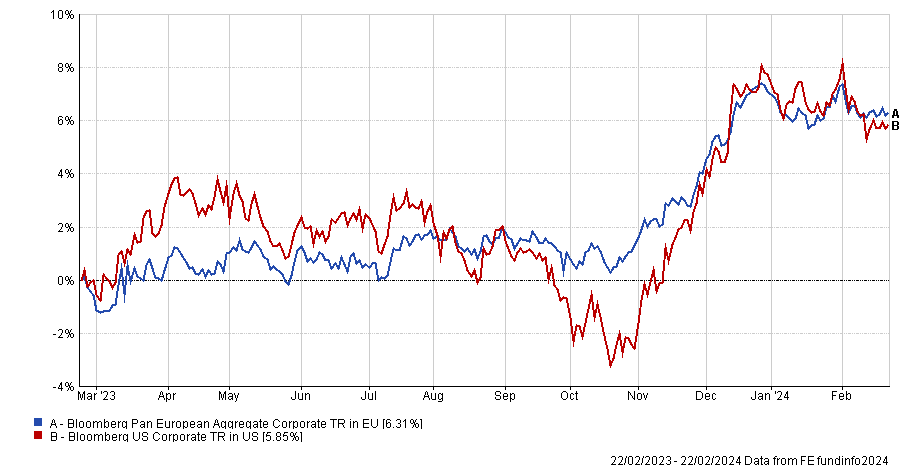

“Certain markets we find are very expensive, such as the US market,” he explained. “We are more focused on opportunities in Europe among developed markets.”

The firm’s investment team is leaning towards the idea that interest rates will be higher for longer and as such, are focusing on what the implications of this will be on markets.

Spreads will likely need to widen

After a strong year, investors are optimistic on the outlook for the US economy, which has allowed spreads in US investment grade and high yield bonds to compress.

Reddy suggested that spread compression has perhaps moved too far and too fast, especially when compared with Europe and emerging markets.

“We think that reflects the expectation from a number of investors that the US will have a soft landing or no landing,” he said. “That enthusiasm has led to spreads continuing to compress.”

“We do think that if we don’t get that follow through from the Fed and if rates are going to be higher for longer that will create more pressures for the economy.”

In his view, markets need to come around to the idea that there is a greater probability of outcomes beyond a soft landing: “that for us means that spreads will likely need to widen,” he explained.

But where Reddy believes investors are being appropriately paid to take additional risk in the bond market is in other geographies, namely Europe.

“We think that in Europe, there are more opportunities of getting paid more to take the risk,” he said.

“When you look at the overall European market, it is generally higher quality than the US: it tends to have companies with less cyclicality when you look at the sector makeup.”

Additionally, the composition of the European market has more favourable characteristics for bond investors, according to Reddy.

He said: “They tend to be a little bit more conservative in their capital structure, so they typically don’t have as much leverage as their US counterparts.”

“We think it would be more prudent to own less cyclical and less leveraged companies if the economic growth slows.”

“Those are more prevalent in the European market, and we happen to get paid more to own them. That for us is a great trade off at this point in time.”

Opportunities in India

Although spread levels aren’t necessarily as attractive in India – a region which has seen a lot of investor interest recently – Reddy believes there are some selective opportunities.

He said: “Investors have moved out of China bonds into India credits, so there have been significant capital inflows already.”

“That has made spreads less attractive in our opinion, but the positive macro backdrop for India means that spreads are likely to remain relatively stable from here.”

He suggested investors look for corporate bonds trading at deep discounts to par with the potential to refinance in a hard currency market or use the local currency market to refinance hard currency assets.