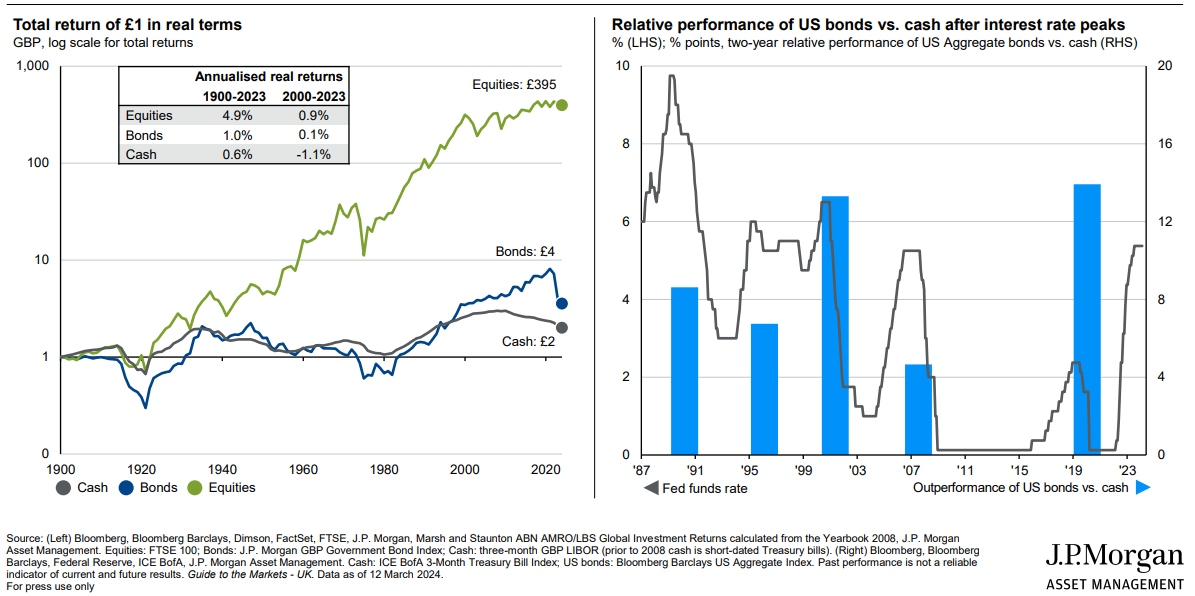

Cash is not as attractive a place for investors to park their money as it might seem. Indeed, despite the short-term appeal of savings rates of over 5%, investors are likely to lose out from the opportunity to generate longer-term returns from other asset classes.

According to date collated by JPMAM, during the 23 years of this century in real terms cash has annualised return of -1.1%, compared with positive returns for equities (0.9%) and bonds (0.1%). The comparable figures since 1900 and 0.6%, 4.9% and 1.0%.

“Western central banks will begin cutting rates in the summer,” Karen Ward, chief market strategist EMEA, at JP Morgan Asset Management (JPMAM), told a recent international media summit in London.

Although consumer spending should reaccelerate in Europe and global trade has bottomed, “so long as this doesn’t reignite inflation, this is good news,” she said.

US bonds typically outperform cash after interest rate peaks, so Ward recommends investors to “lock in yields paid by developed market government bonds and investment grade corporate fixed income”.

Ward (pictured) recommends investors to “lock in yields paid by developed market government bonds and investment grade corporate fixed income”.

Meanwhile, inflation pressures have eased while real wages are growing, which should lift consumer spending. Equities should benefit, and will also be supported by fiscal policy, she said.

However, Ward warned that investors should “be mindful of extreme valuations in segments of the US market, especially top 10 performers, which are trading on forward price-earnings-rations of close to 30x compared with less than 20x for the rest of the S&P 500.

Instead, she advised investors to “diversify across regional stock markets, as discounts of the markets in the UK, the Eurozone and China to the US have widened”.

In addition, alternatives can be used “to plug public market gaps, especially those companies at an early growth which are taking more years (on average seven) to list compared with earlier, when IPOs typically took place within about three years of start-up”.

Most importantly, in a year of multiple elections with their accompanying political noise intensifying, “history says don’t ‘trade’ elections,” said Ward.