The world is on the cusp of the biggest tech replacement cycle it has ever seen because of AI, which partly explains why this top quartile fund manager has been able to hold his nerve despite the recent sell-off.

Sam Konrad (pictured), co-manager of the Jupiter Asia Pacific Income strategy, told FSA during a recent interview, that in January the strategy increased the weighting of its tech stocks in the portfolio. The five stocks it owns are Hon Hai Precision Industry Co, Taiwan Semiconductor Manufacturing Co, MediaTek, Samsung Electronics Co and HCL Technologies.

“When you look at the tech correction, there were several reasons for it, one of which was a concern among the US tech stocks and the extent to which they will be able to monetise their investments in AI. The companies we own in our strategy are already monetising investments in AI. They’re already seeing an increase in revenue and profits and they’re being able to increase their dividends,” he said.

“We’ve seen the performance of our strategy bounce back quite considerably in the last couple of weeks from its low, and when we look back, we think it was right not to panic, not to get too emotional about the fact that the market fell strongly in a couple of days. We held our nerve and we think that will prove to be correct.”

Top quartile performance

The upping of their weighting of the five tech companies is by far the most significant change made to the strategy of late, which generally eschews trading in and out of positions regularly, preferring to take a long-term, patient approach to investing.

Overall, the strategy is heavily concentrated, with holdings typically around 30 stocks. Cash rates vary between zero and 3% and the annual turnover of the portfolio is typically no more than 20%.

It is an income-focused strategy, which means that the overall portfolio needs to have a dividend yield at least 20% more than the benchmark.

The strategy focuses on large-cap stocks with a market cap of more than $3bn, although the vast majority of the portfolio have a market cap in excess of $10bn.

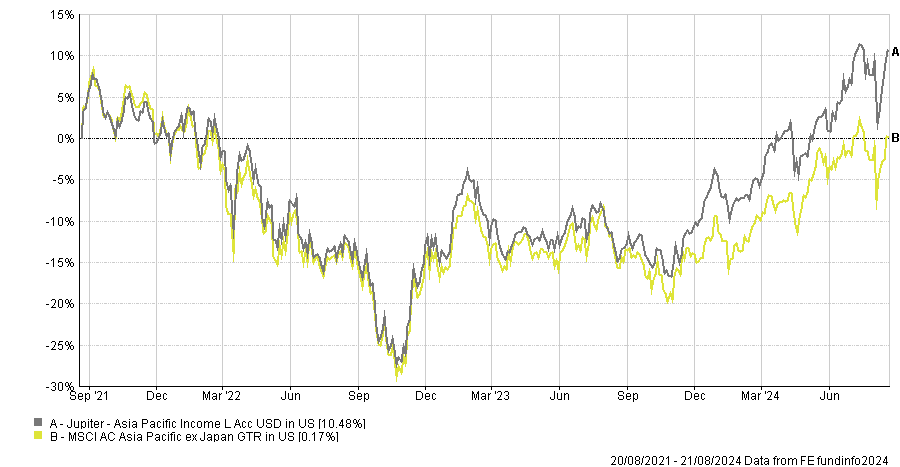

The strategy is a top performer, earning a top quartile ranking on a one-year, three-year and five-year basis, according to FE fundinfo (see chart).

It is to some extent an all-weather strategy (“We don’t think when you invest you have to make a choice between growth and income,” said Konrad), although it tends to suffer a bit when unprofitable tech is on a rampage like in 2020.

Overall, the strategy is fairly defensively positioned, being overweight consumer staples and underweight consumer discretionary, although Konrad explains that this is partly because the strategy prefers to take its consumer discretionary exposure via technology, where it is currently overweight.

Taiwan stance

As well as raising its exposure to tech companies this year, the strategy has at the same time increased its exposure to Taiwan (unsurprisingly given that three of the five tech companies it owns are Taiwanese) to such an extent that Taiwan leapfrogged India earlier this year to become the strategy’s second largest country exposure after Australia.

On the face of it, this appears counterintuitive given that the strategy takes a top-down approach to stock selection meaning that geopolitics features heavily in the decision-making process, although Konrad explains that this is logical.

“We think that the Taiwan risk that people talk about is priced into the Taiwanese stocks that we own, but it’s not actually priced into US tech stocks. And we believe that the Taiwanese tech companies are genuinely world class. They have very few competitors globally, if any, in terms of their technological capabilities and we think they’re invaluable to the global tech supply chains and arguably should trade at higher valuation multiples than they currently do,” he said.

Regarding India, the strategy is now neutral, having been overweight for some time, although this is more of a reflection of the fact that when the strategy received new money, they preferred to allocate it elsewhere rather than having gone off India altogether, Konrad said.

The strategy currently owns five stocks in India and Konrad said that it would quite like to add a sixth, but valuations are the issue.

“We would quite like to add a sixth company to our Indian holdings, but right now we can’t find the company that’s trading at reasonable valuations that fits all of our other criteria that we want to add. We will constantly be on the lookout for that sixth company and we’re prepared to be patient. When the time comes, we will, if we find the right company, be quite happy to add another Indian company, but we’re not going to be rushed into that decision,” he said.

Sam will be joining Fund Selector Asia at our flagship FSA Investment Forum Thailand on 12 September 2024 where he will be presenting Technology, Australia and India: Income and growth in Asia.

Find out more about his session and the event below.