As investors have poured money into Japan on the back of strong equity market performance, the $1.4bn Arcus Japan fund stands out as a top performer.

The actively-managed value strategy is on track to be one of the best performing Japanese equity funds this year, with a return of 34.11% versus 25.65% from the TOPIX index.

Ben Williams, co-manager of the fund, who joined Arcus in 2020, attributes the fund’s recent performance to the experience of the firm’s co-founders Mark Pearson (pictured) and Peter Tasker.

“Value investing has good characteristics for alpha generation over the last 40 years in Japan, but it has had many periods where value has underperformed, and I think this is where Arcus stands out,” he told FSA.

“Because the fund has its successful track record, during the periods where value underperformed – there was no real pressure for Mark as the lead manager to change his approach.”

“I think that’s a key factor because having a successful business which is owned by the fund managers gives them the freedom to really follow their convictions.”

The investment firm is majority owned by its founders Pearson and Tasker who started the firm in 1998.

Despite a decade-long period of underperformance for value-style investing after the Global Financial Crisis (GFC) in 2009, the value strategy has still managed to comfortably outperform the TOPIX – returning 369.24% compared to 243.14% from the index.

“During their investment career they’ve seen monumental bull markets, the most miserable bear markets, and have invested throughout those periods,” Williams added. “I think experience in different market environments helps.”

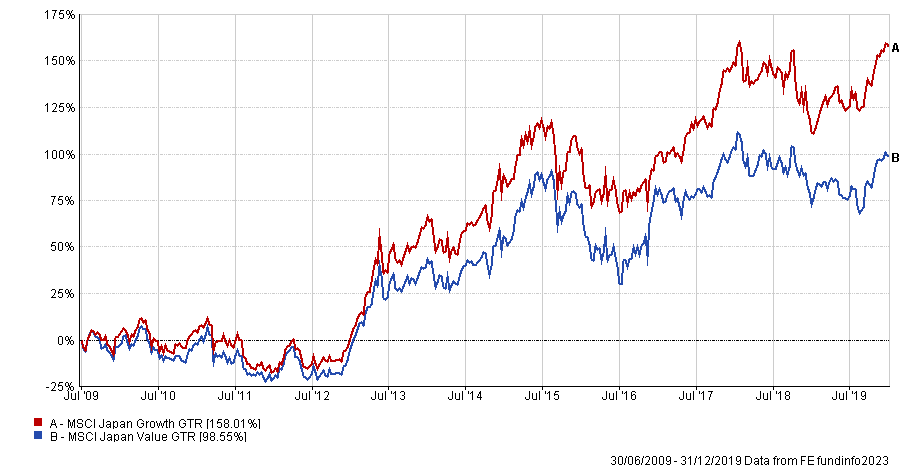

The chart below shows the divergence between value and growth investing in Japan after the GFC.

Williams said: “If you’re a young fund manager working at an organisation as a value investor, you would have quite a difficult period of time.”

“You might well have strayed from your investment principles because you had some career risk, whereas Mark and Peter could stick to their principles, so when the value recovery came, they were fully onboard with that.”

Although value has been particularly strong over past few years, it has been the better performing investment style in Japan for the past three decades or so.

The MSCI Japan Value index is up 356.70% since 1995, versus 113.72% from the MSCI Japan Growth index in local currency terms.

Perhaps another contributor to the success of the fund is that while many investors think through the lens of what the Japanese Yen or inflation or the economy is going to do when investing in the region, Pearson is laser-focused on the individual companies and their fundamentals.

“What is top of mind is always looking for the next good company at the next right price,” he told FSA. “It’s not so much is the Yen going do this or that, or what the general economic trend is.”

Although a bad economy will undoubtedly affect the fundamentals of businesses that operate within it, sometimes the market will price-in too much pessimism into a company’s business outlook, which can be an opportunity for value investors like Pearson.

“You can still make money on a company in tough times, and we often do that,” Pearson said. “We often invest in companies at the worst point in the cycle because things are not going to get any worse than that.”

“The market is a discounting mechanism, so the market discounts a recovery before the recovery happens.”

However, he emphasised the importance of having good sell-discipline and flagged the emotional toll it can have on value investors without conviction.

“The destiny of a value fund manager is to be investing in miserable situations,” he said. “You’re trying to grasp onto some shoots of hope and optimism – and when things are starting to look really good, that’s the time when you say, ‘off you go’.”

Japanese stock market reforms are encouraging

Foreign investors have warmed to investing in Japan over the past year thanks to the latest Japan Tokyo Stock Exchange (TSE) reforms aimed at incentivizing companies to improve their capital efficiency, and Williams said there is good reason investors are taking these changes seriously.

“There were lots of companies in Japan with lots of idle assets and most people assumed they would sit idle forever,” he said. “I think government action along with the TSE is working towards breaking down these long-held assumptions on Japan.”

Another assumption investors have is that there is no market for hostile takeovers in Japan, but the latest government guidelines on mergers & acquisitions from the Ministry of Economy, Trade and Industry (METI) suggests otherwise.

Williams said the latest guidelines should have implications on the discounts typically placed on lowly valued Japanese stocks.

“If investor assumptions were that there’s no market for corporate control, but now there is potentially a market control, it means discounts on companies should be less,” he said.

One aspect of the METI guidelines Williams noted was the specific reference to discouraging the use of employee retention as an excuse for turning down a takeover.

“I think this reflects the fact that the labour market in Japan is so tight, and it seems that the authorities aren’t concerned about takeovers leading to significant increase in unemployment in Japan,” he explained.