Both funds use the MSCI World Health Care Index as their benchmarks, with the Parvest fund using the Ucits III-compliant 10/40 version of the index, which imposes concentration limits (performance of both indices was identical over the three-year period ending 31 October).

One of the main factors in the performance of the two funds is exposure to the sub-industries in healthcare, Ng said.

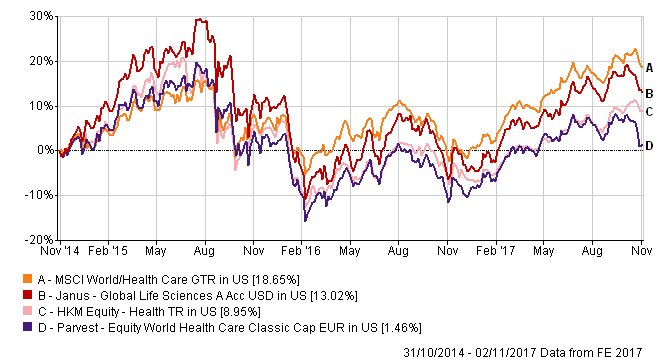

The Janus fund outperformed the benchmark and the Parvest fund by a healthy margin in 2012-14, thanks to its bias toward biotech. “In 2012-14, the biotech sector performed very well.

“After 2015, you don’t see a very big difference between the performance of biotechnology and pharmaceuticals and in 2016, both biotech and pharmaceuticals underperformed,” he said.

As a result, in 2015 and 2016 both funds underperformed.

So far in 2017, both products have delivered double-digit returns, with the Janus fund doing slightly better than the index and Parvest underperforming it.

Both funds have a negative alpha, high beta, and volatility exceeding that of the index, as measured on a three-year basis. While the measurements for the five-year period, which includes the biotech boom of 2012-14, put the Janus fund in a better light with alpha of 0.40 (Parvest’s remains negative at -4.98), the numbers underscore the difficulties in outperforming the index in a risky and volatile industry.

Biotech carries high risk. “Biotech companies require a lot of resources for research and development, a sustainable investment before they pay the money back” said Ng. This results in higher risk and volatility.

|

Janus |

Parvest |

MSCI World Health Care Index |

| 3-year return (cumulative) |

13.52% |

1.20% |

18.87% |

| 1-year return |

20.13% |

12.46% |

19.80% |

| 3-year Alpha |

-2.47 |

-5.76 |

|

| 3-year Beta |

1.25 |

1.14 |

|

| 3-year Sharpe Ratio |

0.05 |

0.00 |

|

| 3-year Volatility |

16.44 |

14.64 |

12.06 |

Data: FE, 31 October 2017, returns in US dollars, ratios are annualised