Despite some market dynamics that resemble the tech bubble of 2000, portfolio managers at GMO believe this time it’s different.

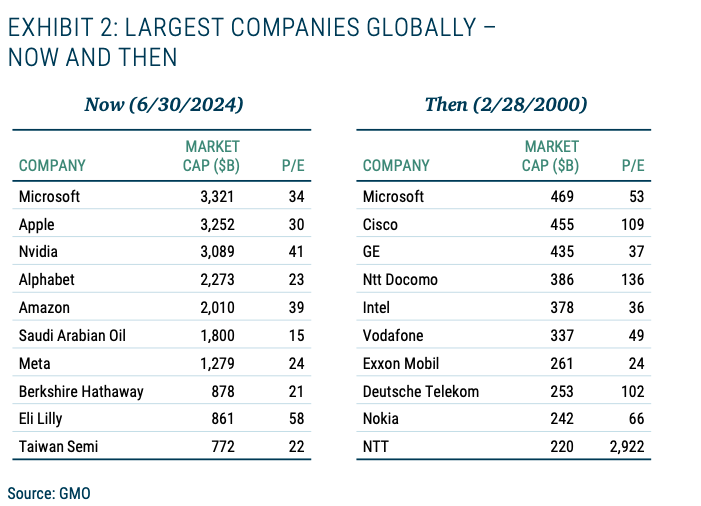

Some investors worry that the narrowness of today’s equity market, the concentration of the largest stocks, and the high dispersion in returns are all eerily reminiscent of the 2000 tech bubble top.

However, the fundamentals and valuation multiples of the largest stocks today look much better than the moments before the bubble burst in 2000, according to portfolio managers at GMO.

This level of optimism isn’t typically associated with a firm that has a reputation for calling out market bubbles and lambasting market participants for irrational exuberance.

Earlier this year, GMO’s chief investment strategist and co-founder Jeremy Grantham warned that the artificial intelligence hype could be a bubble within a bubble and would eventually end in recession.

But this time around, “the stars have aligned differently” say Ty Cobb, Tom Hancock and Anthony Hene, the GMO portfolio managers who authored the investment firm’s most recent report.

“In the short term, it’s anyone’s guess,” they said. “But looking further out, whether today’s mega-caps turn out to be great or less-than-great investments will be a result of the evolution of their fundamentals and the consequent impact on their valuation multiples.”

“Unlike in 2000 when we held only a non-material weight in the top 10, we invest with confidence in a number of these companies today.”

Indeed, the firm’s GMO Quality Strategy, which runs $24.5bn in assets, counts Microsoft, Apple and Alphabet among its top 3 holdings at 6.7%, 5% and 4.7% respectively.

The prior bubble burst

During the 2000 bubble, markets went too far in extrapolating the preceding five-year fundamental returns of 22% per year of the top-10 biggest firms.

“The valuation was simply too rich,” the GMO managers said, noting that the price-to-earnings-ratio reached 60x at its peak, meaning that even with a 19% annualised earnings growth over the next five years the multiple would have still been over 25x.

“In reality the outcome was starkly different – the fundamental return was a relatively puny 8% p.a. for the group, with earnings falling at the telecom companies after what turned out to have been disastrous capital allocation in 3G spectrum auctions,” they said.

They believe that compared with today’s top 10 medium P/E ratio of 27x, the group’s 19% annualised fundamental return expectations are far more achievable.

“If today’s top 10 were to deliver on 19% fundamental return expectations and prices were to stay the same this time around, the multiple would collapse to 12x by 2029,” they said.

“Implicitly, investors expect less from the mega-caps now than they did in 2000. In a real sense, the stakes are lower today.”

They also note that the profitability and balance sheet strength of the top 10 today sits just shy of the 10th percentile of GMO’s quality screen, compared with in 2000 when the top 10 group “were barely better than the median business”.

They added: “That fits well with our fundamental assessment of quality – most of the current crop have stronger barriers to entry, interesting optionality (e.g., in AI and digitalization), and a better record in capital allocation, too.”

They argue that by focusing on fundamentals via quality, while controlling valuation risk, investors can “avoid overreach on the earnings multiple”.

They said: “If we compare today’s markets with the market top in 2000, we see less to fear today on both the fundamentals and the multiples.”