Hollie C. Briggs, CFA, CAIA

Head of Global Product Management

Growth Equity Strategies Team of Loomis Sayles, an affiliate of Natixis Investment Managers

Beware the catchy nicknames and acronyms which feed the 24/7 news cycle. Pundits often give these names to high-profile stocks, which then trigger yet more upward price momentum as herd mentality exacerbates short-term thinking. Whether in up markets or down markets, assigning more weight to recent events – known as recency bias – is one of the key dangers long-term investors must guard against. While these reflexive responses to short-term market variables have no impact on long-term value, they do create asset pricing anomalies that patient, disciplined investors can take advantage of.

Active, differentiated decision-making leads to differentiated returns

Take Meta Platforms, for example, which we have owned continuously for almost 13 years. In 2022 as the “work from home” bubble burst, many managers doubted Meta’s decision to allocate billions of dollars to AI and its metaverse, causing them to substantially reduce or sell their holdings. In contrast we saw this as an opportunity, so added to our Meta holdings throughout 2022. When AI exuberance surged in 2023 many managers bought back into Meta but are unlikely to have fully benefited from its 194% annual return that year, including a 76% rebound in the first quarter alonei. Similarly, the Russell 1000 Growth Index, which follows a price momentum strategy, saw its weight in Meta fall from 3.35% at the start of 2022 to 0.34% by the end of 2022i, leaving it with only a fraction of the benefit from the company’s 2023 rebound. Our 4.99% position in Meta at the end of 2022 showed our highly differentiated active ownership approach – and conviction – in stark contrast to peers who traded in and out unnecessarily, increasing trading costs and negatively impacting their returns.

It is not simply ‘what’ you own, that matters but ‘how’ you’ve owned it over time

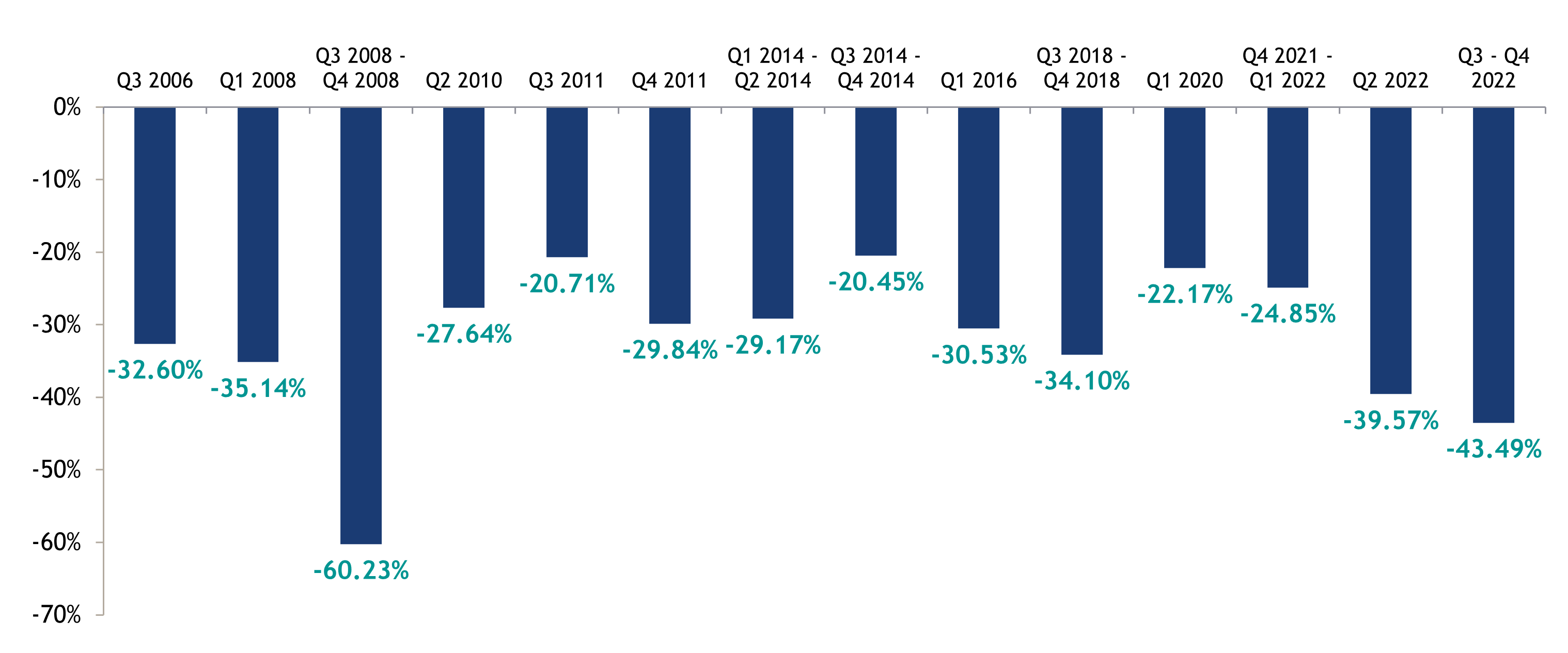

Even great businesses routinely endure significant share price drops. In the nearly 19 years we have owned Amazon it has declined 20% – 60% 14 times. Yet despite this, it has outperformed the Russell 1000 Growth index by over 12x during this period.

AMAZON: PERIODS OF LARGE DECLINES SINCE Q2 2006

Examples above are provided to illustrate the investment process for the strategy used by Loomis Sayles and should not be considered recommendations for action by investors. They may not be representative of the portfolio’s current or future investments, and they have not been selected based on performance. Loomis Sayles makes no representation that they have had a positive or negative return during the holding period.

Past Performance is no guarantee of future results.

Focus + conviction drives outperformance

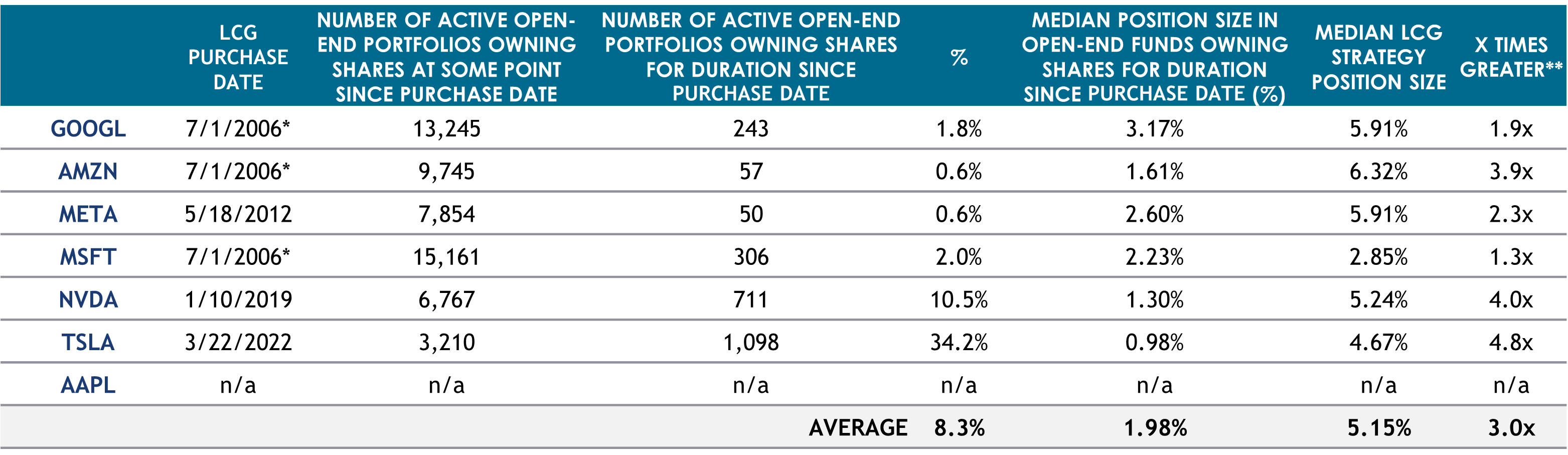

When stocks are outperforming, they are easy to hold. It’s far harder to stay invested when everyone is selling. The table below demonstrates how our ownership history (focus) and position size (conviction) has been differentiated over the entire life of our strategy. As of the end of 2024 six of the Magnificent 7, Alphabet, Amazon, Meta, Microsoft, Nvidia, and Tesla, are in our top-ten holdings, signaling that we believe they are among the most attractive reward-to-risk positions in our portfolio. We have never owned Apple. Our average holding period for these companies is now approaching 13 years.

Holding period and concentration of companies held in Large Cap Growth strategy since purchase date

**x Times Greater is the calculation resulting from the Median LCG Strategy Position Size divided by the Median Position Size in Open-End Funds Owning Shares for Duration Since LCG Purchase Date.

Data Sources: Loomis Sayles, FactSet.

*As of June 30, 2024. Although this information is dated, we believe that the results are still reliable.

The portfolio manager for the Growth Equity Strategies joined Loomis Sayles May 19, 2010, and performance prior to that date was achieved at his prior firm. Examples above are provided to illustrate the investment process for the strategy used by Loomis Sayles and should not be considered recommendations for action by investors. They may not be representative of the strategy’s current or future investments and they have not been selected based on performance. Loomis Sayles makes no representation that they have had a positive or negative return during the holding period.

Past performance is no guarantee of future results.

Behavioral biases create market opportunities

Traditional economic theory assumes individuals make decisions rationally. However, as we’ve seen, investors often make emotional and irrational decisions – exacerbated by the 24/7 news cycle. This does, however, create opportunities for investors that can identify these pricing anomalies and take advantage of them.

The first principle of our GES Team’s Alpha Thesis holds that our long-term investment horizon allows us to capture value from secular growth and capitalize on the stock market’s shortsightedness through a process called time arbitrage. We believe our ability to consistently implement the tenets of our GES Alpha Thesis constitutes a differentiated approach and our 2nd percentile ranking for absolute and risk-adjusted returns since strategy inception in 2006 through year-end 2024 show the success of this approach.

i Source: Loomis Sayles, Factset, FTSE Russell

Past Performance is no guarantee of future results.

For readers in Hong Kong, click here to learn more.

For readers in Singapore, click here to learn more.

In Singapore: This document is provided by Natixis Investment Managers Singapore Limited having office at 5 Shenton Way, #22-05/06, UIC Building, Singapore 068808 (Company Registration No. 199801044D). Mirova Division (Business Name Registration No.: 53431077W) and Ostrum Division (Business Name Registration No.: 53463468X) are part of NIM Singapore and are not separate legal entities. The content of this document is strictly confidential and has been prepared for informational purposes only and for the exclusive use of institutional and accredited/professional clients or prospects. Under no circumstance may a copy be shown, copied, transmitted or otherwise distributed to any person or entity other than the authorised recipient without the advance written consent of Natixis Investment Managers Singapore Limited. Investment involves risk. The information contained herein does not constitute an offer to sell or deal in any securities or financial products. The content herein may contain unsolicited, general information without regard to an investor’s individual needs, objectives, risk parameters or financial condition. Therefore, please refer to the relevant offering documents for details including the risk factors and seek your own legal counsel, accountants or other professional advisors as to the financial, legal and tax issues concerning such investments, if necessary, before making investment decisions in any fund mentioned in this document. Past performance and any economic and market trends or forecast are not necessarily indicative of the future or likely performance. Certain information included in this document is based on information obtained from other sources considered reliable. However, Natixis Investment Managers Singapore Limited does not guarantee the accuracy of such information. Natixis Investment Managers Singapore Limited is a business development unit of Natixis Investment Managers, the holding company of a diverse line-up of specialised investment management and distribution entities worldwide. The investment management subsidiaries of Natixis Investment Managers conduct any regulated activities only in and from the jurisdictions in which they are licensed or authorised. Their services and the products they manage are not available to all investors in all jurisdictions. It is the responsibility of each investment service provider to ensure that the offering or sale of fund shares or third-party investment services to its clients complies with the relevant national law. This advertisement or publication has not been reviewed by the Monetary Authority of Singapore.

In Hong Kong: The content of this document is strictly confidential and has been prepared for informational purposes only and for the exclusive use of professional investors. Under no circumstance may a copy be shown, copied, transmitted or otherwise distributed to any person or entity other than the authorised recipient without the advance written consent of Natixis Investment Managers Hong Kong Limited. Investment involves risk. The information contained herein does not constitute an offer to sell or deal in any securities or financial products. The content herein may contain unsolicited, general information without regard to an investor’s individual needs, objectives, risk parameters or financial condition. Therefore, please refer to the relevant offering documents for details including the risk factors and seek your own legal counsel, accountants or other professional advisors as to the financial, legal and tax issues concerning such investments if necessary, before making any investment decisions in the fund(s) mentioned in this document. Past performance information presented is not indicative of future performance. If investment returns are not denominated in HKD/USD, USD-/HKD-based investors are exposed to exchange rate fluctuations. Natixis Investment Managers Hong Kong Limited is a business development unit of Natixis Investment Managers, a subsidiary of Natixis that is the holding company of a diverse line-up of specialised investment management and distribution entities worldwide. Certain information included in this material is based on information obtained from other sources considered reliable. However, Natixis Investment Managers Hong Kong Limited does not guarantee the accuracy of such information. Issued by Natixis Investment Managers Hong Kong Limited.