Each month we feature the allocation in one of the three portfolios offered by FE Advisory Asia: cautious, balanced and growth. Data is included to show how well the portfolio has done compared to the previous month and year-to-date so that readers can get a sense of performance.

Additionally, Luke Ng, senior VP of research at FE Advisory Asia, provides a concise analysis on macro events and their potential impact on the portfolio.

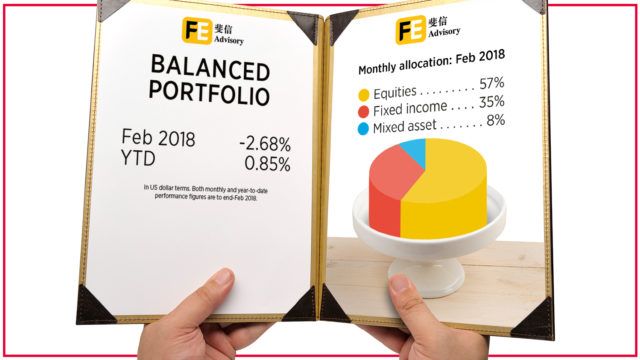

A breakdown of the Balanced portfolio at the end of February 2018. Performance figures are in the menu image above.

Portfolio breakdown and holdings are based on latest published data for each constituent, which may have publication dates that differ.

Percentages are based on current holdings and should only be used as a guide. Some information is provided to FE from independent third parties whom FE does not control. FE cannot guarantee the accuracy or reliability of the data, or its suitability for use by all investors.

How did the market perform in February?

February proved a difficult month for investors as nearly all markets went into negative territory. The market fell early in the month but managed to claw back some of the losses by month end. The primary cause of the fall was the better than expected US wage data, which raised fears of further rate rises by the Fed. This initially hit the bond market before impacting the global equity markets. Bond proxy sectors, such as healthcare, were hit the hardest, whereas energy and technology managed to hold up better.

While most equity markets suffered in February, some markets fared better than others. Japanese equities fell less than most of its developed market peers in US dollar terms, thanks primarily to a stronger yen, which helped smooth out the losses. On the flip-side, the UK was one of the weakest developed markets, dragged down partly by the comments of the Bank of England governor Mark Carney that the UK rate rises would come sooner and more quickly than expected.

Among emerging markets, Asian equities generally underperformed their peers in Europe and Latin America, weakened primarily by a tougher pull back from the leading nations including India and China. In contrast, Thailand and Russia managed to secure marginal gains during the month. The former held up better thanks to the supportive performance of the energy and utilities sectors, and the latter benefitted from stronger economic data, softer inflation and the move to lower interest rates by the Russian central bank.

Following the correction in January, US treasury yields continued to rise during the month. Fixed income generally registered negative returns, with investment grade corporates faring worse than sovereign and high yield bonds.

How did the FE balanced portfolio perform?

As all the key asset classes suffered a downturn in February, our FE Advisory balanced portfolio fell 2.68% in US dollar terms. Year-to-date however, the portfolio is still up 0.85%. Approximately 35% of the portfolio is invested in fixed income funds, well diversified among sovereign, investment grade and Asian high yield. It is primarily denominated in US dollars. These exposures contributed around -0.30% to the portfolio losses during the month. The remainder was due broadly to the losses in the equities sleeve of the portfolio. The best performing equity fund in our portfolio was the JPMorgan Japan (Yen) Fund. It managed to secure marginal gains aided by the strong rebound in the second half of the month and by the appreciation of the yen versus the US dollar. Our holding in a China dividend focused strategy also helped mitigate some of our losses as the fund outperformed on the back of its defensive nature.

FE Advisory Asia portfolio performance

| Jan 2018 | Feb 2018 | YTD 2018 | |

| Cautious | 1.43% | -1.58% | -0.17% |

| Balanced | 3.64% | -2.68% | 0.85% |

| Growth | 5.19% | -3.60% | 1.39% |