After being shunned by investors for several years, Chinese equity markets rallied sharply in late September following a surprise stimulus package announcement.

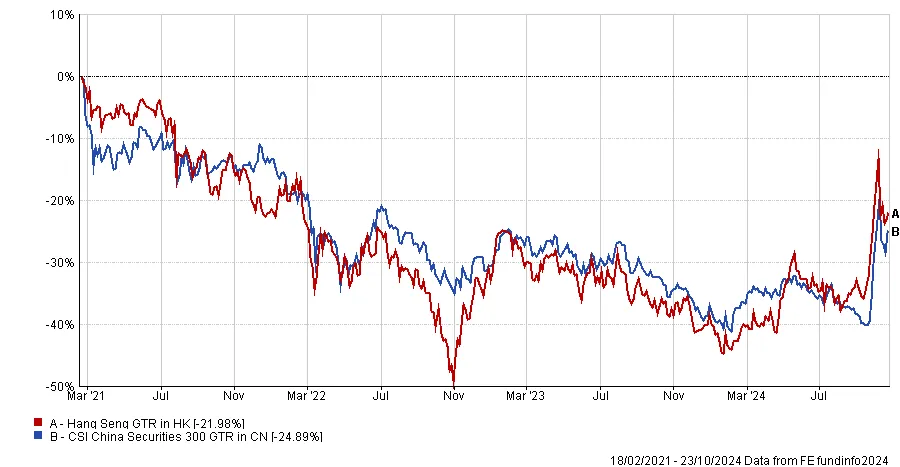

The Chinese onshore CSI 300 index has since risen 23.8% over the past month; meanwhile the Hong Kong Hang Seng index has risen 13.8%.

But after this breakneck rally, “it is hard to argue that China overall is cheap and oversold”, according to Duncan Robertson, portfolio manager of Asia strategies at TT International.

“MSCI China is very close to its 5- and 10-year median P/E valuations,” he said in a recent note. “This comes against a backdrop where the fundamentals are arguably worse than at almost any time in the past 10 years, other than during the prolonged covid lockdown period.”

His core view is that China’s economy is still challenged due to geopolitics, demographics, excess debt, deflation, and the unwinding of its property bubble.

He said: “Perhaps the best template for what is likely to happen in China is Japan. As Japan deflated, the market went through a multi-year period of underperformance, punctuated by the occasional sharp rally on hopes of a bottom.”

“In our view, this is what we are witnessing in China now,” he added.

Both the Hang Seng index and the CSI 300 index are still down more than 20% from their previous highs set in early 2021.

As such, in Robertson’s Asia equity strategy, he is materially underweight China, partially offset by an overweight to Hong Kong in the form of international businesses.

He has added to some Hong Kong/China positions in recent days, including Prudential, Johnson Electric, Mindray Medical and Proya.

However, he used the recent rally to trim positions such as Alibaba “due to concerns that China’s ecommerce market is increasingly mature and competitive”, he said.

But this underweight may become a headwind in the short term, as one of the measures announced by Chinese authorities include credit lines designed to help its listed companies fund share buybacks.

Although this is something that concerns Robertson, he said: “These may be largely symbolic, but they are effectively telling corporates to buy the market, and by extension, telling citizens to do the same.”

“We have seen in the past that China can experience sharp retail investor-fuelled rallies and that valuations can move well ahead of fundamentals.”

“While this is clearly a risk to being underweight, it is one that we are comfortable with, as banking on Chinese retail investors buying the market is far from a compelling investment case when weighed up against the aforementioned structural issues and the exciting opportunities we see in other markets.”