As economic growth recovers from the pandemic, Barings favours high yield (HY) credits, with BB+ names now comprising nearly 60% of the market, up from 35% in 2007.

“This uptick in quality is due in part to last year’s record fallen angel activity, as a number of large, investment grade (IG)-rated companies were downgraded into HY as the pandemic took hold,” Martin Horne, Barings’ head of global public fixed income, told FSA.

The asset manager has been betting on companies which it categorises as “rising stars” that have the potential to be upgraded to IG in the next one to two years.

In the US market, according to Barings internal analysis, as much as $200bn of HY debt looks likely to migrate back to the IG market, which presents opportunities to identify candidates for upgrades.

“We have already seen an improvement in credit rating trends, with recent rating upgrade activity outpacing downgrades, and as we look ahead, one of the bright spots for the HY market should be around this increased ‘rising star’ activity,” said Horne.

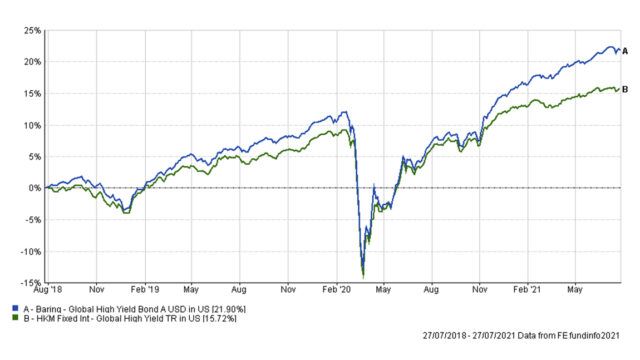

Barings has total assets under management of more than $382bn. It runs the Barings Global High Yield Bond Fund, which has exposure to North American and European HY corporate bond markets.

The $2.21bn fund consists of 13% in the energy sector, followed by healthcare and basic industry at 9.3% and 8.1% respectively. It has the least exposure to financial services at 6.2%, services at 6.1% and retail at 5.7%, the latest fund factsheet shows.

When compared with the global HY fixed income average, the Barings fund posted a 21.9% cumulative return over three years, while the sector reported a 15.72% return, according to FE Fundinfo. The fund is quite volatile over a three-year period, with volatility of 10.03% compared with the sector average of 9.89%, FE Fundinfo data shows.

Tactical allocations

In terms of sectors, Horne said he favours pro-cyclical sectors such as energy and leisure, which have benefitted from the post-pandemic reopening up as vaccination rates increase. On the other hand, he is negative towards the retail sector, which he believes, faces more structural headwinds in the future.

Despite increasing concerns over risks due to climate change regulations, the fixed income head at Barings has “tactically” increased exposure to the energy sector, including investing in some high quality fallen angel energy names that entered the market. He thinks the energy sector is mispriced after the Covid-19 related severe drawdowns in the first half of 2020.

The annualized dividend yield for most share classes of the fund is around 7.5%, and the ongoing charges figure for the retail share classes is about 1.34%, according to the factsheet.

To minimize influence from US treasury bond yields, Barings overweights higher coupon and shorter maturity bond holding, and has limited exposure to bonds which mature after at least 10 years.

“If periods of rising [US] treasury yields are associated with higher growth and inflation prospects, as has been the case during the first half of 2021, this type of a reflationary environment is typically a positive backdrop for HY bond markets.”

Horne added that the resurgence in consumer demand is expected to support company earnings, revenues, and cash flows in this and next year.

In terms of risks, Horne said he continues to look out for credit default candidates.

“Given investments here are made in below IG rated issuers, credit risk is a key risk factor within the HY bond market, which our team aims to manage by leveraging our large investment platform and undertaking rigorous due diligence on all underlying strategy holdings,” said Horne.

Barings Global High Yield Bond Fund vs sector average