Investing in high yield makes sense right now given the current market consensus that the US Federal Reserve will be able to engineer a soft landing. That is the view at least of Sunita Kara, Aviva Investors’ global co-head of high yield.

Since the beginning of the year, there has been no shortage of asset managers who have said that now is a good time to reengage with fixed income because of the attractive entry points on offer following last year’s sell-off.

However, nearly all of the interest has been geared towards investment grade thus far as most asset managers have made the argument that there is no need to look further down the credit curve because of the yields IG already offers.

A corollary of that argument is that high yield is not sufficiently compensating investors for the recession risk currently. The ICE BofA US High Yield Index Option-Adjusted Spread, for example, was last quoted at 3.95%, for example versus 10.87% when the coronavirus crisis first hit in March 2020.

Kara views that approach as outmoded given the fact that inflation has started to slow and growth remains robust despite 11 interest rate hikes.

“If the base case is for a US or global recession, then clearly that’s not what we’re being compensated for, but our base case is that we continue on this low growth, bit of a disinflationary path, at least for the next three to six months and therefore high yield valuations make sense where they are today.

“Year to date outflows from the asset class are about $12bn and that’s because there wasn’t the expectation that the economic outlook would be having that soft landing narrative. But, at the moment, 400bp of spread, 8.25% of yield, it’s attractive enough for asset allocators to put some money to work in high yield.”

Kara also noted that a number of high-yield issuers had responded to the surge in liquidity following the pandemic by pushing out their debt maturities and in some cases paying down their debt altogether, thereby minimising the risk of default.

“The maturity profiles for the next two to three years, 10% of that is triple Cs but the majority that is coming due is double Bs and we don’t necessarily think that there will be defaults coming from higher quality high yield. It will just be a pricing exercise where double Bs now have to pay twice as much in cash interest costs than they have currently locked in,” she said.

“Triple C average default rates tend to be about 17%; for double Bs, it’s less than 1%. So that’s strategically why it makes sense and even now where we are in the current cycle, there’s no need to reach into the lowest quality segment of high yield because the yields are very attractive on the higher quality side.”

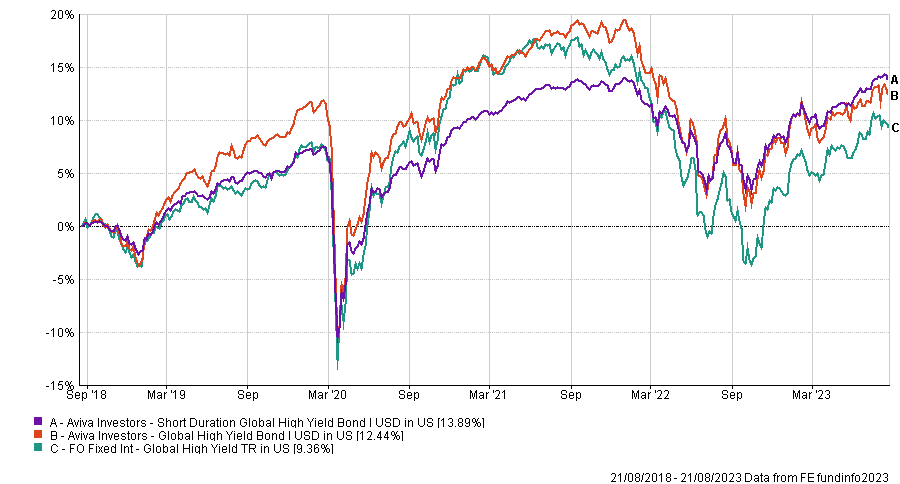

Kara is co-manager of the $3.87bn Global High Yield Bond Fund as well as the $321.7m Short Duration Global High Yield.

The Global High Yield Bond Fund ranks in the second quartile compared with its peers on both a three-year and five-year time horizon with returns of 2.7% and 12.44% respectively, according to FE fundinfo.

Meanwhile, the Short Duration Global High Yield fund ranks in the first quartile, with returns of 8.06% and 13.89% over the same period.

The Global High Yield Bond Fund invests mainly in high yield credit issued by corporations anywhere in the world, although it has a particular emphasis on North America and Europe. It invests at least two-thirds of its total net assets in bonds that are rated below BBB- by S&P or Baa3 by Moody’s or are unrated.

The Short Duration Global High Yield Fund has a similar investment philosophy but invests primarily in high yield bonds with maturities of five years or less.

Generally, Kara notes that Aviva’s current positioning is defensive, due to the fact that we are late in the economic cycle. Kara notes within cyclical, there is room to differentiate though.

“We’ve got structural weak areas like retail, which is now at risk of a pick-up in defaults. On the other hand, we do find there is huge amounts of resilience in the leisure sector. That leisure trading is working even two years after the reopening post-Covid. Things like cruises, hotels and airlines. There is pressure on income, but people are still finding money to spend on travel,” she said.

She describes financials as “interesting”, noting the improvement in capital ratios and non-performing loan ratios banks have posted over the last decade, although she said that she tends to avoid going towards the lower end of the capital structure.

This is not necessarily because of the debacle following Credit Suisse’s writedown of its AT1 bonds but rather because of the volatility.

“The lowest quality, the AT1s or the contingent capital securities, they tend to be volatile. So whilst we may get banks with very healthy core equity tier 1 ratios, it doesn’t necessarily prevent that subordinated paper from being volatile during periods of an increase in market volatility. In order to be enticed to go lower down the capital structure, we do need a backdrop of low market vol, low rates vol and low credit vol,” she said.

Arguably Aviva’s biggest conviction comes in relation to geographies, where the fund is overweight Europe versus the US currently. Kara notes that this is an arbitrage play as European high yield is currently trading about 70bp wider than US high yield, whereas typically European high yield has traded inside US high yield.