“Not all innovations are equal”, Spy remarked to an American GFIG fund salesman and old friend who he caught up with this week. The veteran unveiled his most exciting whiskey find in years, Skrewball Peanut Butter Whiskey (yes, it is a thing). Consuming too much of this rather gruesome concoction led to a discussion on decision-making. According to Herodotus, the venerable Greek historian, the Persians always deliberated on significant decisions while they were drunk. Vitally, they then reflected and reconsidered their decisions the next day once they had sobered up. If a decision was approved when drunk and when sober, the decision was approved overall. Spy’s conclusion, for the record, is that Skrewball is not delicious under any circumstances, but the Persians were definitely onto something.

Schroders is on the hunt for a new client executive to join its “Client group team in Hong Kong to provide sales support to institutional business and pension business teams.” While the job description includes some rather mundane team support tasks such as updating salesforce and answering client queries, Schroders suggests that a “CFA candidate will be an advantage”. Spy reckons this suggests the role is a rather fast-track route to a proper sales function, for those prepared to do the hard yards.

The heady allure of private markets with the promise of returns that make a casino blush, have made PE vehicles awfully desirable to private banks and family offices. But, what if the PE firms can’t exit their large investments, wonders Spy? Right on queue, Federated Hermes has put on an important piece on the challenges facing the industry and all is not quite so rosy. “Global buyout-backed exit value was down 66% in 2023 versus 2021, leaving the industry with an estimated $3.2trn in unexited assets sitting in general partner portfolios. In Q1 2024, private equity exits reached their lowest level in three years. The dormancy of the exit market is leaving investors without cash to commit to new opportunities, stagnating private equity allocations within investor portfolios. Despite expectations that macroeconomic conditions are set to improve, 2024 is projected to be the second worst year for exits since 2016.” Ouch! Buyers, you have been warned.

With China’s stock market being powered by the intoxicating rush of government stimulus, Spy, along with the rest of the market is wondering if this rally is at all sustainable or is the best of the run behind us? Fidelity, for one, still thinks China represents good value. Graham Smith, put out an insight piece making the case. “While recent market gains have been considerable, China’s stock markets still look inexpensive compared to the amounts companies are earning. Shares have broadly moved from being extremely cheap to less cheap. At the end of August, the MSCI China Index traded on just 8.9 times forward earnings compared with 17.7 times for world markets. Market gains of around 25% since then imply that this rating may have increased to about 11 times, which is still low.” Hard to argue with that, reckons Spy.

It is not just China that is cheap, but emerging markets in general look good value too, according to strategists at Pictet Asset Management. “Emerging market equities are very cheap with a number of markets showing healthy earnings dynamics. Overall, emerging economies are growing faster than the developed world, inflation dynamics are supportive and the US easing in a non-recessionary environment – enough in our view to offset concerns over US election risks. Our metrics show that earnings momentum is strongest for emerging markets and Japan – based on changes to 12-month forward earnings per share forecasts and market breadth.” For the record, the Swiss manager is rather keen on gold, despite the recent rally, and is negative on the euro. With Germany and France’s well publicised political and economic woes, Spy, is not exactly surprised.

Spy has always been a fan of dividends. Companies that pay dividends have real cash flows, not fantasy gymnastics accounting. With that in mind, Spy was not thrilled to read that the S&P 500’s dividend yield has moved down to a measly 1.27%. That ties with Q4 2021, for the lowest yield since 2000. Either share prices have got ahead of earnings or companies are not being very generous, which is not much comfort for income seekers in either scenario.

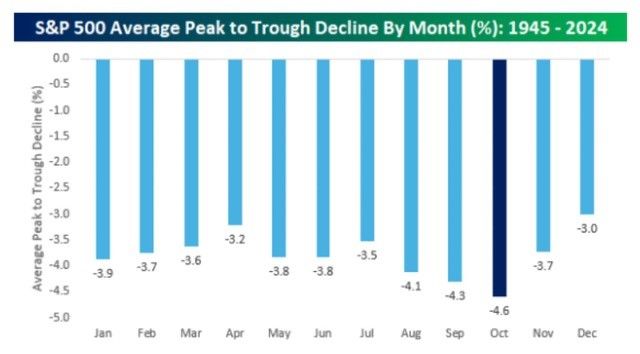

It’s October: ghoulish Halloween lies ahead and therefore a few stories are bound to run around on how this is the scariest month. To be fair, October is historically a positive, but often volatile, month for US stocks. According to data from Bespoke going back to 1945, October has the largest average peak-to-trough decline within the month, at around 4.6%. But as humourist Mark Twain put it, “October. This is one of the peculiarly dangerous months to speculate in stocks. The others are July, January, September, April, November, May, March, June, December, August and February.”

Until next week…