Investors can find better value and upside in Asian AI beneficiaries despite the compelling opportunity in US technology stocks.

This is according to UBS Global Wealth Management (GWM) chief investment office (CIO), which argued that many investors are “overexposed” to the ‘Magnificent Seven’ and other US tech names.

“For investors looking to optimize their tech exposure, Asia also offers a wealth of AI beneficiaries trading at reasonable valuations, including supply chain names exposed to AI edge-computing,” the report said.

A lot of the increased optimism surrounding the investment potential presented by AI development is focused on the AI infrastructure that is required to power it.

UBS GWM for example, expects the AI infrastructure segment to grow to $195bn in 2027, a 50% CAGR from 2022’s $25.8bn figure and much higher than the firm’s previous estimate of 38% CAGR.

“This stronger outlook is also consistent with the guidance from leading AI suppliers in Asia, where we see additional drivers like GPU cloud and AI edge computing on top of strong demand for training and inferencing,” the report explained.

It highlighted that while the AI industry is expected to experience substantial growth, AI edge computing presents new opportunities within the tech supply chain.

Indeed, much of the future growth of AI has been largely forecasted and accounted for in the strong performance of the US technology hyperscalers such as Microsoft, Amazon and Google.

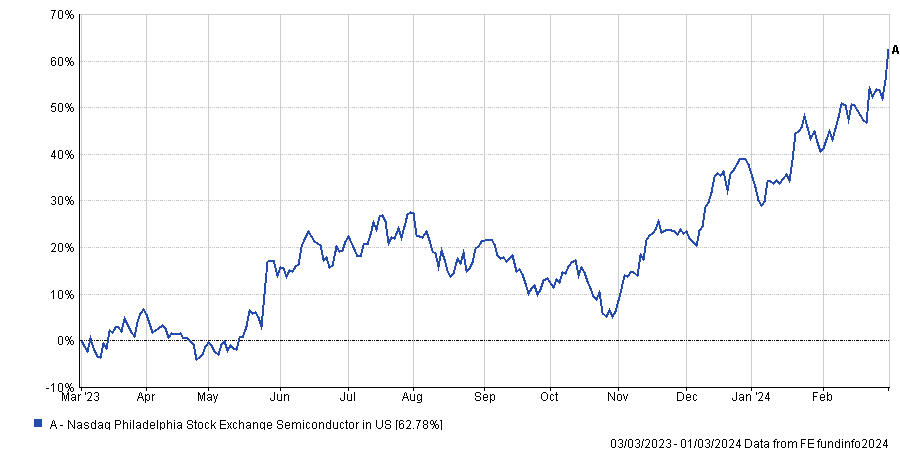

Additionally, the increased demand for AI GPUs has been reflected in the strong performance of Nvidia and other members of the semiconductor supply chain.

Performance of US semiconductors over the past year

Hence, the report said investors looking for the next beneficiary of the future of AI may want to look to Asian companies posed to benefit from the potential growth of end-device AI chips and AI edge-computing.

“While we believe the majority of near-term spending in generative AI computing will focus on data center investments (which are GPU-intensive), we think end-device AI chips and AI edge-computing can provide low latency and personalized generative AI services that are less resource-intensive,” it said.

“For instance, some basic image generation and translation services may not need a model with trillions of parameters, and may instead only require training a few billion parameters. Today, many smaller and dedicated AI chipsets can perform such tasks.”

“We think they can be easily integrated inside end-devices like smartphones and PCs, and other segments like autos and Internet of Things (IoT) devices.”

This is where the authors of the report believe that the ability to process data locally without being exposed to external data security risks “may force” many consumer electronics companies to explore the opportunity in AI edge-computing.

The AI edge opportunity

This is because “they can still participate in the generative AI opportunity by integrating AI edge-computing chips in end-devices,” the report said.

“In certain situations, the ability of edge devices to offload some basic computation from the GPU-intensive cloud-based computation can come in handy.”

Some of the biggest consumer electronics companies in the world, such as Samsung, Xiaomi and Sony, are listed in Asia, and produce the bulk of the world’s smartphones and personal electronic devices.

The report said: “Similarly, we see smartphones and PCs as low-hanging fruit, and select Asia tech supply chain names exposed to these segments should likely see incremental demand.”

“In these consumer devices, we see significant pick-up in the penetration of dedicated AI chips.”

“In the medium- to longer-term, other consumer and industrial devices—including autos—should integrate AI edge chips to take advantage of the proliferation of generative AI applications.”

The authors of the report believe that the revenue from AI edge-computing devices has the potential to reach $30bn in the next five to ten years, a forecast they admitted “may prove to be conservative” given it represents only a low-single-digit share of overall semiconductor industry revenues.