Investors will start to look outside the box to diversify if US Treasuries sell-off during risk-off events, according to Jean-Charles Sambor, head of emerging markets (EM) debt at TT International.

He pointed to a profound change occurring in the correlations between different asset classes in financial markets since Trump’s tariffs were announced.

“You’ve had this very interesting change in correlations across multiple asset classes,” Sambor (pictured) told FSA.

“Usually when you have global risk off, the US dollar is supposed to strengthen, this time, the US dollar weakened. Usually when you have global risk off, US Treasury yields are likely to go down very significantly, and this time, Treasury yields initially went up.”

“This shows that for the first time, US markets are seen as a risk market rather than a risk off market,” Sambor said. “You also had an underperformance of US credit compared to emerging market credit.”

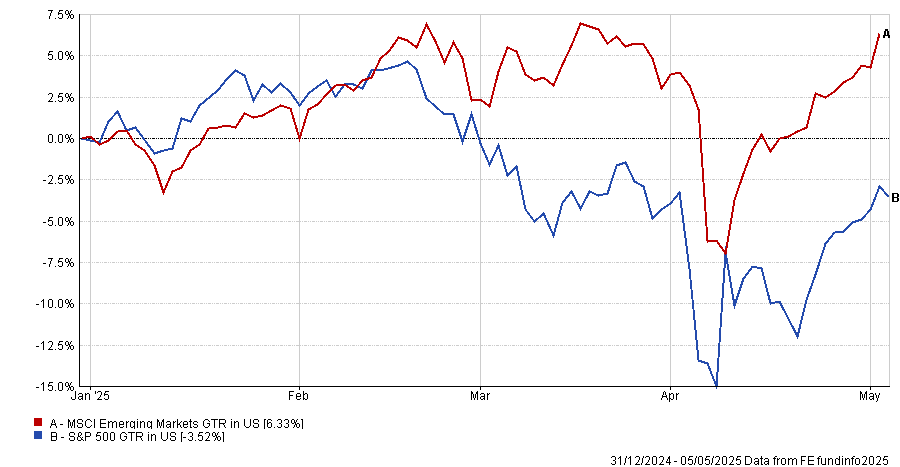

Indeed, year-to-date, emerging market equities have also outperformed US equities, which is not usually the case during a risk-off market (see chart).

Sambor said the main driver of US Treasuries behaving differently is the market starting to question the long-term outlook for the US economy.

There is growing uncertainty surrounding US trade policy and fiscal policy, with some commentators debating the US currency’s role as the world’s reserve currency.

All of this has major implications for asset managers, according to Sambor, who believes will start to look for more diversification if US Treasuries no longer provide the same cushion during risk off events.

He argued that this change in correlations between asset classes will likely spark a wave of money from asset allocators over-exposed to the US to search for a new home.

He said: “The marginal seller of risk is coming from the US, it’s not coming from emerging markets and that’s very, very new.”

“I think that emerging markets could have its moment. Initially money will go back to Europe, but the second wave will be investors saying: ‘give me anything without a dollar sign in front of it’ and emerging markets will benefit.”

While most investors agree that global trading relationships are being re-written, economic uncertainty is increasing and geopolitical risks are as high as they’ve been for decades, most portfolios don’t necessarily reflect these views, argues Sambor.

“People will 100% agree with you when you say we are living in a multipolar world. Nobody will challenge you. But when you ask if their portfolio reflects this multipolar world, they will say all their exposure is to the US.”

“Whereas if you look at the outlook for emerging markets, it has deteriorated but it’s much better than developed markets,” he added.

“Fiscal deficits are lower, interest expenses are lower, public debt to GDP is extremely low. Growth could slow down but it’s still better than most DM markets.”

While Sambor isn’t necessarily saying it’s a rosy picture in emerging markets, because there are risks posed by a global downturn, he believes the balance of payments and fiscal outlook much more supportive than developed markets.

“People say when the US catches a cold, EM goes to hospital. I think this time that it’s unlikely” he said. “Yes, EM will slow down, but EM should be way more resilient than US and Europe.”