According to some reports, Credit Suisse is losing about 200 bankers per week as the fallout from its shotgun marriage to UBS continues to reverberate. Across the Atlantic, Goldman Sachs says it going to be downsizing and sacking staff. Combine that with thousands of well publicised tech lay-offs and one could almost get the impression the world is falling apart. And yet, before we all fall into the “we are all doomed” mindset, Spy was reassured this week to speak to several asset managers and wealth managers in Hong Kong and Singapore, who all said the same thing: they are desperate to hire more people and are finding it hard to get the talent. Here in Asia, at least, there are plenty of jobs to go around. And that bodes well for the years ahead for our industry and our economy.

What’s the old saying? You wait for ages for a bus and then two come along? Spy has seen several ETF providers offering “buffered” strategies. If you think this would be something to do with gyms, you would be much mistaken. These are time-targeted, risk-minimising funds which aim to protect the downside, offering capped upside, within a specific time frame. While that sounds good, Spy is reminded of structured products that proliferated about a decade ago promising protection to investors using complex options and derivatives strategies. What they all had in common was rather juicy fees and a tendency to blow up when a black swan event happened that the model said was a “nine-delta” outside chance. For the brave of heart, look at Allianz Investment Management’s ‘Buffered’ ETFs or First Trust Advisors ‘Target Outcome’ range.

Talking of ETFs, Singapore and Shanghai announced this week that they have signed an MoU to build a link between their respective ETF markets. The SSE-SGX ETF Connect will hopefully boost liquidity and provide easier access to each other’s listings. SGX has already done something similar with Shenzhen. Three ‘feeder’ ETFs, CSOP CSI Star ETF, CSOP ChiNext 50 Index ETF and UOBAM Ping An ChiNext ETF have already come to the market in Singapore via that route. Slowly, but surely, China continues the internationalisation of its financial markets as depth and connectivity increase in every direction.

With the news this week that Franklin Templeton is buying Putnam Investments for $1bn, Spy had a look at their shares since their last big acquisition. The purchase of Legg Mason closed in September 2020 and Franklin Resources (BEN), the listed parent holding company, was trading at about $21.50. Today they are just $3 higher at $24.50. While Spy will happily acknowledge that the result has not been value destroying, it has hardly been transformational either. The Putnum portfolio is definitely complementary, with a range of alternative strategies joining the stable. Time will tell if this adds much fire to BEN’s own share performance.

Artificial Intelligence stocks and those deemed to most likely benefit have certainly put some fuel into the equity markets of late. Nvidia’s brief valuation jump above $1tn the most notable. Spy is absolutely convinced there is plenty of frothy bubbliness in the air. He is reminded of Bill Gates’s most prescient saying, “Most people overestimate the utility of a new technology in the first two years and underestimate it over the next 20.” In other words, expect a lot of ridiculous, over-hyped successes and some dramatic failures and then, in time, some massive long-term winners to emerge. Investors may be desperate to invest in AI companies, but some of the biggest leaders from the AI revolution will be existing firms that weren’t created for AI but are in fact positioned to exploit it. In a similar paradigm, Tesla has exploited the advances in lithium batteries.

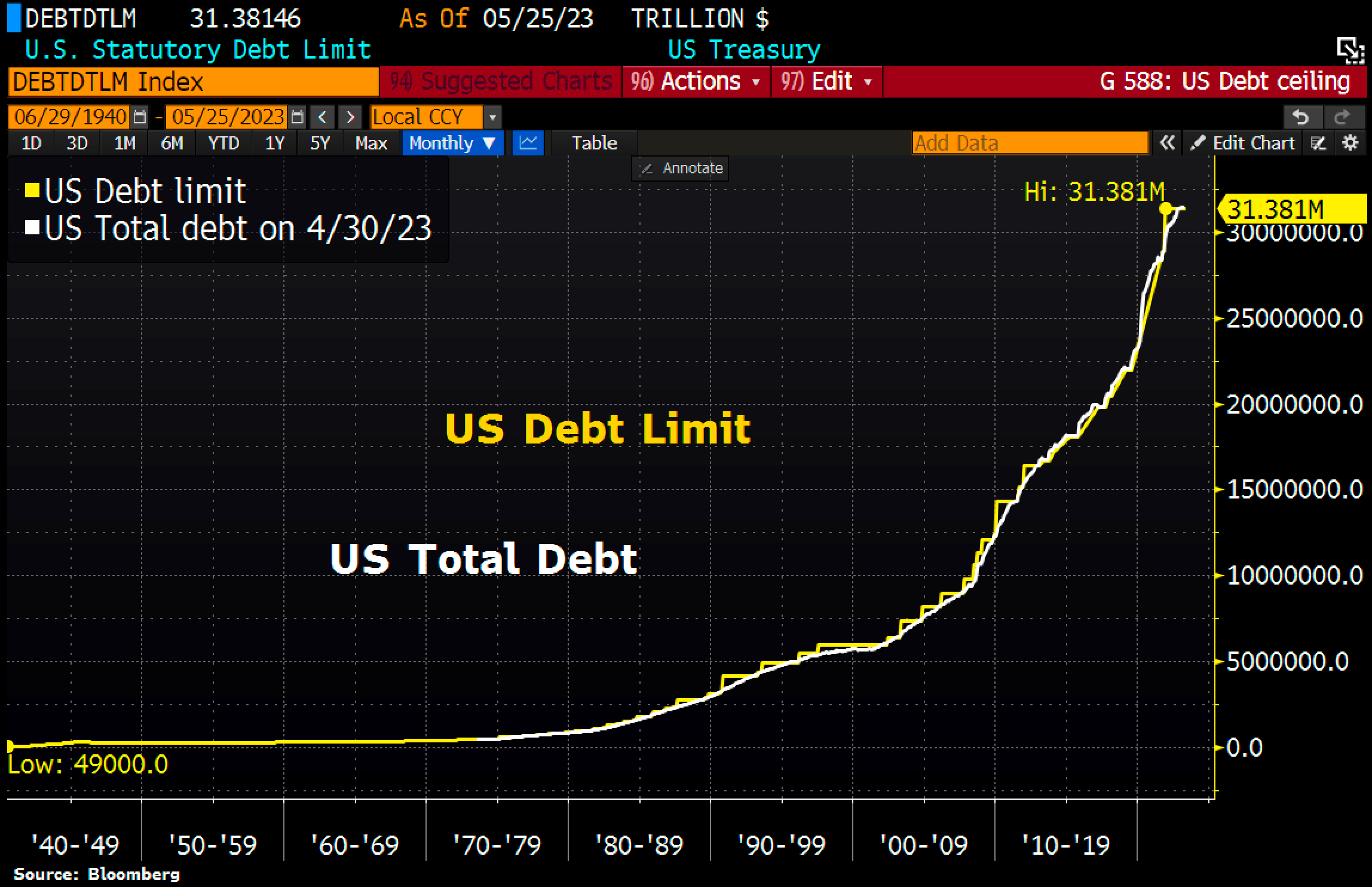

As Spy comfortably predicted, the US debt ceiling is being raised as the Biden – McCarthy deal makes its way through Congress. This was always political drama and not a realistic possibility of genuine default. Spy does have to hand it to the American government, it certainly knows how to fill the Federal ‘credit card’ quickly. Take a look at this chart below. It plots the US Debt Limits vs Total US Debt. The moment the limit is raised the spending follows suit, like clockwork. It is almost as if the US government believes Oscar Wilde was correct when he wrote, “Anyone who manages to live within his budget suffers a lack of imagination.”

Talking of debt, the American consumer is also choking on debt, notes Spy. Total credit card debt in the United States has reached $1trn for the first time. The average American family now holds $10,000 in credit card debt and 40% of Americans now have more credit card debt than savings. Some nice Friday numbers: US Household Debt: $17.1trn, US Mortgage Debt: $12trn, US Car Loans: $1.6trn, US Credit Card Debt: $1trn. Heart-warming in age of rising rates.

Quietly in the background, the Evergrande saga continues to rumble ominously. Caixin reported this week that a subsidiary of Evergrande Group has failed to repay debt investors in its wealth management products a previously promised amount. The reason for the non-payment? A lack of cash. That old chestnut. Chinese investors continue to learn a valuable lesson in credit quality.

Spy’s quote of the week, which should probably be plastered on the wall of every single financial adviser is, “The most valuable personal finance asset is not needing to impress anyone.”

Until next week…