It is a quiet week in Asia due to the Lunar holidays, but Stephen Roach, the former chairman of Morgan Stanley in Asia, ruffled a few feathers with his op-ed in the Financial Times this week suggesting that “Hong Kong is over”. Roach’s core point is that with a tighter political environment in Hong Kong, the territory’s domestic capacity to solve some of its woes are more limited and the local stock market’s dire performance over the last decade reflects that malaise. Spy has heard many private and public comments to the effect, “Ah, but Hong Kong will adapt, it always does.” That is very true but that is not really Roach’s point, is it? Hong Kong has been extraordinarily special for a century, just as Vienna was in its heyday of the dominant Habsburg empire. In Europe, Vienna remains a beautiful and great city but its “moment” of dominance has passed. Roach fears Hong Kong’s moment has passed too and Spy, looking further south to Singapore,worries that he might just be right, too.

Spy is old enough and certainly ugly enough to remember the Dot Com boom in the late 1990s and early 2000s. Having lived through that period of “irrational exuberance” and the traumatic aftermath, the warning signs of a bubble in the AI space are now flashing everywhere. Artificial intelligence has enormous promise and application; that is not really in question. What must be doubted is that every company vaguely connected with AI is suddenly worth vast amounts more than it was before. Nvidia became America’s third most valuable company this week, overtaking Amazon and Alphabet. At least Nvidia makes things people want to buy – i.e. chips to power AI applications. What Spy can’t countenance is the fact that disclosures that Nvidia owns tiny stakes, in marginal companies, has sent their stocks soaring. Take one example, SoundHound, which supposedly uses AI to process speech and voice recognition, jumped 67% on Thursday, after Nvidia revealed a stake that amounted to a relatively small $3.7m at the time of the filing. Nvidia invested in SoundHound in 2017 as part of a broad $75m venture round – not exactly betting the farm on the firm. This kind of blind buying is unlikely to end well. Yes, there will be huge winners, but most firms in the AI space will either go bust or fail to deliver. This smacks of a dramatic case of FOMO.

Just as the US and Europe are grappling with all things ESG and ‘sustainability’ due to a widespread political backlash on the ground, China throws its hat in the ring. The Shanghai and Shenzhen stock exchanges and the Science and Technology Innovation Board market have adopted ESG disclosure requirements forcing companies to reveal their ESG information, including Scope 3 emissions and scenario analysis, by April 30, 2026. “Companies are now required to provide comprehensive disclosures on issues such as biodiversity, climate impact, corporate governance and sustainability practices. A key innovation is the concept of ‘double materiality’, which weighs both the financial impact of ESG factors on the company and the company’s impact on society and the environment.” reported BNN. China may be late to the party but at least it has shown up even if the dance floor looks littered with discarded punch glasses.

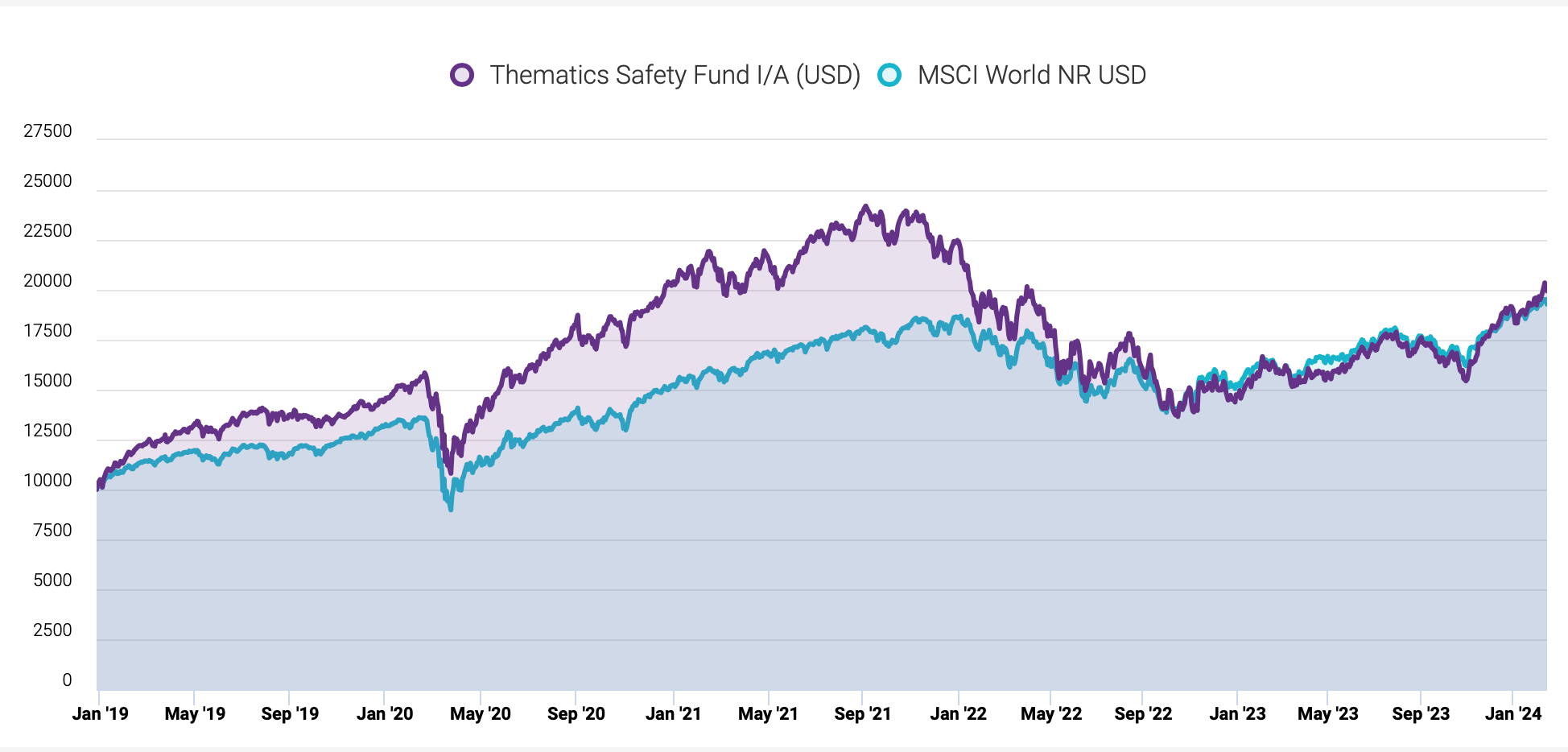

Spy loves a good thematic fund. Trying to capture the value of a trend or theme that runs throughout a marketplace seems like a great idea. The problem is that all too many thematic funds don’t outperform over the long term. Take Natixis’s Safety Fund. The strategy “invests in companies that offers products and services for the physical and digital protection of individuals, businesses and governments.” With war taking place in several hotspots across the globe and digital security never being more important, Spy would expect a fund like this to blow the lights out. However, five years from launch and the strategy has merely equalled its benchmark. To be sure, it has performed fine, but delivered real alpha, not so much.

Private equity’s allure for high-net-worth investors has been obvious for a while. And, looking at the numbers, it is hard not to see why. According to Tony Robbins (esteemed financial author), if one had a million dollars and invested it in the S&P 500 35 years ago it would be worth $26 million today. Take the same million, the same 35 years, and put it in private equity and it would be worth a staggering $139 million. Spy is not sure how that calculation is made but if it is anywhere close to accurate, the democratisation of PE can only be a good thing.

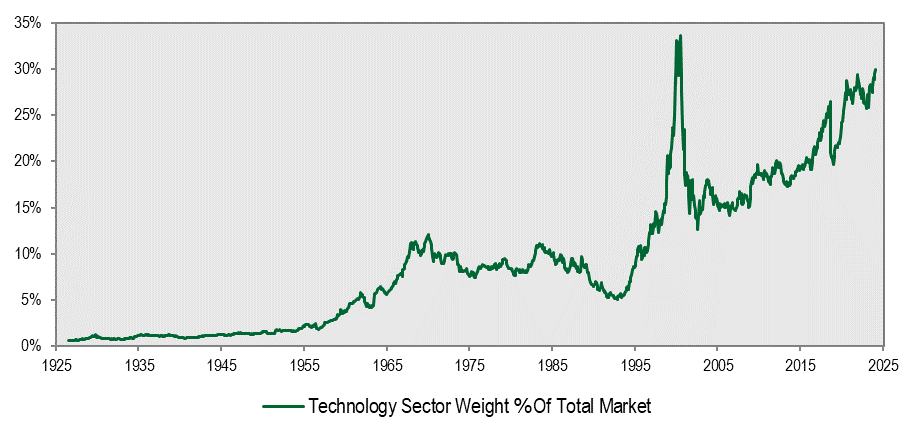

Worried about concentration? Perhaps we all ought to be. The S&P 500 technology sector is now 29.9% of the total S&P 500 index. Looking back at nearly a hundred years of S&P history, the number has never been so high.

Fun Friday fact: John D. Rockefeller’s estimated $1.4bn net worth in 1937 was equivalent to 1.5% of US GDP when he died. Elon Musk is currently worth about $199bn and America’s GDP was $27.36trn in 2023. That makes Musk only half as successful as Mr Rockefeller at 0.72% of America’s GDP (at the moment).

Until next week….