“Are you not entertained?” shouted Russell Crowe as Maximus Decimus Meridius in Gladiator. Watching the Trump administration pirouette on policy and tariffs, making a fool of market timing investors and experts alike, Spy could not help but have the image of the Roman Coliseum replete with the baying mob this week. The only thing that has tamed the administration’s madness is the bond market, enough to intimidate a gilded, spoilt emperor, drunk on his own delusions of grandeur and omnipotence. To paraphrase Maximus, “Volatility smiles at us all. All a man can do is smile back.”

Lazard Asset Management has joined the active ETF trend, notes Spy. Its small, but growing, portfolio includes Equity Megatrends (THMZ) and Japanese Equity (JPY) and, as of this week, a Next Gen Technologies ETF, trading under the ticker TEKY. (Which Spy rather does like.) However, if you were looking for some names you have never heard of, don’t bother with the fund’s top ten holdings, despite the blurb saying, “Lazard Next Gen Technologies ETF seeks to invest in the innovation leaders across the AI Tech Stack that will enable the next generation of automation applications.” Microsoft and Nvidia are, predictably, the top two positions. In Spy’s opinion, the most unlikely stock in this rather concentrated portfolio is Mastercard, which is the fund’s ninth largest holding.

Talking of active, Goldman Sachs Asset Management is convinced that active’s moment has arrived (again), reckons Spy. In an outlook note, the investment giant points out, “Active ETF strategies have outperformed across all asset classes over the past year or so, and in relatively inefficient markets, like small caps and fixed income, active ETFs have delivered consistently superior returns for the last 10 years.” This is certainly different to the narrative pushed by many passive zealots. Their strategists do freely admit, “The main exception is in the large cap space, where excessive concentration and extended valuations make it difficult to generate alpha in excess of benchmarks.” Passive for US large cap, active for everything else seems to be the mantra.

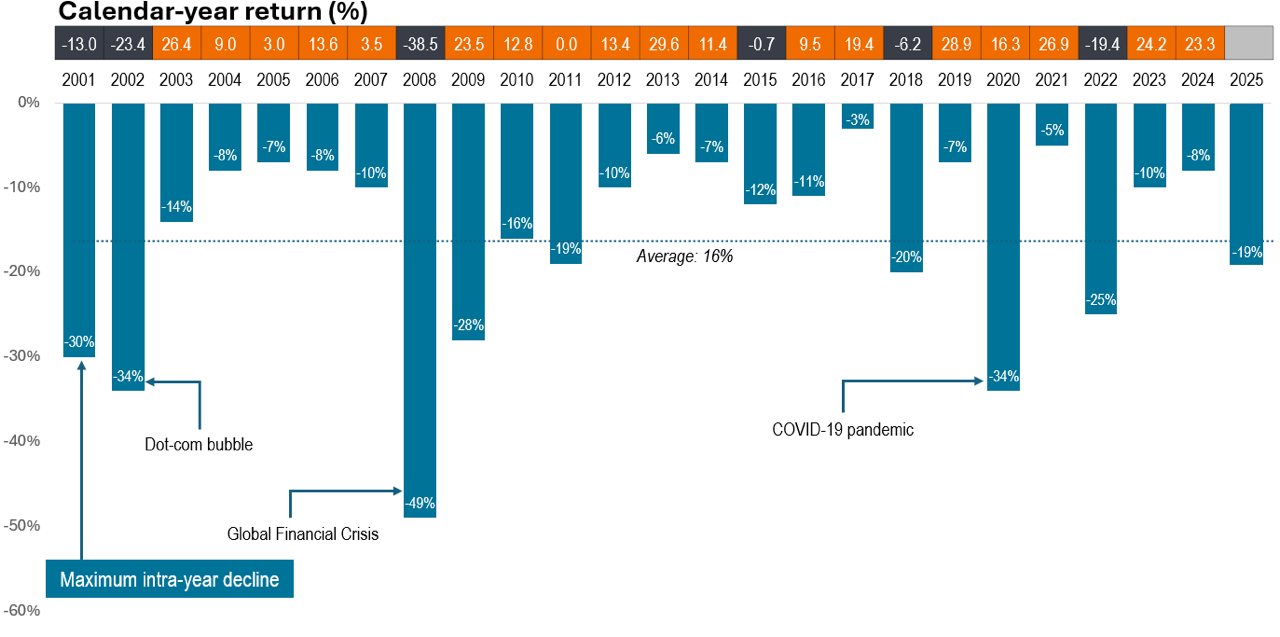

For those feeling the white heat and sweat-inducing pain of market volatility, this rather glorious chart from Janus Henderson Investors may help to calm the nerves, thinks Spy. Ben Rizzuto writes, “Investors must remember that the present is a magnifying glass. The feelings we experience during market declines – and during rallies, for that matter – tend to be outsized compared to what’s really happening, and the big picture gets lost in the moment. This chart reminds us that even though declines happen frequently, the market has grown substantially over the long term.” Nailed it.

In a thoughtful piece worth reading in full, M&G Investments is helping investors see alternative opportunities that come with advances in technology but is not the technology itself. Alex Araujo, fund manager in M&G Global Listed Infrastructure, refers to a kind of Jevons Paradox in the electricity market. “The new economy, characterised by cutting-edge technology companies, needs the old economy’s power grids, transportation networks and manufacturing facilities to thrive. Despite this interdependence, investors are predominantly channelling their funds into the new economy, often overlooking the critical investments needed in the old economy to sustain this growth.” Opportunity is everywhere, if we look at it in the right way.

Psst, wanna buy a company? According to Bain & Company there are now a whopping 29,000 unsold companies owned by the private equity (PE) industry. Adding further pain, the buyout industry has about $1.6trn in “unspent capital” — what the industry likes to call “dry powder” — waiting to be deployed, according to Pitchbook. Much of that money, about 24%, has not found a home for four long years or even longer. The PE industry has been so successful at raising money, it has an embarrassment of riches and hardly anywhere to put it. Investors hoping for quick returns may be in for some disappointment, reckons Spy.

In Shakespeare’s Hamlet, Polonius utters the immortal words, “Neither a borrower nor a lender be, for loan oft loses both itself and friend, and borrowing dulls the edge of husbandry.” This timeless wisdom springs to mind when it was revealed this week that Americans are not paying back their credit cards in record numbers. In the fourth quarter, 11.12% of credit-card accounts were only making the minimum payment, up from 10.87% in the third quarter, according to the Philadelphia Federal Reserve data. Spy’s sophisticated readers will know that this foolishness is a road to penury. Spy supposes when you have a reckless government, that halfway through its fiscal year in 2025, has already increased its budget deficit by $1.3trn, a $2.6trn annual rate, equalling a mind-blowing 9% of GDP, what do you expect? Monkey see, monkey do.

Spy’s quote of the week from wealth manager, Peter Mallouk, “Bad investors sell in markets like this. Good investors get nervous but hold. Great investors are completely unfazed. The best investors get excited about potential opportunities.”

Until next week…