Kevin Anderson, State Street Global Advisors

Even with the imminent availability of a Covid-19 vaccine, markets face the prospect of a short-term burst of growth, followed by some uncertainties, as policymakers attempt to wean economies off the monetary and fiscal stimulus which helped bolster risk markets last year.

In this environment, SSGA favours growth and quality assets, particularly those in the US and China.

“We prefer growth and quality assets to value stocks in light of uncertainty regarding fiscal stimulus and persistent geopolitical risk, and believe investors will be most likely to find them in North America and in China,” Kevin Anderson, head of investments, Asia Pacific at SSGA, told a recent media briefing.

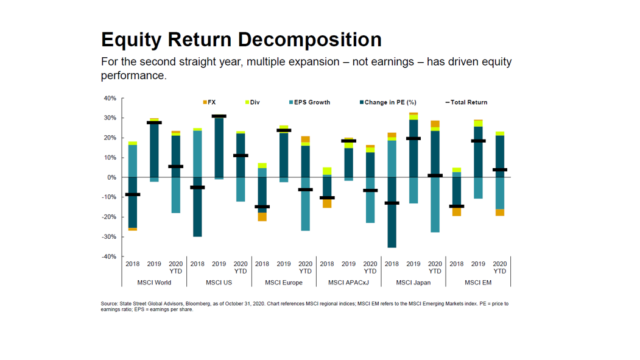

However, although the equity risk premium continues to favour exposure to equities, “there is limited room for additional [price-earnings ratio] multiple expansion, which has driven equity performance during the past two years”.

“Instead, earnings must come through to support continued market performance, because the liquidity created by quantitative easing will be insufficient to sustain the upward trend,” said Anderson.

SSGA expect the US and China to generate the strongest earnings expansion, with Chinese equities also experiencing a shift towards growth features, underpinned by consumption and digitalisation trends.

“China will be the only large economy to see positive GDP growth in 2020, likely around 2.5%, but this positive outlook should be tempered with caution over the longer term given high debt levels, deteriorating demographics and ongoing geopolitical tensions potentially posing challenges,” said Anderson.

“We expect earnings growth in China to be especially resilient, and the Chinese growth and consumer stocks most appealing. We also believe that Chinese fixed income assets and the renminbi are very attractive, given the yield pickup and because we see room for further currency appreciation,” he said.

Meanwhile, the US is forecast to face less marked GDP contractions than many other developed economies, at an expected 3.7%, compared with more acute declines of 9% in the UK and 7% in the eurozone.

Among other asset classes, SSGA is overweight US corporate credit, because “spreads will be supported by the Federal Reserve’s purchase programmes”, but underweight US Treasury bonds because “quantitative easing will keep rates rangebound”.

Elsewhere, emerging market currencies are poised to outperform, according to SSGA.

“They are priced at one of the steepest discounts we’ve seen in two decades relative to the US dollar, and they offer value relative to most major developed market currencies. In addition, domestic emerging market debt provides investors with attractive income compared with US Treasuries,” said Anderson.

“In particular attractive yields [more than 3% for the 10-year bond] and demand pull from index inclusion suggest investors should add Chinese bonds,” he said.

RISKS OF NORMALISATION

However, SSGA warns that although it is comfortable with its expectations for a strong economic rebound in 2021, the firm is increasingly focusing its sights on “everything that comes after that surge”.

In its mid-year global market outlook, released in August 2020, SSGA compared the Covid-19 pandemic to a relay race, with multiple overlapping stages.

Global economies have now transitioned from a successful stage one (the injection of monetary and fiscal stimulus) to stage two – an economic reopening as lockdown restrictions in some places eased, according to Anderson.

“With the outlook for a vaccine increasingly positive and the first vaccinations rolling out imminently, an exit from stage two looks increasingly likely. But, at some point, economies will need to transition back to autonomous growth, independent of monetary and fiscal stimulus. The adjustment is certain to be complex, and it is very likely to cause some market turbulence along the way,” he said.

As a hedge against volatility and future shocks, SSGA recommends tactical allocations to gold, duration, cash, and defensive equities.