The burgeoning days of the smartphone were led consecutively by Palm, Blackberry and HTC. Designing from scratch, the trio created innovative products that were far superior to anything offered by the legacy feature phone makers at that time. They also exploited the then nascent microchip technology to marry the latest hardware and software capabilities. As advances in chip technology lowered the barrier to entry, however, their first mover advantages dwindled. Eventually, the smartphone world became dominated by Apple’s iOS and Google’s Android. In the latter camp, the scale and vertically- integrated components of Samsung allowed them to prosper, with the rest of the market squeezed out by the low-cost Chinese players.

The automotive industry is undergoing a similar revolutionary transition to electric vehicles (EVs). The incumbents have proved reluctant to embrace this trend, given their internal combustion engine (ICE) business models; belatedly, they are now reacting. But like their feature phone cousins, this has often been compromised by trying to repurpose an ICE design and supply chain to EVs rather than starting with a blank slate. Tesla’s Model 3 was a wake-up call to the industry. Now we are seeing automakers go all-in on EVs, with bold future targets.

Impact on automakers as EVs evolve

As the EV industry grows and matures, the sustainability of Tesla’s initial advantages and long-term implications for the industry remain to be seen. Merchant battery cell makers are rapidly closing the gap with Tesla, while VW and Ford have announced ambitious plans to vertically integrate batteries. Naturally, as battery densities improve and EV range extends, consumer ‘range anxiety’ will fade. This will also negate the need for a proprietary charging network that will also become increasingly standardised.

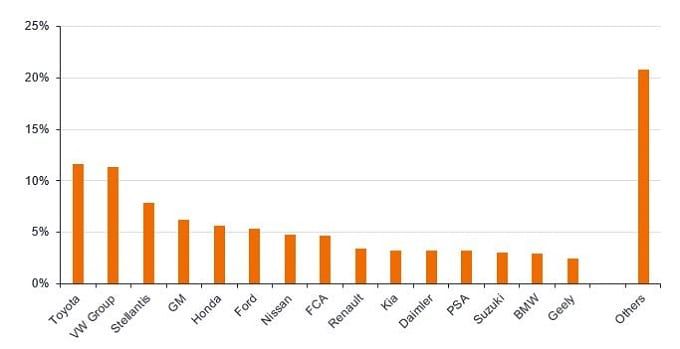

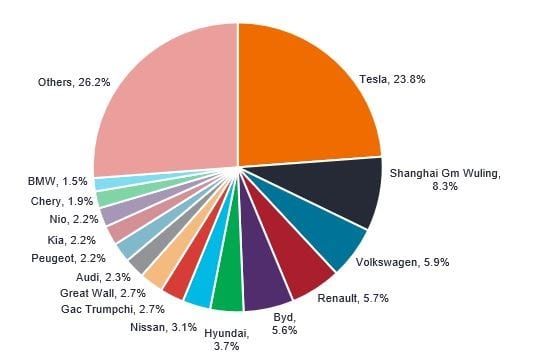

Incumbent automakers have finally recognised the need for better EV design, resulting in high quality new EV models emerging. Bringing to bear their existing manufacturing scale and expertise, costs are also coming down rapidly. Consequently, Tesla has been losing market share in the US and Europe. In today’s ICE market, no automaker has more than 15% market share and it remains a highly fragmented market (Figure 1). Tesla today is in the lead with 22.6% share in the nascent EV market (Figure 2). But with a plethora of EV models being launched by incumbent automakers and a host of new EV start ups emerging globally, the sustainability of Tesla’s lead is debatable. Meanwhile, the rumoured entry of Apple into the market only clouds the picture further.

Figure 1: Global auto market share in 2020

Figure 2: A fragmented market: global EV market share in 2020

Investing in sustainable transport

Perhaps the most important takeaway from the smartphone era is to focus less on the hardware. In the same way smartphones have become fairly commoditised, it is likely that so too will EVs. The car will become yet another client for the delivery of internet services. As such, controlling the operating system and therefore gateway to these EV clients will be key, in the same way it was for Microsoft in the PC and Apple and Google in the smartphone eras. Will that be open source like Android or a walled garden like Apple has created? If the latter, will Tesla or a new entrant become dominant? Will the automotive incumbents successfully pivot their companies to be software centric?

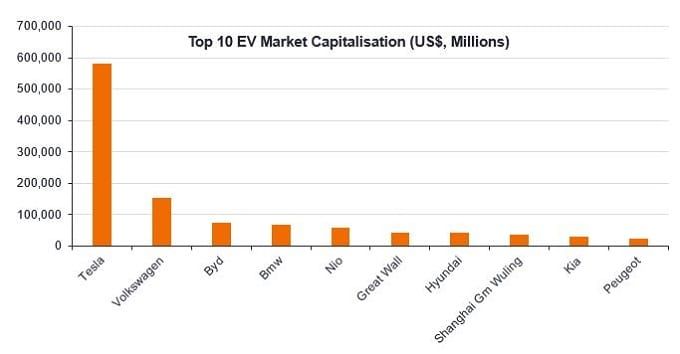

Figure 3: The battle for EV dominance

Suppliers who can provide electrification reference designs will reduce time to market and enable new entrants in the same way as their smartphone forefathers. Power semiconductors are essential for the power management and charging of EVs, as is central processing power and a new ethernet networking architecture for autonomous driving.

As with smartphones, betting on the winning EV brand is difficult and competition is fierce. But there are opportunities to invest in key EV suppliers that are agnostic to which EV brands do well and have high barriers to entry and attractive margins. The road to a more sustainable future presents attractive investment opportunities for those who know where to look and learn from history.

Disruption and innovation are accelerating. Let Janus Henderson help you harness the power of change and stay on the right side of disruption. Find out more for Hong Kong and Singapore.

Glossary

Reference design: refers to a technical blueprint of a system, which third parties may enhance or modify the design as required. Electrification car design is driven by consumer needs and incorporates aesthetics and style, performance and drivability, and comfort and connectivity.

Commoditised: when goods or services become relatively indistinguishable from rivals and are only differentiated by price tags.

Important information

The views presented are as of the date published. They are for information purposes only and should not be used or construed as investment, legal or tax advice or as an offer to sell, a solicitation of an offer to buy, or a recommendation to buy, sell or hold any security, investment strategy or market sector. Nothing in this material shall be deemed to be a direct or indirect provision of investment management services specific to any client requirements. Opinions and examples are meant as an illustration of broader themes, are not an indication of trading intent, are subject to change and may not reflect the views of others in the organisation. It is not intended to indicate or imply that any illustration/example mentioned is now or was ever held in any portfolio. No forecasts can be guaranteed and there is no guarantee that the information supplied is complete or timely, nor are there any warranties with regard to the results obtained from its use. In preparing this document, Janus Henderson Investors has reasonable belief to rely upon the accuracy and completeness of all information available from public sources. Past performance is no guarantee of future results. Investing involves risk, including the possible loss of principal and fluctuation of value.

Not all products or services are available in all jurisdictions. This material or information contained in it may be restricted by law, may not be reproduced or referred to without express written permission or used in any jurisdiction or circumstance in which its use would be unlawful. Janus Henderson is not responsible for any unlawful distribution of this material to any third parties, in whole or in part. The contents of this material have not been approved or endorsed by any regulatory agency.

Any reference to individual companies is purely for the purpose of illustration and should not be construed as a recommendation to buy or sell or advice in relation to investment, legal or tax matters.

Issued in (a) Singapore by Janus Henderson Investors (Singapore) Limited (Co. registration no. 199700782N) licensed and regulated by the Monetary Authority of Singapore. This advertisement has not been reviewed by the Monetary Authority of Singapore. (b) Hong Kong by Janus Henderson Investors Hong Kong Limited, licensed and regulated by the Securities and Futures Commission. This document has not been reviewed by the Securities and Futures Commission of Hong Kong. We may record telephone calls for our mutual protection, to improve customer service and for regulatory record keeping purposes.

Janus Henderson is a trademark of Janus Henderson Group plc or one of its subsidiaries. © Janus Henderson Group plc.