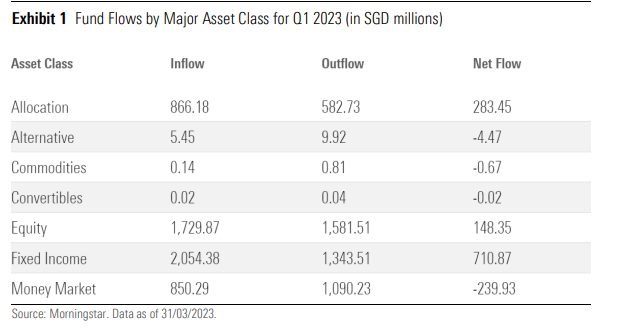

Net inflows for authorised and recognised unit trusts in Singapore came in at S$897.58m ($666.01m) in the first quarter of the year, down from the S$4.86bn posted in the last quarter of 2022.

A key contributor to this year’s figure was the S$710.87m in net subscriptions received under fixed income. This comes as the asset class saw inflows and outflows of S$2.05bn and S$1.34bn respectively.

Other major asset classes that reported inflows included allocation and equity. Allocation funds reported subscriptions of S$283.5m. Most of these funds came from the moderate allocation category, which collected S$310.6m during the quarter.

Meanwhile, net flows for equity funds stood at S$148.35m in 1Q2023.

For reference, major global stock markets closed the first three months of 2023 with broad gains. The Nasdaq Composite led the board with a 16% rebound, while Euronext Paris CAC 40 and FSE DAX, the benchmark indexes for France and Germany, respectively, also recorded double-digit gains. These two European markets were closely followed by Taiwan’s TSEC TAIEX PR TWD, up 12.24%.

In the United States, the market’s focus was initially on the Federal Reserve’s next moves in tackling the uncomfortably high levels of inflation and a red-hot job market.

“As the quarter headed into its final days, the collapse of Silicon Valley Bank stirred concerns about a credit crunch and investors’ focus shifted dramatically to the health of the banking sector,” IMAS and Morningstar wrote in their report. They add that tech stocks were the outperformers in 1Q2023, rallying on better-than-expected earnings results and demand, effective cost-cutting strategies and enthusiasm for artificial intelligence.

In this time, the S&P 500 index returned 7.03%, while the DJ Industrial Average was little changed. European markets also staged a rebound, recouping a large part of the losses posted last year.

Meanwhile, global large-cap blend equity funds and US large-cap blend equity funds ranked ninth and tenth, receiving net inflows of S$20.24m and S$13.56m, respectively.

“Among global strategies, large-cap growth equity funds posted the biggest outflows for the quarter. Investors also redeemed capital from value-oriented global and US strategies, however, US large-cap value equity funds reported outflows of S$25.02m while their global counterparts reported mild net outflows of S$6.92m,” IMAS and Morningstar said in their report.

Against this backdrop, sentiment for thematic equity strategies was seemingly mixed with investors favouring equity funds and selling off units in healthcare, alternative energy, financial services and natural resources-related funds.

The Asia-Pacific ex-Japan Equity and China Equity A-shares topped Morningstar’s equity fund categories with net flows of S$178.44m and S$63.12m respectively.

Conversely, the Asia ex-Japan Equity and Global Large-Cap Growth Equity funds were amongst the lowest in the same category, following net outflows of S$62m and S$44.29m.

Money Market Fund Flows

Another asset class that continued to post net outflows in the first quarter was money market funds. Investors’ redemptions of these cash management products as well as outflows from Asia money-market and the miscellaneous money market category led to S$293.93m in net outflows.

Meanwhile, excluding global and US fixed-income funds, all bond categories recorded outflows this quarter. Asia fixed-income funds continued to record the largest redemptions, as the category group ended the quarter with negative net flows of S$209.78m after the fourth quarter’s S$327.98m outflows. Emerging markets and Europe fixed-income funds posted small negative flows of around S$3m.

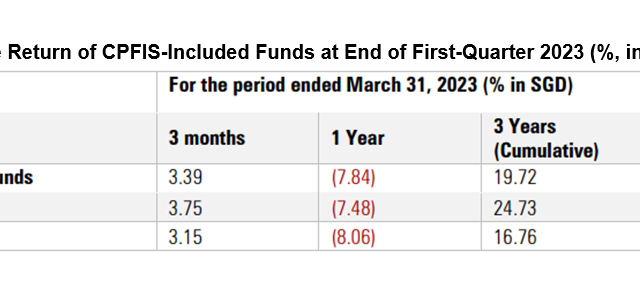

The overall performance of CPFIS-included funds (unit trusts and ILPscombined) was up 3.39% in the first quarter of 2023, versus the fourth quarter’s positive return of 2.53%. Over the one-year period through March 2023, the CPF averaged a loss of 7.84% and a positive return of 19.72% on a cumulative basis over the past three years.

During the quarter, all asset classes finished with a gain. Equity CPF funds registered a 4.01% gain and bond funds a 1.82% gain, while allocation funds were up 2.76%. Money market funds ended with a 0.98% gain.

Over the past year, equity, bond, and allocation funds all notched negative returns. Equity funds took a more severe hit as negative returns dipped to nearly 10%. Fixed income and allocation funds reported average negative returns of 3.73% and 7.19%, respectively.

Outlook

A weaker economy – both in the US and in many countries globally – as well as high inflation levels is expected to give room for the Federal Reserve ease monetary policy at the end of the year.

The central bank had begun tightening monetary policy in 2022; the federal-funds rate has risen to a range of 4.75% to 5% from zero.

With this in mind, analysts from Morningstar reckon that “investor sentiment could oscillate between positive news that hits the tape and unfavorable economic metrics releases,” in the near term.

“The market will need to see a turnaround in leading economic indicators to break through the top of this range and rally up toward where we see fair value. For investors with a long-term investment orientation, there is enough margin of safety in the market to use selloffs to judiciously add to equity exposures,” they said.

“If global growth slows, and it will likely manifest itself in weak demand for Asian goods and lower export figures to those selling to the US and Europe. The full brunt of this slowdown has yet to come to fruition and some disappointment could occur in the market,” the analysts said, adding that companies in industrials and some tech names, especially for companies whose orderbooks undershoot expectations, will be the first to feel the pain.