Claudia Calich, M&G Investments

During the worst of the sell-off in risk assets in March 2020, as investors absorbed the possible impact of the coronavirus pandemic on economic activity, yield spreads of high yield emerging market bonds spiked to 1,200 basis points (bps). The premium over US treasury yields was wider even wider than during the worst days of the global financial crisis in 2008, Bloomberg data shows.

Spreads have narrowed substantially as risk appetite returned in response to aggressive monetary stimulus policies by major central banks and as governments throughout the world embarked on massive debt-fund spending.

However, current average spreads of 608bps remain well above the low of 200bps seen in May 2007, and wider than the pre-pandemic panic level of 500bps.

“Continued monetary and fiscal support amid clear signs of economic recovery as vaccines are rolled out provide an encouraging environment for many emerging markets,” Claudia Calich, a fund manager at M&G Investments told a media event on Wednesday.

“Demand for the asset class remained strong at the start of this year, as evidenced by a further tightening of spreads in January despite a high level of new issuance,” she said.

Yet, several high yield [sub-investment grade] sovereign debt issues have room to rally further, having lagged investment grade issues, according to Calich.

“Investment grade issuers look relatively rich, in our opinion, so we favour exposure to higher-yielding issuers,” she said.

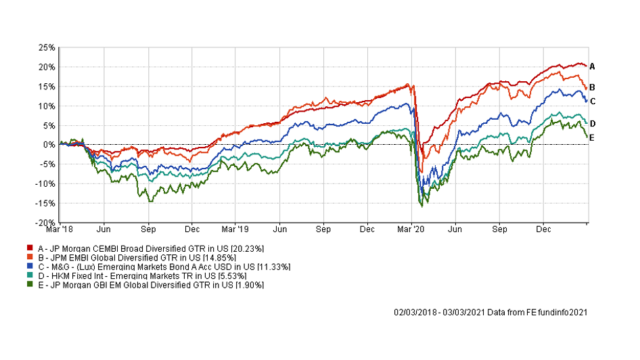

Calich manages the $2.8bn Luxembourg-domiciled M&G Emerging Markets Bond Fund, which has generated a three-year cumulative return of 11.3% (in US dollars). It has outperformed the average 5.53% by emerging market bond funds available in Hong Kong, but has done less well than the 12.32% return by its benchmark of three equally-weighted JP Morgan indices, according to FE Fundinfo.

The fund had an annualised volatility of 9.81% during the period, slightly higher than its peers (9.57%), but lower than the JP Morgan GBI EM Global Diversified index (11.04%) and the JPM Global Diversified index (10.24%), FE Fundinfo shows.

The portfolio’s largest individual country holdings include Russia, Mexico, South Africa, Brazil and Indonesia, and 26% is allocated to emerging market corporate credit, according to the January fund factsheet.

The fund has also bought rare sovereign issuers, including Armenia and Benin, while managing to avoid some of the worst-performing borrowers, such a Belize, Ethiopia and Lebanon.

Callich has continued to increase exposure to local currency debt this year. About 65% of the fund is allocated to US dollar-denominated bonds, but 26% is invested in local currency emerging market government bonds, which is two percentage points above the benchmark weight.

M&G Emerging Markets Bond Fund vs sector average and its JP Morgan index benchmarks