Global fund giant Loomis, Sayles & Co has been doubling down on its investment into Elon Musk’s electric vehicle (EV) manufacturer Tesla.

According to the firm’s latest 13F filing, the various investment teams at Loomis Sayles increased their stakes in Tesla by over 41% during the last quarter as it lags the other members of the ‘Magnificent Seven’.

Following a blistering 120% rally in 2023, Tesla shares have since declined 30% year-to-date and remain some 50% below their peak in 2021.

Despite growing investor concern about the outlook for the company, Hollie Briggs, head of global product for the growth equity strategies (GES) team at Loomis Sayles, said: “There’s nothing wrong with Tesla. Tesla is not broken.”

“Our thesis comes down to the fact that we believe Tesla, given its competitive advantages, is well positioned to benefit from the secular growth in EVs,” she told FSA in an interview.

“We think that EV penetration is going to grow substantially: over our investment horizon we think EVs will go to roughly 50% of light vehicle sales.”

“We added to our position because we believe the company’s shares sell at a significant discount to our estimate of intrinsic value and thereby offer a compelling reward-to-risk opportunity.”

EV sales as a percentage of total car sales have jumped over tenfold between 2017 and 2022 and reached 18% of all cars sold in 2023, according to the International Energy Agency (IEA).

Although Tesla faces increased competition for EV sales globally, particularly from Chinese manufacturers, Briggs (pictured) said the GES team expects Tesla will be able to maintain its 20% market share as EVs continue to penetrate the auto market.

She added: “Even during the recent automotive industry slowdown, Tesla continued to show market share gains as a percentage of total light duty vehicles.”

Despite recent declines in Tesla’s operating margins following price cuts and the broader headwinds for automobile sales, Briggs noted that Tesla’s operating margins remain among the highest in the industry.

Over the long term, the GES team believes Tesla will be able to generate operating margins in the 20% range due, in part, to the software sales that are expected in the years ahead, most notably in the form of full self-driving (FSD).

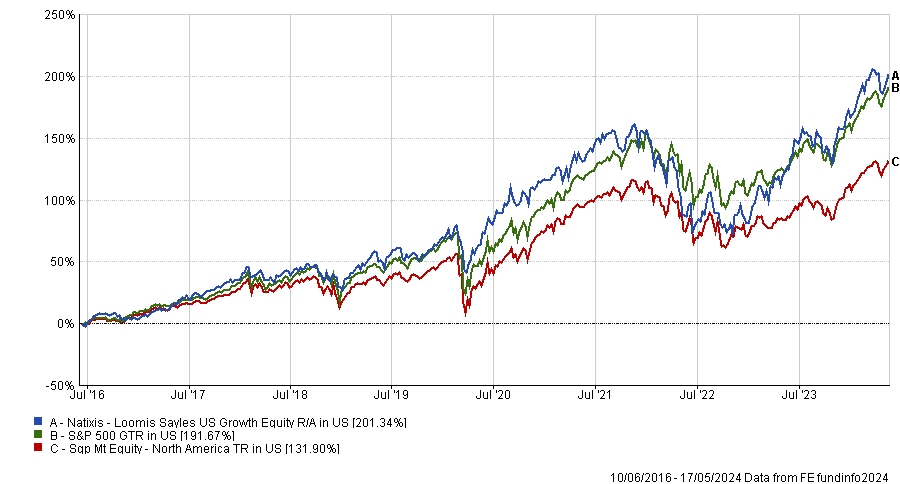

Loomis, Sayles & Co – an affiliate of Natixis Investment Managers – has $348bn in assets under management and its growth equity strategies have been long-time top performers.

The $3.6bn Natixis Loomis Sayles US Growth Equity strategy for example, was one of 10 funds last year that outperformed the S&P 500 by over 20%. It is ranked top-quartile amongst its peers over the past 1, 3 and 5 years.

Managed by Aziz Hamzaogullari since 2016, the fund significantly outperformed in 2023 and despite being a growth strategy, had a relatively lower drawdown than its other high-growth peers during 2022.

Briggs said much of this outperformance can be attributed to its contrarian investment approach and adding to out-of-favour growth stocks during downturns – so long as the fundamentals hold up.

“We’re not necessarily contrarian on whether something is a quality company,” she said. “We’re contrarian on whether or not today’s stock price represents our long-term view as we have our research done well in advance.”

“We don’t chase prices, we only buy companies as they’re coming down,” Briggs explained. “So we took advantage to buy Tesla in 2022, starting with a small position and have been adding to it to build our position on price weakness.”

She emphasised the importance of having a long-term view and modelling a company’s cash flows well beyond a typical investment horizon.

“When you look at a company like Tesla, our minimum investment time horizon might be five years, but our models are at least 10 years,” she said. “For a pharmaceutical company like Novo Nordisk our models will go out for 15 or 20 years in order to capture potential assets in their development pipeline.”

“Wegovy is all the rage right now, but if you read our investment thesis from 2014 when we first bought Novo Nordisk, we spoke about the weight loss capabilities of the GLP-1 and we even estimated a market share opportunity, which today we see is even larger given the increasing prevalence of obesity worldwide.”

Novo Nordisk has seen notable success of its GLP-1 therapies where it captures about 50% of the $20bn of spending on branded diabetes treatments, and more recently with weight loss drug Wegovy, where Novo Nordisk has been a pioneer.

“Time in the market, not timing the market matters,” Briggs added, admitting that it may sound cliché. “Compounding is so important, but one thing that some investors miss is: you get those at the end.”

“You don’t get the compounding benefits unless you actually stay invested. The companies that we’re investing in are compounding on their own opportunity so it’s sort of a compounding squared.”

“Staying invested is giving you that compounding opportunity in companies that themselves are compounding their own benefits over time.”