Global investors have been rattled by a risk-off trade over the past month as the effects of escalating tariff policy announcements and increasing political uncertainty take hold.

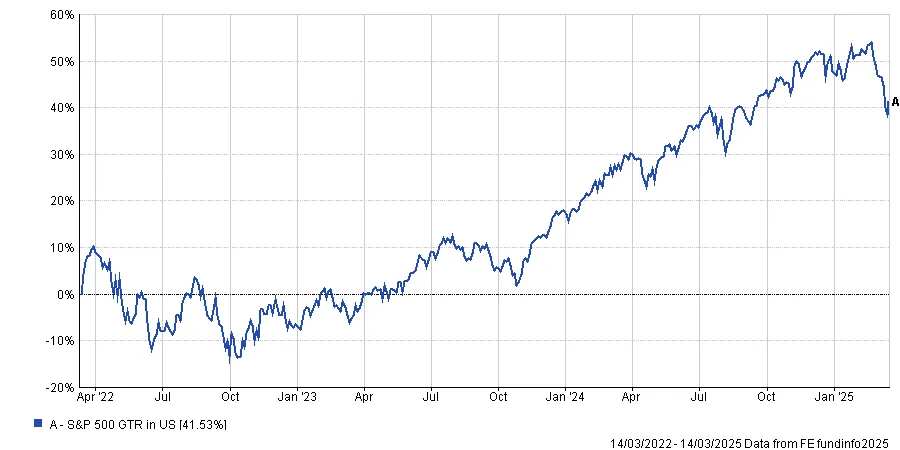

The S&P 500 index has endured a 10% correction, credit spreads have ticked up higher and US Treasuries have rallied on the back of growing fears of an economic slowdown.

Despite these recent moves, John Woods, Lombard Odier chief investment officer, Asia, said at a recent media briefing he does not see any imminent recession.

“As vanilla as that sounds, actually it’s quite a hot topic,” he added. “The market is really focusing on the impact of these tariffs on the outlook for growth.”

“Now, if, like us, you have a view that the underlying dynamics around consumption, the labour market, investment, particularly in the US, remain robust, then we observe this volatility in the market as essentially a soft patch, as a mid-cycle slowdown.”

Woods noted that a bull market typically tends to have 10% to 15% pullbacks every two and a quarter years, which is close to the duration of the current bull market. The S&P 500 index bottomed in October of 2022.

“We’ve probably got another quarter of volatility, but into the second half of this year I think growth will start to stabilise, the Fed will start to roll out cuts, the industrial cycle will normalise, profit growth will normalise and markets will stabilise and tick higher,” Woods said.

He anticipates that the S&P 500 index will close the year out higher than current levels despite continued volatility.

Woods is also bullish on the Europe, labelling it as “the most extraordinary story almost in a generation”. European stocks have rallied some 10% year-to-date.

“Germany’s decision to take its foot off the debt brake has profound consequences, extraordinary consequences, because it won’t only be Germany – that will propagate around the rest of Europe,” he said.

“We will see tens of billions, if not hundreds of billions, being spent on military upgrades, infrastructure upgrades, technology upgrades over decades.”

Woods also sees the recent volatility as a good opportunity for investors to lock in yields.

“You are getting an extraordinary amount of value in dollar credit,” he said. “Credit spreads are likely to tick a little wider on the back of this uncertainty around growth, but I don’t think it lasts long.”

“As the growth cycle normalises and as the Fed starts to cut, I think we’ll see yields tick lower both in Europe and the United States.”

However, he views investment grade credit as better risk-adjusted value than in high yield.

“If you are able to buy IG credit with a yield of 6% offers outstanding risk-adjusted value, value you’ve not seen for fifteen years.”

He added that investors could see capital appreciation as yields decline and spreads remain stable. “This is a standout opportunity we’re discussing with clients,” he said.