Andrew Norelli, JP Morgan Asset Management

Traditional fixed income such as developed market government bonds have come under pressure amid elevated inflation, while some quality higher yielding corporate credit and emerging market debt present compelling opportunities, according to JP Morgan Asset Management (JPMAM)

“We remain generally positive on economic growth, so the market’s sharp repricing has given us an opportunity to add risk at cheaper levels and higher yields while remaining short duration,” Andrew Norelli, comanager of the JPMorgan Income Fund, told FSA.

Yet, “most investors face the prospect of another year of negative real cash returns in 2022, or possibly longer. This means staying invested and seeking out assets that are likely to generate higher-yielding income have become more important.”

Norelli’s strategy has two main features: First, it aims to earn attractive income given a “prudent level of risk and, it looks for an income profile similar to high-yield credit but with lower volatility.

“This is achieved by sourcing income from sectors with low or negative correlations, hence resulting in portfolio volatility that is lower than those of the individual sectors,” said Norelli.

Second, it tries to deliver consistent dividends from a wide range of sectors, which it in part achieves by retaining coupon income for leaner times.

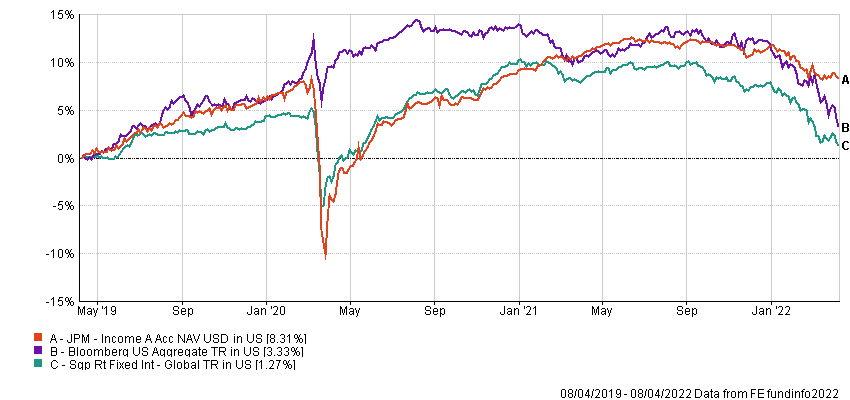

Strategy performance

The $11.3bn JP Morgan Income Fund has generated an 8.31% three-year cumulative return, outperforming its benchmark Bloomberg Barclays US Aggregate index (3.33%) and the average return of global fixed income funds available to retail investors in Singapore (1.27%), according to FE Fundinfo.

However, the strategy has been more volatile than both during the same period, and suffered a particularly sharp fall in March 2020. Its annualised volatility is 7.24%, compared with 4.81% for its benchmark and 5.55% for its peers, FE Fundinfo data shows.

JPMorgan Income Fund versus benchmark and sector average

Almost 90% of the portfolio is invest in North American bonds, and sector preferences include securitised debt (42%) and high yield credit (31%), according to the fund’s factsheet (28 February 2022).

The manager favours sectors with “well-supported fundamentals” and attractive carry, including high-yield corporate bonds, securitised credit and bank capital.

“The high yield credit market continues to look attractive on a go-forward basis as growth remains robust and corporate earnings continue to show strength. Additionally, the level of distressed debt and high yield default have remained historically low,” said Norelli.

Meanwhile, non-agency mortgage-backed securities (MBS) are supported by the strength of both the US housing market and the US consumer, and he is positive about the dynamics surrounding multi-family commercial MBS, where long-term demographic trends are beneficial, and shorter lease terms allow properties to increase rents and cash flows in line with higher growth and inflation.

Norelli also sees opportunities in emerging markets, as a result of wider spreads and higher absolute yields, and he also likes Tier-1 capital instruments because of strong bank balance sheets.

Inflation risks

Norelli expects the US Federal Reserve to hike interest rates by at least 25 basis points at each of the next seven meetings, bringing the policy rate to 1.75 – 2% by the year-end.

“Near term, a commodity shock is occurring at a time when labour markets and manufacturing capacity are already tight, global commodity inventories are low and inflation is rising at a rate not seen since the early 1980s,” he said.

“A further, material acceleration in inflation that does not subside over the balance of the year could cause central banks to be more aggressive in tightening monetary policy, thus sacrificing economic growth in future years and potentially upsetting markets.”

His concern is that if the Federal Reserve gets to 1.75%–2% over the next seven meetings and inflation is still a problem, it may start the next leg of tightening to 3%–4%. “Markets are not prepared for that,” he said.

By using US Treasury futures to manage its duration exposure, the Norelli thinks that the strategy is able to execute its interest rate decisions independently from its sector allocation strategies, “highlighting the importance of a flexible and dynamic approach to duration management”.