After a bruising 2022, there has been no shortage of asset managers who are willing to declare that fixed income is now back.

Last year, bonds sold off on par or in some cases more than equities, while the historically negative stock-bond correlation broke down.

Despite this difficult backdrop, advocates of fixed income point to the fact that last year’s repricing means that most fixed income assets now yield much more than dividend yield of the S&P 500 index.

At the same time, the negative correlation between stocks and bonds has re-emerged and the diversification benefits of fixed income are clear once again.

For the time being though, most of the interest in fixed income is towards core fixed income, particularly government bonds, as the feeling is that corporate spreads do not look sufficiently attractive to compensate investors for the recession risk.

Most asset managers are taking a wait-and-see approach when it comes to corporate debt, hoping that as more companies begin to refinance at higher rates, there will be opportunities to pick up good quality assets at attractive prices.

Meanwhile, duration remains a thorny issue as there are some advocates that now is a good time to lock in long duration assets with rates expected to fall, although that is by no means consensus at the moment.

Against this background, Darius McDermott, managing director at Chelsea Financial Services, chose the M&G Global Macro Bond fund and the Wellington Global Bond fund for this week’s head-to-head article.

| M&G | Wellington | |

| Size | $1.68bn | $1.64bn |

| Inception | 2011 | 2018 |

| Managers | Jim Leaviss | n/a |

| Three-year cumulative return | -5.74% | -5.69% |

| Three-year annualised return | -6.24% | -5.73% |

| Three-year annualised alpha | -1.23 | 1.05 |

| Three-year annualised volatility | 8.04 | 10.64 |

| Three-year information ratio | -0.54 | -0.28 |

| FE Crown fund rating | *** | ** |

| OCF (retail share class) | 0.63% | 0.55% |

Investment approach

The M&G fund has the discretion to buy bonds issued by governments and companies anywhere throughout the world as well as those denominated in any currency.

In deciding which bonds to buy, manager Jim Leaviss considers the macroeconomic environment and then will rely on the stock-picking skill of his team to build out the portfolio.

That flexibility in terms of markets the fund can invest in allows Leaviss to choose which bond markets he likes throughout the world and then overlay tactical bets onto them.

Leaviss also leverages the ideas of different fund managers within the wider M&G group, choosing the ideas that most align with his long-term macro views and short-term overlays.

“The goal is to find a range of bonds that are not correlated with each other. This is where risk management is centred. Risk is a key input into the whole framework, with correlation the main statistic to consider,” said McDermott.

The fund typically holds 0.5% in any single corporate bond name with the aim of reducing the impact of individual stock failures. In total, the fund will have about 100 to 120 different positions at any given time.

“The goal is to find a range of bonds that are not correlated with each other. This is where risk management is centred. Risk is a key input into the whole framework, with correlation the main statistic to consider,”

darius mcdermott, chelsea financial services

Meanwhile, the Wellington fund invests across government bonds, currencies and global credit with the majority of opportunities they invest in comprising liquid rates and liquid currencies. Credit is added to the approach but is not the main driver, notes McDermott.

The fund gets investment ideas following detailed macroeconomic analysis and specialist research into major government bond markets. The fund also utilises a quantitative model to pick out relative value opportunities in government bonds.

McDermott also touches upon some differences between the two funds with the Wellington fund having a greater exposure to higher quality bonds, while the M&G fund has greater exposure to duration and yields more.

Fund characteristics

Country allocation:

| M&G | Wellington | ||

| US | 35.5% | n/a | n/a |

| UK | 14.6% | n/a | n/a |

| Germany | 7.1% | n/a | n/a |

| France | 3.3% | n/a | n/a |

| Mexico | 3.1% | n/a | n/a |

| Spain | 2.9% | n/a | n/a |

| Canada | 2.9% | n/a | n/a |

| Italy | 2.7% | n/a | n/a |

| Other | 27% | n/a | n/a |

| Cash | 18.8% | n/a | n/a |

Performance

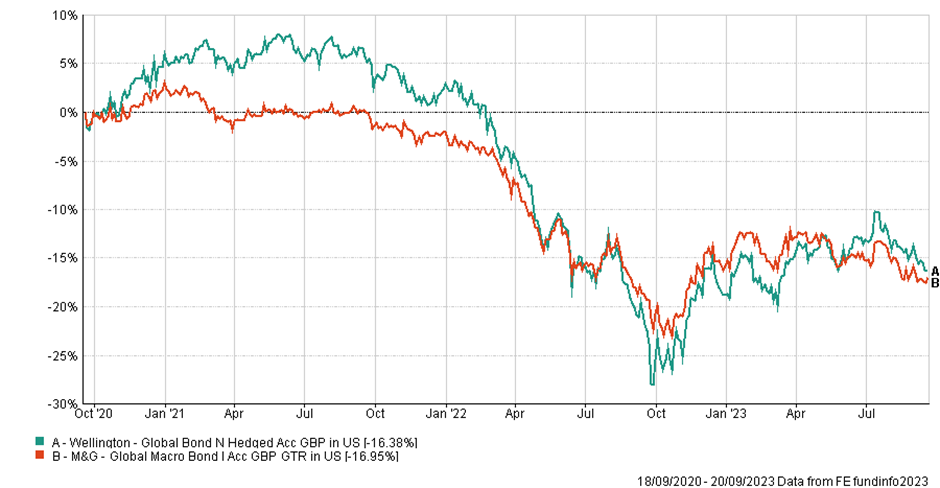

“Both have ‘go anywhere’ mandates, although the M&G fund does appear to dive deeper into emerging markets. I’d expect the M&G fund to outperform when markets rally, but the 80% exposure to A-rated or above government bonds should give the Wellington fund greater downside security. It is interesting that the Wellington fund is up 6% year-to-date, while the M&G has lost 0.2%,” said McDermott.

McDermott also points out that it is difficult to pinpoint an exact time when the M&G fund will traditionally perform given its top-down focus, although he expects the Wellington fund to fare better in more volatile periods given its greater exposure to higher quality bonds and emphasis on liquidity.

McDermott also notes that the fees for both funds are reasonable with the Wellington fund having an ongoing charge of 0.55%, while for M&G this is slightly higher at 0.63%.

Discrete calendar year performance

| Fund | YTD* | 2022 | 2021 | 2020 | 2019 |

| M&G | -4.33% | -3.23% | -3.98% | 8.83% | 4.39% |

| Wellington | -0.09% | -11.20% | -2.02% | 4.12% | 2.33% |

Manager review

“The two teams behind these funds are about as good as they can get,” said McDermott.

Leaviss has been with M&G since 1997 following a five-year period at the Bank of England. He has managed the M&G Global Macro Bond fund ever since its launch in 1999 and also heads up the firm’s wholesale fixed interest team, which has £46bn ($56.5bn) of assets under management.

Meanwhile, the Wellington fund is managed by the global bond investment team, which comprises a mixture of strategists, investment analysts and risk managers. Each portfolio manager is given the mandate to come up with investment ideas for his or her particular area of knowledge.

Conclusion

Overall, McDermott says that both funds are good options and that the Wellington fund is a core holding, which is focused on providing security and liquidity to investors. He notes that over the past decade, the only time it has recorded a meaningful loss was in 2022.

“If I were to lean towards one, it would be the M&G fund, purely because we know just how good a manager Jim Leaviss is. He has a vast array of tools at his disposal for this fund and uses them all to great effect. From his own ability to read the macroeconomic environment, to his team’s stock-picking skills and full flexibility of the fund in terms of bonds, currencies and the use of derivatives, it is a formidable mix,” said McDermott.