The FSA Spy market buzz – 6 June 2025

Animal spirits run wild; Franklin Templeton is taking credit; EM banking revolution; Not all luxury is equal; Death of search and the AI machine; George Soros on wins and much more.

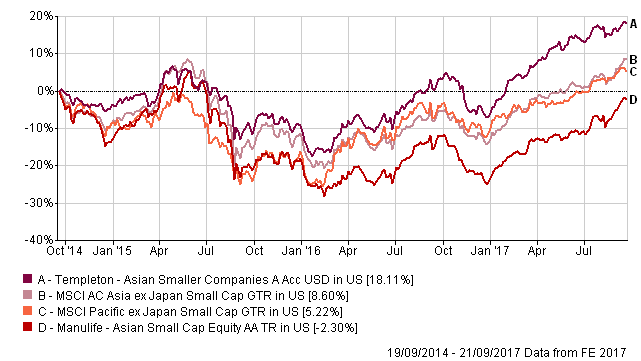

The Manulife fund severely underperformed in 2016, delivering a 5.59% loss, compared to a loss of 1.15% for its benchmark.

“It was expected, given that last year was a value rally,” said Share. “It was mainly the energy stocks and the material stocks that were outperforming, whereas this fund has more of a growth focus, so more focused on IT or consumer names.”

Some growth stocks also did well, but they were mostly in the large cap space, such as Alibaba, Tencent or Baidu. “Since this is a small cap fund, it was unable to participate in that large cap tech rally,” Share said.

The Manulife fund delivered a better performance than the Templeton fund in four out of nine calendar years since the latter fund’s inception: 2011, 2012, 2013, and so far in 2017.

The Templeton fund performed better in 2016 likely thanks to the value bias in some of the stocks the management team likes, Share said. “They try to buy stocks that are trading at a discount to their growth potential. In a value environment like last year, they’ve also done well.”

The Manulife fund shows a higher volatility, predominantly due to the high portfolio turnover, Share noted. “There’s a lot of market timing in there,” she said.

| Manulife | Templeton | |

| 3-year return (cumulative) | -5.95% | 18.16% |

| 1-year return | 10.12% | 16.95% |

| 3-year Alpha | -5.17 | 2.71 |

| 3-year Beta | 1.03 | 0.85 |

| 3-year Sharpe Ratio | -0.01 | 0.32 |

| 3-year Volatility | 15.71 | 13.07 |

| Annual turnover | 200% – 300% | 20% |

Investors turn to real estate for alternative income

Investors turn to real estate for alternative income

Tap into Japan’s post-pandemic growth trends

Tap into Japan’s post-pandemic growth trends

Ninety One: Finding opportunities in times of change

Ninety One: Finding opportunities in times of change

Healthcare’s innovation shifts into high gear

Healthcare’s innovation shifts into high gear

Exciting opportunities in AI & Robotics outside of traditional tech

Exciting opportunities in AI & Robotics outside of traditional tech

Despite headwinds, ESG continues to perform

Despite headwinds, ESG continues to perform

Don’t get left behind in fixed income

Don’t get left behind in fixed income

M&G Episode Macro shines after tough year

M&G Episode Macro shines after tough year

Your Questions Answered by Federated Hermes Impact Opportunities

Your Questions Answered by Federated Hermes Impact Opportunities

How can a sustainable approach also ensure you don’t compromise performance?

How can a sustainable approach also ensure you don’t compromise performance?

Animal spirits run wild; Franklin Templeton is taking credit; EM banking revolution; Not all luxury is equal; Death of search and the AI machine; George Soros on wins and much more.

Part of the Mark Allen Group.