Macroeconomic uncertainty coupled with rising inflation levels and the possibility of a looming recession have caused the performance of Asian equities to be topsy-turvy.

Most recently, on Tuesday, Asian stocks mostly rose as investors cheered the prospect that the US economy will avert a major debt default, improving sentiment across most asset classes.

MSCI’s broadest index of Asia Pacific shares outside Japan rose 0.4% early Tuesday after US stocks closed on Monday for the Memorial Day holiday. The index was down some 1.3% in the month of May.

Over in Hong Kong, the Hang Seng index climbed 0.31% while neighbouring China’s CSI300 index dipped 0.06%. Meanwhile, Australian shares were up 0.03%, while the Nikkei stock index slipped 0.28%, cooling a tad after the Japanese benchmark hit a 33-year high on optimism over the US debt deal and a weaker yen.

Against this background, FSA asked Claire Liang, senior analyst for manager research at Morningstar, to select two Asian equities funds for comparison. She chose the JP Morgan Pacific Equity fund and Robeco Asia Pacific fund.

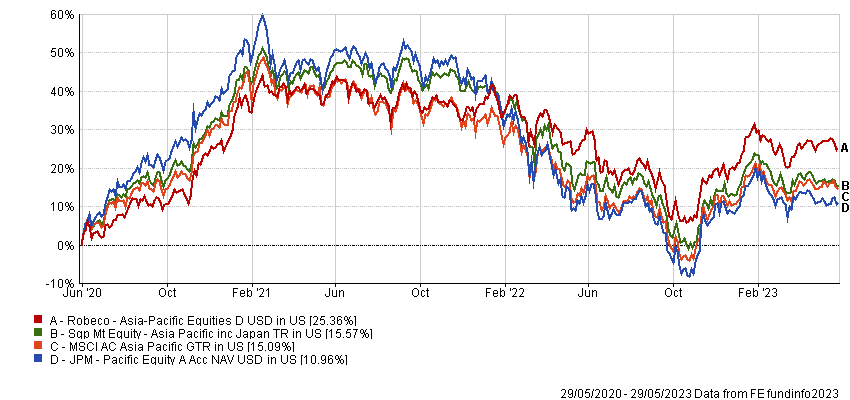

Managed by Aisa Ogoshi and Robert Lloyd, the JP Morgan fund has seen an annualised three-year cumulative return of 4.22% compared to the Robeco fund, which has a return of 8.69%. The latter, which was set up in 2010, is managed by Harfun Ven and Joshua Crabb.

| JPM Pacific Equity | Robeco Asia Pacific Equity | |

| Size | $1.87bn | $481.5mn |

| Inception | 2005 | 2010 |

| Managers | Aisa Ogoshi, Robert Lloyd | Harfun Ven, Joshua Crabb |

| Three-year cumulative return | 4.22% | 8.69% |

| Three-year annualised return | 3.53% | 7.82% |

| Three-year annualised alpha | -1.85 | 3.24 |

| Three-year annualised volatility | 17.67% | 15.4% |

| Three-year information ratio | -0.27 | 0.39 |

| Morningstar star rating | ***** | **** |

| Morningstar medallist rating | Silver | Bronze |

| FE Crown fund rating | ** | ** |

| OCF (retail share class) | 1.78% | 1.76% |

Investment approach

Both funds adopt different investment styles, observes Liang. Breaking this down further, she explains that the investment process for the JP Morgan Pacific fund is actually “quite growth focused”. “The portfolio managers will look for companies that have strong balance sheets, good management teams as well as solid growth prospects. As such, we can see that the portfolio has been formally sitting in the core growth area of the Morningstar style box over the years,” she said.

In line with this, the portfolio for the JP Morgan fund is also overweight industry leaders, such as AIA and Tencent, meaning that the overall portfolio actually has greater exposure towards the giant and large cap names. “I think the portfolio has been leaning towards growth-oriented sectors as it has a notable overweight position and also has a higher position in the technology and healthcare sectors over the past three years compared to the Robeco fund,” said Liang. Conversely, she pointed out that the JP Morgan fund has a “light touch” in traditional sectors such as energy, utilities and real estate, unlike the Robeco fund.

“I think the portfolio has been leaning towards growth-oriented sectors as it has a notable overweight position and also has a higher position in the technology and healthcare sectors over the past three years compared to the Robeco fund.”

Claire Liang, senior analyst, manager research at Morningstar

Regarding the Robeco fund, Liang noted that the managers make decisions based on “momentum awareness”. “So, the portfolio manager actually looks for low valuations relative to their peers, but they also recognise the momentum factors can be a major market driver in Asia. So, they will pay attention to the company’s earnings and price momentum terms in sizing their stock positions and identify better entry and exit positions,” she said.

“We have seen that the portfolio has been sitting in the value area of the Morningstar style box over time and its P/E [price-to-earnings] and P/B [price-to-book] multiples have been below the index as well,” said Liang. In terms of sector allocation, Robeco’s portfolio has a higher allocation to financials, industrials, real estate and energy compared to the JP Morgan fund and it also has less exposure to information technology and healthcare.

Fund characteristics

Sector allocation:

| JP Morgan | Robeco | ||

| Information Technology | 25.6% | Industrials | 20.9% |

| Financials | 18.3% | Financials | 20.6% |

| Health Care | 11.7% | Information Technology | 17.3% |

| Consumer Discretionary | 10.6% | Consumer Discretionary | 12.6% |

| Industrials | 10.2% | Communication Services | 6.4% |

| Communication Services | 8.0% | Real Estate | 6.0% |

| Consumer Staples | 6.6% | Health Care | 5.6% |

| Materials | 6.4% | Materials | 4.0% |

| Real Estate | 1.8% | Consumer Staples | 3.6% |

| Cash | 0.8% | Energy | 2.3% |

| Utilities | 0.6% |

Top five holdings:

| JP Morgan | weighting | Robeco | weighting |

| Taiwan Semiconductor | 7.0% | Alibaba Group | 4.08% |

| Tencent | 5.0% | Samsung Electronics | 4.05% |

| Samsung Electronics | 4.7% | Sumitomo Mitsui Financial Group | 3.80% |

| CSL | 3.8% | Hitachi | 2.96% |

| Sony | 3.4% | T&D Holdings | 2.53% |

Geographical allocation:

| JP Morgan | weighting | Robeco | weighting |

| Japan | 33.3% | Japan | 40.9% |

| China | 16.3% | China | 17.2% |

| Taiwan | 12.2% | Australia | 9.4% |

| Korea | 10.7% | Korea | 9.4% |

| Australia | 9.6% | Taiwan | 4.9% |

Performance

Comparing the two funds, Liang pointed out that Robeco’s portfolio is a bit more diversified compared to the JP Morgan fund and it has a greater allocation to mid-cap stocks as well.

As for the performance of the two funds, she pointed out that the JP Morgan fund is expected to do well in a growth environment, as was the case between 2017 and 2019 and in 2020. However, it may struggle during value environments such as in 2021 and 2022, where value stocks notably outperformed their growth peers. Interestingly, the performance of the Robeco fund has been quite the opposite given the different emphasis of its manager.

Nonetheless, both strategies have demonstrated a higher volatility in terms of the standard deviation relative to the index in the long run. Additionally, the JPMorgan fund has a more concentrated portfolio than the Robeco fund.

Discrete calendar year performance

| Fund/Sector | YTD* | 2022 | 2021 | 2020 | 2019 | 2018 |

| JP Morgan | 1.98% | -23.6% | -1.1% | 31.29% | 27.99% | -12.8% |

| Robeco | 5.19% | -12.45% | 6.56% | 8.26% | 16.91% | -18.54% |

| Asia Pacific ex Japan | 3.68% | -17.22% | -1.46% | 19.71% | 19.36% | -13.52% |

Manager review

There has obviously been a rotation from growth to value since stocks since 2021 and if that were to continue, Liang says that the Robeco fund would continue to outperform the JP Morgan strategy. She added that the JP Morgan was more volatile.

However, she has a higher conviction on the JP Morgan investment team. The fund is led by Robert Lloyd and Aisa Ogoshi, the latter of whom has 24 years of investment experience. Ogoshi spent the first four years of her career as an analyst and a portfolio manager in in JP Morgan’s Japan portfolio management team.

Laing pointed out that her Japan investment credentials are important considering that Japan accounts for over 30% of the index. “She gets support from the sector analyst and also the country’s specialist within JP Morgan’s nearly 100-member, emerging markets and Asia Pacific equities team,” she said, adding that this is the largest team that Morningstar covers in the region.

Robeco’s fund is co-managed by Joshua Crabb, who has 27 years of experience, although he only took over the fund in July 2022. He is very experienced, particularly in Asia Pacific ex-Japan equities.

With this in mind, Liang reckons that the other co-manager, Harfun Ven, can help plug the gap, given his strong investment background in Japan. All in all, the fund gets good support from a compact team of 13 and while the team is quite experienced, it has seen some turnover at the senior ranks in the recent years.

Conclusion

When asked which fund she prefers, Liang pointed out that both are good options for investors seeking exposure to Asia Pacific equities. “We have a higher conviction and higher rating on the JP Morgan fund because it has a strong management team who are backed by deep and analytical resources,” she said. She also said that the JP Morgan fund’s investment process is well structured and has been consistently applied, thus allowing it to deliver strong results over market cycles.

Amid expectations of rising inflation levels and higher interest rates, Liang believes that growth stocks may suffer. This may hurt the JP Morgan Pacific fund given the portfolio manager’s preference for quality growth stocks.