The FSA Spy market buzz – 6 June 2025

Animal spirits run wild; Franklin Templeton is taking credit; EM banking revolution; Not all luxury is equal; Death of search and the AI machine; George Soros on wins and much more.

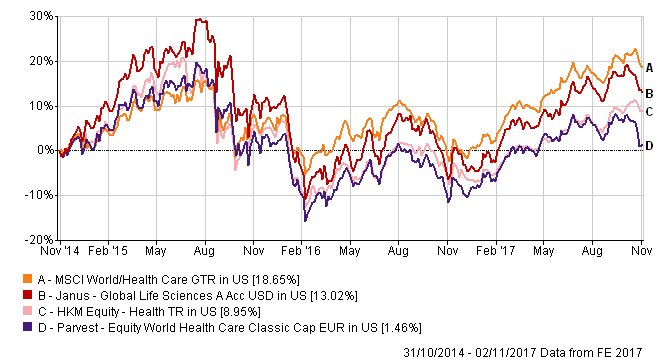

Both funds use the MSCI World Health Care Index as their benchmarks, with the Parvest fund using the Ucits III-compliant 10/40 version of the index, which imposes concentration limits (performance of both indices was identical over the three-year period ending 31 October).

One of the main factors in the performance of the two funds is exposure to the sub-industries in healthcare, Ng said.

The Janus fund outperformed the benchmark and the Parvest fund by a healthy margin in 2012-14, thanks to its bias toward biotech. “In 2012-14, the biotech sector performed very well.

“After 2015, you don’t see a very big difference between the performance of biotechnology and pharmaceuticals and in 2016, both biotech and pharmaceuticals underperformed,” he said.

As a result, in 2015 and 2016 both funds underperformed.

So far in 2017, both products have delivered double-digit returns, with the Janus fund doing slightly better than the index and Parvest underperforming it.

Both funds have a negative alpha, high beta, and volatility exceeding that of the index, as measured on a three-year basis. While the measurements for the five-year period, which includes the biotech boom of 2012-14, put the Janus fund in a better light with alpha of 0.40 (Parvest’s remains negative at -4.98), the numbers underscore the difficulties in outperforming the index in a risky and volatile industry.

Biotech carries high risk. “Biotech companies require a lot of resources for research and development, a sustainable investment before they pay the money back” said Ng. This results in higher risk and volatility.

| Janus | Parvest | MSCI World Health Care Index | |

| 3-year return (cumulative) | 13.52% | 1.20% | 18.87% |

| 1-year return | 20.13% | 12.46% | 19.80% |

| 3-year Alpha | -2.47 | -5.76 | |

| 3-year Beta | 1.25 | 1.14 | |

| 3-year Sharpe Ratio | 0.05 | 0.00 | |

| 3-year Volatility | 16.44 | 14.64 | 12.06 |

Data: FE, 31 October 2017, returns in US dollars, ratios are annualised

China’s post-pandemic growth gathers pace

China’s post-pandemic growth gathers pace

Accessing India’s tech future

Accessing India’s tech future

How ETFs offer an active way to drive sustainable returns

How ETFs offer an active way to drive sustainable returns

Market volatility is creating enticing opportunities for value investors

Market volatility is creating enticing opportunities for value investors

Investment Ideas for 2021: Explore the untapped potential in China Small Companies

Investment Ideas for 2021: Explore the untapped potential in China Small Companies

Don’t get left behind in fixed income

Don’t get left behind in fixed income

Sourcing resilient yield and income through short-dated credit

Sourcing resilient yield and income through short-dated credit

China bonds: plugging the yield gap

China bonds: plugging the yield gap

Sustainable Investing in Changing Market Conditions

Sustainable Investing in Changing Market Conditions

Animal spirits run wild; Franklin Templeton is taking credit; EM banking revolution; Not all luxury is equal; Death of search and the AI machine; George Soros on wins and much more.

Part of the Mark Allen Group.