The FSA Spy market buzz – 6 June 2025

Animal spirits run wild; Franklin Templeton is taking credit; EM banking revolution; Not all luxury is equal; Death of search and the AI machine; George Soros on wins and much more.

The Franklin strategy has shown disparate results during the past decade, according to Caquineau. The light exposure to defensive sectors has been a headwind, while stock-picking has been less effective in recent years, particularly in 2014 with the underperformance of long-term plays such as Metro and Cairn.

In 2015, the fund’s upside was limited by the underweighting of healthcare, a few unsuccessful stock bets and a large cash position, Caquineau explained. In 2016, the team made a mistake during the Brexit vote by cutting its exposure to banks at steep losses. Stock-picking in financial services was also negative in 2017 but proved more successful in 2018. Stock picking was positive across sectors ex-financials and industrials in 2019.

Under Katrina Dudley’s tenure as lead manager from May 2018 the stock-picking has been more consistent, which is a positive sign, noted Caquineau.

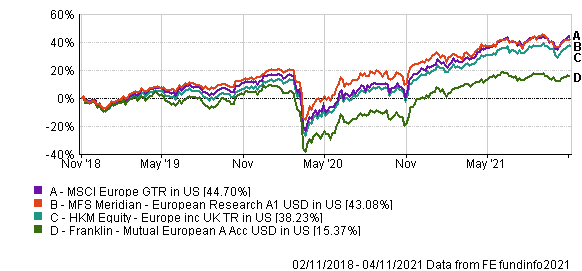

Over three years, the fund has generated a cumulative return of 15.37% in US dollar terms, according to FE Fundinfo, which is a significant underperformance relative to its MSCI Europe Index benchmark (44.07%) and the average return of European equity funds available to Hong Kong retail investors (38.23%).

The product has also been more volatile during the same period, with annualised volatility of 26.06%, compared with 22.43% for its benchmark and 21.4% for its peers.

“The Franklin fund will do better when value as a style outperforms,” said Caquineau.

Turning to the MFS fund, Caquineau noted that it has delivered solid risk-adjusted returns over the long term.

“Strong returns have typically been generated across a broad range of stocks and sectors, reflecting the quality of research across the board,” he said. “The consistency of these returns through different market environments is impressive.

Historically, the team’s focus on high-quality franchises and sustainable earnings growth has helped the fund exhibit greater resilience in weaker market conditions such as 2008, 2011, or the first quarter of 2020, according to Caquineau.

The fund has posted a 43.08% three-year cumulative return in US dollars, just shy of its MSCI Europe benchmark and ahead of its peers, according to FE Fundinfo. Its annualised volatility of 20.03% is less than the volatilities of both its index and sector average.

“The MFS fund’s portfolio is built to be less sensitive than the Franklin product to style cycles,” said Caquineau.

“MFS has indeed generated consistent returns through different market environments whereas Franklin has experienced headwinds as growth stocks outperformed value stocks in recent years,” he concluded.

Discrete calendar year performance

| Fund/Sector |

YTD* |

2020 |

2019 |

2018 |

2017 |

2016 |

| Franklin |

11.32% |

-4.61% |

17.88% |

-17.12% |

19.84% |

-3.81% |

| MFS |

10.07% |

8.40% |

27.04% |

-14.04% |

28.48% |

-5.15% |

| Equity – Europe incl. UK |

15.31% |

6.44% |

22.20% |

-16.71% |

24.03% |

-4.61% |

| MSCI Europe |

17.24% |

5.93% |

24.59% |

-14.32% |

26.24% |

0.22% |

Healthcare’s innovation shifts into high gear

Healthcare’s innovation shifts into high gear

Thematic investment series: Innovative transformation cuts across “old” and “new” economy companies

Thematic investment series: Innovative transformation cuts across “old” and “new” economy companies

Accessing Asian 5G innovation: three key portfolio themes

Accessing Asian 5G innovation: three key portfolio themes

Tech WELLcovered | Work reimagined

Tech WELLcovered | Work reimagined

Fixed income – making ground in ESG as ETFs see rapid growth in AUM

Fixed income – making ground in ESG as ETFs see rapid growth in AUM

Dynamism is the name of the game for this global macro strategy

Dynamism is the name of the game for this global macro strategy

Unmasking the dividend opportunity

Unmasking the dividend opportunity

Your Questions Answered by Federated Hermes Impact Opportunities

Your Questions Answered by Federated Hermes Impact Opportunities

Riding the wave of alternative income amongst HNWIs in APAC

Riding the wave of alternative income amongst HNWIs in APAC

How can a sustainable approach also ensure you don’t compromise performance?

How can a sustainable approach also ensure you don’t compromise performance?

Animal spirits run wild; Franklin Templeton is taking credit; EM banking revolution; Not all luxury is equal; Death of search and the AI machine; George Soros on wins and much more.

Part of the Mark Allen Group.