The FSA Spy market buzz – 6 June 2025

Animal spirits run wild; Franklin Templeton is taking credit; EM banking revolution; Not all luxury is equal; Death of search and the AI machine; George Soros on wins and much more.

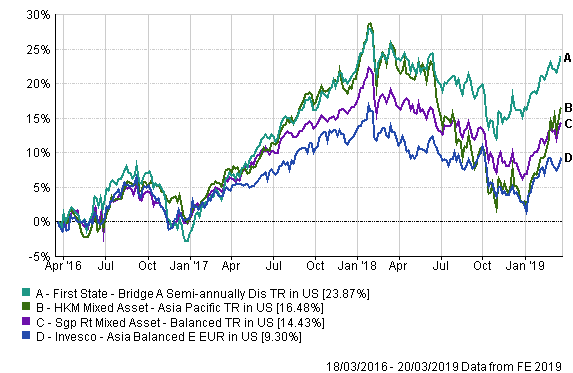

Nel believes that the First State Fund outperforms its peers during bear markets because of the equity sleeve’s focus on quality stocks. However, it may lag its peers during market rallies because of that focus.

“But it has consistently outperformed its index and its peers,” Nel noted.

Turning to the Invesco fund, Nel said that the product’s flexibility should enable it to participate more in an equity rally, and thus, should outperform.

“We do expect the product to do better [than the First State fund], especially if there is more upside in equities,” he said.

However, the fund historically has underperformed its peers as well as its benchmark, Nel noted.

“If you look at only high dividend stocks, you can fall into value traps,” he said, adding that the change in strategy in 2017 to have a total return approach should be positive for the fund.

“But it’s still too early to see whether this change will be good,” he said.

Discreet annual calendar performance (%)

| Fund / sector |

YTD 2019 |

2018 | 2017 | 2016 | 2015 |

2014 |

| First State Bridge A Semi-annually Dis TR in US |

5.98 |

-4.71 | 24.82 | 1.81 | -3.72 |

7.84 |

| Sector : Singapore retail mixed asset balanced |

6.72 |

-8.75 | 17.07 | 2.39 | -6.57 |

-0.77 |

| Invesco Asia Balanced E EUR in US |

6.16 |

-9.75 | 13.25 | 1.96 | -8.09 |

3.08 |

| Sector: Hong Kong mixed asset Asia Pacific |

12.81 |

-14.87 | 20.64 | -0.50 | -6.24 |

2.61 |

In terms of volatility, the First State fund is more volatile than the Invesco product, according to data from FE.

| Fund / Index |

Volatility |

| First State Bridge A Semi-annually Dis TR in US |

7.83 |

| Sector : Singapore retail mixed asset balanced |

6.23 |

| Invesco Asia Balanced E EUR in US |

6.69 |

| Sector: Hong Kong mixed asset Asia Pacific |

9.71 |

“But First State’s downside protection is better, as well as its risk-adjusted returns,” he said.

The First State fund’s three-year annualised Sharpe ratio, which measures risk-adjusted returns, is 0.46, while the Invesco fund’s Sharpe ratio is 0, according to FE.

From “FAANG” to “MAMAA” to “Magnificent 7” – what’s in a name?

From “FAANG” to “MAMAA” to “Magnificent 7” – what’s in a name?

Tech WELLcovered | Work reimagined

Tech WELLcovered | Work reimagined

Who’s afraid of higher interest rates?

Who’s afraid of higher interest rates?

Fixed income – making ground in ESG as ETFs see rapid growth in AUM

Fixed income – making ground in ESG as ETFs see rapid growth in AUM

Investment Ideas for 2021: Explore the untapped potential in China Small Companies

Investment Ideas for 2021: Explore the untapped potential in China Small Companies

Market volatility is creating enticing opportunities for value investors

Market volatility is creating enticing opportunities for value investors

The year of living dangerously for income investors

The year of living dangerously for income investors

China bonds: plugging the yield gap

China bonds: plugging the yield gap

Sustainable Investing in Changing Market Conditions

Sustainable Investing in Changing Market Conditions

Accessing Asian 5G innovation: three key portfolio themes

Accessing Asian 5G innovation: three key portfolio themes

Animal spirits run wild; Franklin Templeton is taking credit; EM banking revolution; Not all luxury is equal; Death of search and the AI machine; George Soros on wins and much more.

Part of the Mark Allen Group.