The FSA Spy market buzz – 6 June 2025

Animal spirits run wild; Franklin Templeton is taking credit; EM banking revolution; Not all luxury is equal; Death of search and the AI machine; George Soros on wins and much more.

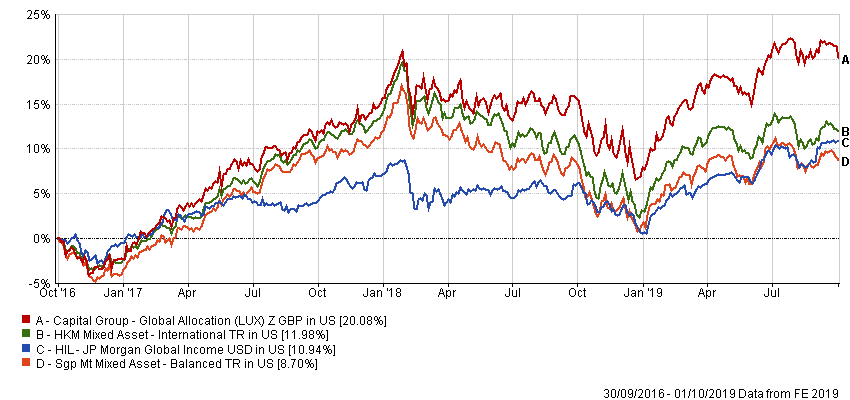

Performance

“Although both products consistently outperform their internal benchmarks, the Capital Group fund has typically generated stronger returns than the JP Morgan fund,” said Claus.

“Its growth bias means that it performs better in market upturns, and it has, perhaps surprisingly, also held up well compared with the more value-focussed JP Morgan fund during market downturns, such as in 2018,” she added.

The Capital Group fund has generated a three-year cumulative US-dollar return of 20.08% compared with 10.94% by the JP Morgan fund, although at the expense of greater annualised volatility of 7.15% compared with 4.71%, according to FE Analytics data.

Since its launch in February 2014, the Capital Group fund has outperformed both its moderate-allocation category and its 60% MSCI ACWI and 40% Bloomberg Barclays Global Aggregate benchmark.

“Risk-adjusted returns of the strategy have been appealing as well, evidenced by an above-average upside-capture ratio and a higher resilience in drawdowns,” said Claus.

“Stock selection has been by far the most important performance driver of the strategy, including in 2015 and 2017,” she added.

In 2015, the overweights in Amazon and Microsoft were the largest contributors, and in 2017, Nintendo and ASML were among the best-performing stocks. In 2016 and 2018, stock-selection results were fairly neutral, but in 2018, the large overweight in British American Tobacco “detracted from relative performance, while cash and an overweight in Merck were the largest positive contributors in a falling market environment,” said Claus.

Turning to the JP Morgan fund, “while the strategy’s long-term record remains strong, it does court significant risk because of its sizable high-yield debt component,” said Claus.

“In turbulent markets, such as 2008 and 2011, when credit fears rise, the strategy is more vulnerable to losses. Having said that, volatility has been falling is slightly below the category average (5.64%).”

Moreover, the strategy has provided a high income while delivering competitive total returns, according to Claus.

Its 13.54% five-year cumulative return is much higher than its category average of 3.60%, according to FE Analytics data.

Meanwhile, the yield at over 5% is paid out from the portfolio’s underlying holdings, so that capital growth is not being sacrificed to make income distributions.

“Overall, the fund has offered an attractive combination of income and capital appreciation,” said Claus.

Discrete annual performance

|

Fund /Sector |

2018 |

2017 |

2016 |

2015 |

2014 |

| Capital Group |

-0.78% |

7.91% |

24.27% |

4.94% |

– |

| Mixed asset – international |

-3.74% |

6.95% |

21.15% |

1.11% |

7.40% |

| JP Morgan |

-6.17% |

7.76% |

4.55% |

-1.92% |

4.95% |

| Mixed asset – balanced |

-9.98% |

15.60% |

-3.62% |

-4.70% |

-1.18% |

Healthcare’s innovation shifts into high gear

Healthcare’s innovation shifts into high gear

The year of living dangerously for income investors

The year of living dangerously for income investors

From “FAANG” to “MAMAA” to “Magnificent 7” – what’s in a name?

From “FAANG” to “MAMAA” to “Magnificent 7” – what’s in a name?

Exciting opportunities in AI & Robotics outside of traditional tech

Exciting opportunities in AI & Robotics outside of traditional tech

Step up your portfolio by doubling down on sectors set for long-term growth

Step up your portfolio by doubling down on sectors set for long-term growth

The future of mobility

The future of mobility

Accessing India’s tech future

Accessing India’s tech future

Impact opportunities: investing to limit biodiversity loss

Impact opportunities: investing to limit biodiversity loss

Tap into Japan’s post-pandemic growth trends

Tap into Japan’s post-pandemic growth trends

Market volatility is creating enticing opportunities for value investors

Market volatility is creating enticing opportunities for value investors

Animal spirits run wild; Franklin Templeton is taking credit; EM banking revolution; Not all luxury is equal; Death of search and the AI machine; George Soros on wins and much more.

Part of the Mark Allen Group.