The FSA Spy market buzz – 6 June 2025

Animal spirits run wild; Franklin Templeton is taking credit; EM banking revolution; Not all luxury is equal; Death of search and the AI machine; George Soros on wins and much more.

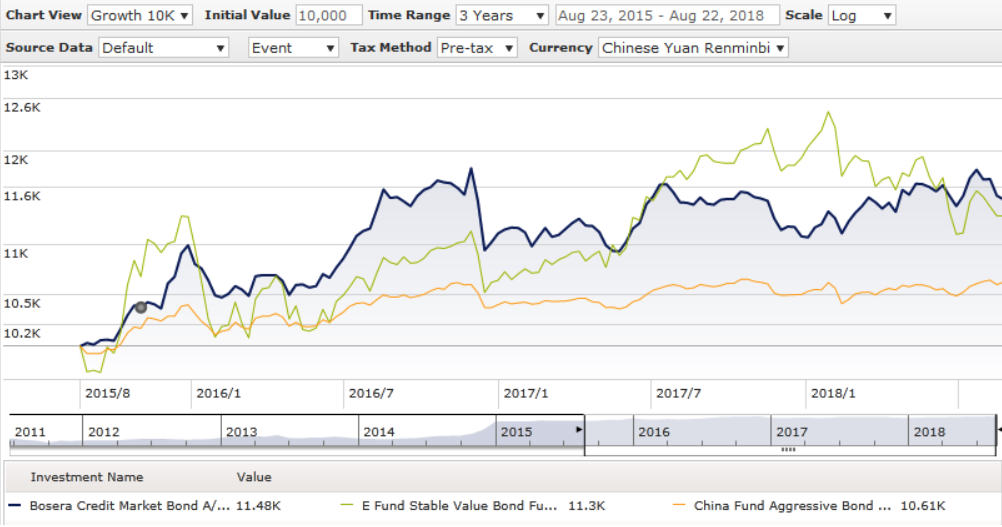

Both funds have performed differently depending on which asset classes performed well during a particular calendar year, Wu said.

Although the majority of both funds are invested in fixed income, Wu noted investors should look at the asset allocation of the equity sleeve as well because both asset classes can be performance drivers.

For example, onshore Chinese equities underperformed this year compared to last year, which led to negative returns for the E Fund product.

However, the Bosera Fund posted positive returns because of exposure to policy bank bonds, according to Wu.

Discreet calendar year performance

|

YTD |

2017 | 2016 | 2015 |

2014 |

|

| Bosera Fund |

3.8 |

-0.51 | 1.5 | 12.98 |

88.34 |

| E Fund Fund |

-4.96 |

11.75 | -5.88 | 29.32 |

77.68 |

“The policy bank bond assets contributed a lot to the Bosera fund’s performance this year,” Wu said.

However, the same asset class led to negative returns last year as policy bank bonds underperformed.

Turning to the E Fund vehicle, she said that equity exposure was a key driver, adding that the fund performed well during the growth stock rally in 2014 and 2015.

Wu added that both funds have high volatility. The three-year annualised volatility for the Bosera fund is 7.39, while E Fund’s volatility is 11.18.

Wu explained that the E Fund’s volatility is higher is due to its exposure to growth stocks, which are more volatile than other stocks in the onshore market.

China bonds: plugging the yield gap

China bonds: plugging the yield gap

Conditions in the high yield market

Conditions in the high yield market

Don’t get left behind in fixed income

Don’t get left behind in fixed income

How ETFs offer an active way to drive sustainable returns

How ETFs offer an active way to drive sustainable returns

From “FAANG” to “MAMAA” to “Magnificent 7” – what’s in a name?

From “FAANG” to “MAMAA” to “Magnificent 7” – what’s in a name?

Unmasking the dividend opportunity

Unmasking the dividend opportunity

Who’s afraid of higher interest rates?

Who’s afraid of higher interest rates?

The future of mobility

The future of mobility

Investors turn to real estate for alternative income

Investors turn to real estate for alternative income

Federated Hermes SDG Engagement Equity: 2021 H1 Report

Federated Hermes SDG Engagement Equity: 2021 H1 Report

Animal spirits run wild; Franklin Templeton is taking credit; EM banking revolution; Not all luxury is equal; Death of search and the AI machine; George Soros on wins and much more.

Part of the Mark Allen Group.