The case for the sustained outperformance of emerging market equities often falls on deaf ears with distributors given their trajectory over the past decade, although there are compelling reasons why asset allocators should consider EM more seriously when it comes to portfolio selection.

For one thing, and perhaps the most obvious reason, EM stocks currently look attractive both on a historical and relative basis. According to data compiled by Mirae Asset Management, EM equities trade at 10.9x earnings and 1.4x book value, equivalent to an 8% and 4.3% discount versus their historical average.

Those figures also represent a 39.5% discount and 60.2% discount against the S&P 500 compared with the standard 10-year historical average discounts of 30% and 49.6%.

There are also several tailwinds supporting emerging markets currently, notably prospects for a weaker dollar (which tends to favour emerging markets because of lower import costs and increased FDI flows) and also the fact that a number of countries, most notably in Latin America, are further ahead than the Fed in grappling with inflation and have the scope to cut interest rates.

Advocates of EM stocks also point to the fact that the composition of most constituent countries has changed radically in the past two decades, where fixed exchange rates, high debt levels and political instability are now thankfully largely things of the past.

There is also the argument for adding EM stocks to a portfolio just because they tend to have low correlation to developed markets. This is especially the case in China, which is currently on a different economic cycle to the West.

Still, given the ongoing uncertainty due to the Russia-Ukraine war and China’s stuttering reemergence from lockdown, there are still several headwinds that currently leave the outlook for the second half of the year for EM equities uncertain.

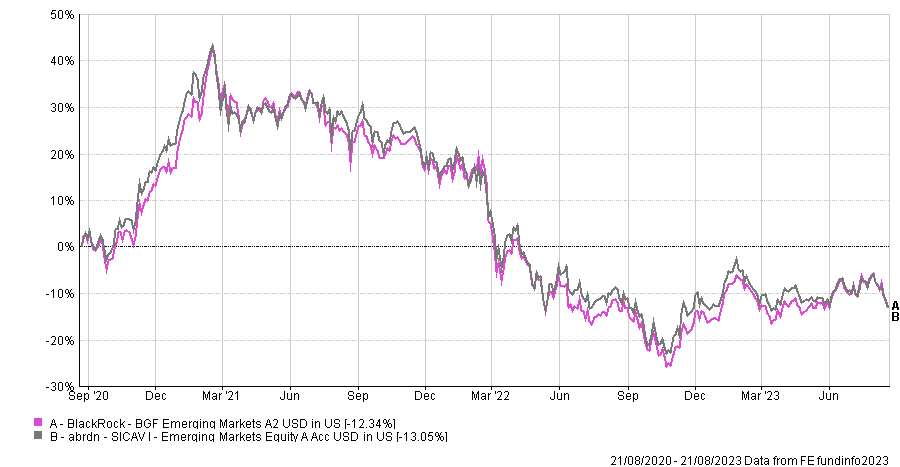

Against this background, Sam Lo, senior analyst of manager research at Morningstar, selected two emerging market funds for this week’s head to head. He chose the abrdn Emerging Markets Equity Fund and the BlackRock Global Funds – Emerging Markets Fund.

| Abrdn | BlackRock | |

| Size | $1.18bn | $2.64bn |

| Inception | 2003 | 1993 |

| Managers | Nick Robinson, Joanne Irvine, Devan Kaloo, Kristy Fong, Ng Xin Yao, Adam Montanaro, Fraser Harle | Gordon Fraser, Kevin Jia |

| Three-year cumulative return | -1.53% | -1.27% |

| Three-year annualised return | -4.43% | -4.35% |

| Three-year annualised alpha | -3.20 | -3.05 |

| Three-year annualised volatility | 18.80 | 19.21 |

| Three-year information ratio | -0.66 | -0.65 |

| Morningstar star rating | ** | **** |

| Morningstar analyst rating | Neutral | Neutral |

| FE Crown fund rating | ** | ** |

| OCF (retail share class) | 1.92% | 1.86% |

Investment approach

The abrdn fund is very much focused on quality, preferring companies with strong franchises and good balance sheet strength. This is illustrated by the higher return on equity and lower financial leverage among the stocks in the portfolio compared with the benchmark MSCI Emerging Markets index.

“The abrdn fund is much more of a purely bottom-up fundamental driven process; pretty much akin to other abrdn house strategies. The hallmark is the focus on quality. It has a very salient quality bias from a stylistic perspective,” said Lo.

Lo also notes that the fund has a slight growth bent to it as a result, although he distinguishes it from other growth funds.

“It’s not the brute force growth. It’s about the fundamental driven sustainable growth that we’re talking about here. It’s not a super growthy portfolio per se,” he said.

The portfolio is somewhat concentrated as the team tends to hold between 40 and 70 stocks at any given time; this is currently around 60. The portfolio turnover has averaged around 20% annually over the past five years.

One notable thing about the abrdn fund as well is that it is somewhat underweight China relative to the benchmark, although it has large stakes in Tencent and Alibaba Group Holding. It also has been reducing its weighting to tech stocks due to concerns about demand.

“The abrdn fund is much more of a purely bottom-up fundamental driven process; pretty much akin to other abrdn house strategies. The hallmark is the focus on quality.”

Sam lo, morningstar

It was forced by the Russia-Ukraine war to make large disposals of a number of Russian stocks including TCS Group and Sberbank. Other recent exits include Sea, Allegro, Kakao and Meituan.

Meanwhile, the BlackRock fund is a mixture of both top-down and bottom-up research. Gordon Fraser, the lead manager, leverages BlackRock’s risk analytics platform to determine how to position the portfolio in terms of country allocation and also stylistic orientation as well.

“The key things that Gordon Fraser looks for are the level of economic activities for the country, also the level of foreign exchange strengths and weaknesses, the yield levels and then market liquidity for various countries in the emerging market space. And afterwards he will also decide on whether to position the portfolio along the value, growth, momentum or quality dimensions,” said Lo.

Once Fraser has decided upon which countries and styles to choose from, his stock selection process looks at the companies’ competitive position and management quality with a preference for firms with solid free cash flow and upside earnings revision potential.

From the 300 ideas analysts put forward, Fraser chooses about 70 of them to construct a portfolio. Portfolio turnover is typically around 100% each year, reflecting the fund’s overall nimble approach.

The fund currently has an overweighting to Brazil because of Fraser’s favourable view of the country’s foreign exchange and fiscal position. He bought Ambev, the brewing company, in mid-2022.

Fund characteristics

Sector allocation:

| Abrdn | BlackRock | ||

| Financials | 25.6% | Financials | 23.77% |

| Information Technology | 23.7% | Information Technology | 22.65% |

| Consumer Discretionary | 13.5% | Consumer Discretionary | 13.85% |

| Consumer Staples | 8.5% | Consumer Staples | 8.39% |

| Materials | 7.2% | Healthcare | 7.15% |

| Communication Services | 6.7% | Materials | 6.39% |

| Industrials | 5.3% | Cash and/or Derivatives | 4.94% |

| Energy | 3% | Industrials | 4.38% |

| Other | 5% | Communication | 4% |

| Cash | 1.4% | Energy | 2.24% |

| Utilities | 1.65% | ||

| Real Estate | 0.59% |

Country allocation:

| Abrdn | Weighting | BlackRock | Weighting |

| China | 23.5% | China | 29.15% |

| India | 16.2% | India | 14.38% |

| Taiwan | 12.6% | Taiwan | 12.03% |

| Korea | 9.9% | Brazil | 11.13% |

| Brazil | 7.3% | Korea | 10.21% |

| Mexico | 6% | Cash and/or Derivatives | 4.94% |

| Hong Kong | 4.2% | Mexico | 2.62% |

| Indonesia | 3.8% | Thailand | 2.47% |

| Other | 14.6% | Indonesia | 2.41% |

| Cash | 1.8% | Kazakhstan | 1.62% |

Top five holdings:

| Abrdn | Weighting | BlackRock | Weighting |

| Taiwan Semiconductor Manufacturing Co | 9.1% | Taiwan Semiconductor Manufacturing Co | 7.43% |

| Samsung Electronics Co | 6.3% | Samsung Electronics Co | 7.19% |

| Tencent Holdings | 5.8% | Alibaba Group Holding | 5.08% |

| Housing Development Finance Corp | 4.2% | Axis Bank | 2.49% |

| Alibaba Group Holding | 4.1% | Bank Rakyat Indonesia | 2.41% |

Performance

Over a long-term horizon, the abrdn fund has fared quite well, although its performance has tended to be quite lumpy because of its quality bias, which only favours certain market conditions.

“If you look year from year, I wouldn’t call it a feast or famine situation, but the relative performance versus the market peers tends to jump around. If quality stocks are fashionable, it tends to do better; if not, vice versa,” said Lo.

Unsurprisingly, the fund has struggled since 2021 due to the rotation from growth stocks to value stocks, while its allocations to Hong Kong and Taiwan as well as within financials and materials also weighed on its results.

The big reason for the huge downturn in performance last year though was its prior allocation to Russia as the managers were forced to write down some of their holdings.

Similarly, the BlackRock fund also had a dismal year last year on the back of losses related to Russia. Lo noted that this was a bit of an aberration as Fraser has overall successfully navigated the market cycles, outperforming during difficult periods such as 2018 and 2021 as well as performing well during market rallies in 2019 and 2020.

“The headline objective is to try to navigate the market nimbly, to try to identify the inflection points and to position the portfolio accordingly as well as to try to outperform in all market conditions. Actually, they did a pretty good job until 2022,” said Lo.

Russia was a real kick in the teeth though and according to Morningstar research, accounted for more than half the underperformance during the year.

Lo noted that Fraser favoured Russian equities going into the first quarter of 2022 as he believed that they were cheap and were a good place to gain exposure to value stocks.

“Gordon Fraser invested in the oil names in Russia, which he was initially optimistic would work out and it didn’t. He did not invest in oil names in the Middle East, for example, and that created a double whammy effect for the fund,” said Lo.

Discrete calendar year performance

| Fund/Sector | YTD* | 2022 | 2021 | 2020 | 2019 |

| abrdn | -0.41% | -26.47% | -5.91% | 25.13% | 17.78% |

| BlackRock | 3.86% | -28.04% | -3.06% | 23.19% | 24.6% |

Manager review

The abrdn fund is led by its seven-member Global Emerging Markets portfolio construction group “pod”, which is a typical management structure for the fund manager.

Adam Montanaro is the newest member of the pod, who replaced Fiona Manning following her departure in August last year.

Despite adopting a collegiate approach, Lo identified Devan Kaloo, who serves as global emerging markets equities head, global head of equities and global head of public markets, as the key man among the seven.

Lo notes though that the rest of the pod are also veterans and boast an average 17 years of experience and 13 years of tenure at abrdn.

The pod is able to draw on the strengths of the wider 50-strong global emerging markets team, although there Lo notes that turnover has been high as they tend to lose about five team members per year.

“If we look at some of our other preferred teams, this number is in the mid-single digits. 10% is a bit high. But they’ve introduced some measures to reduce turnover, for example, they’ve revamped the compensation structure. Also, they have a larger component deferred to try to keep people,” he said.

Regarding BlackRock, Lo clearly holds Fraser in high regard, despite his relative youth for the position he occupies at the world’s largest asset manager.

Unusually, he started managing money at BlackRock through a hedge fund, which adds to his pedigree.

“If you talk with him, it’s obvious he knows the landscape pretty well and he’s very articulate in terms of explaining the investment rationale, be it on the top-down side, the macro part, and if you ask him about individual stocks, he has a pretty good grasp of those as well,” said Lo.

Much like with abrdn though, Lo notes that turnover has been a problem with the wider global emerging markets equity team, although most of this was deliberate as BlackRock cut the group’s headcount from 42 to 35.

Conclusion

Overall, Lo demurs when asked which one he prefers.

“For me, it’s hard to make this conclusion because I like them both. I’m not just giving you corporate speak. It’s reflected in the rating. If you ask me personally, I think they have different purposes in the portfolio. One is very nimble, very materially macro driven. I’m talking about the BlackRock fund. For the abrdn fund, it has a very salient quality focus, which it has stuck to over the years and it has delivered for investors over time as well. It really depends. I don’t have a relative preference between the two. I think they’re both good,” he said.