The FSA Spy market buzz – 11 April 2025

Lazard actively looks at Next Gen; Goldman Sachs loves active in small places; Janus Henderson is reassuring; Private equity’s overflowing war chest; Jevons Paradox; Hamlet’s wisdom and much more.

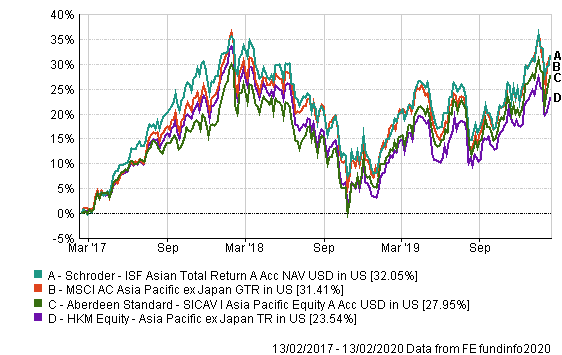

Given that both funds have a quality-bias, Daniels believes that the funds provide downside protection when markets are down.

“But you would expect them to generally lag during bull markets,” he said.

Discrete calendar performance (%)

| Fund / index / sector |

YTD 2020 |

2019 | 2018 | 2017 | 2016 | 2015 | 2014 |

| ASI |

0.89 |

18.67 | -11.2 | 32.45 | 3.76 | -14.92 |

2.11 |

| Schroders |

2.12 |

17.84 | -15.09 | 39.47 | 6.6 | -3.13 |

6.47 |

|

MSCI AC Asia Pacific ex-Japan |

0.72 | 19.48 | -13.68 | 37.32 | 7.06 | -9.12 |

3.09 |

|

HKM Equity – Asia Pacific ex-Japan |

-0.2 | 18.21 | -16.05 | 35.01 | 2.3 | -8.49 |

3.94 |

However, Daniels has more conviction that the Schroders fund will outperform the benchmark and its peers longer-term than the ASI fund.

“We have more conviction in the Schroders fund due to a higher process score.

“There are reasons for the ASI strategy to still outperform [the market], but given the changes in the process in recent years, we do not have the same level of conviction as before,” Daniels said.

In terms of volatility, Daniels expects that the ASI fund is more volatile than the Schroders fund, given that the Schroders option has the hedging feature to keep volatility lower.

Three-year annualised volatility

| Fund / Index |

Volatility |

Sharpe |

| ASI |

13.73 |

0.35 |

| Schroders |

12.8 |

0.45 |

| MSCI AC Asia Pacific ex-Japan |

13.78 |

|

| HKM Equity – Asia Pacific ex-Japan |

13.07 |

Healthcare’s innovation shifts into high gear

Healthcare’s innovation shifts into high gear

Accessing Asian 5G innovation: three key portfolio themes

Accessing Asian 5G innovation: three key portfolio themes

Investors turn to real estate for alternative income

Investors turn to real estate for alternative income

China bonds: plugging the yield gap

China bonds: plugging the yield gap

Smartphones on wheels

Smartphones on wheels

Ninety One: Finding opportunities in times of change

Ninety One: Finding opportunities in times of change

Appetite for thematic investments grows amid rates and inflation concerns

Appetite for thematic investments grows amid rates and inflation concerns

Fixed income – making ground in ESG as ETFs see rapid growth in AUM

Fixed income – making ground in ESG as ETFs see rapid growth in AUM

Tech WELLcovered | Work reimagined

Tech WELLcovered | Work reimagined

Dynamism is the name of the game for this global macro strategy

Dynamism is the name of the game for this global macro strategy

Lazard actively looks at Next Gen; Goldman Sachs loves active in small places; Janus Henderson is reassuring; Private equity’s overflowing war chest; Jevons Paradox; Hamlet’s wisdom and much more.

Part of the Mark Allen Group.