The Japanese stock market’s corporate governance reforms have been an important driver of its recent performance, but larger companies have benefited the most.

This is in part because Japanese large cap stocks have improved their corporate governance faster than their small cap counterparts.

But now regulators have turned their attention to small caps, urging them to manage toward higher returns and valuations, according to GMO’s Drew Edwards and Colin Bekemeyer.

The portfolio managers of the $1.3bn Usonian Japan Value Strategy argue that corporate governance pressure from Japanese policymakers will soon become a “disproportionate tailwind” for small caps.

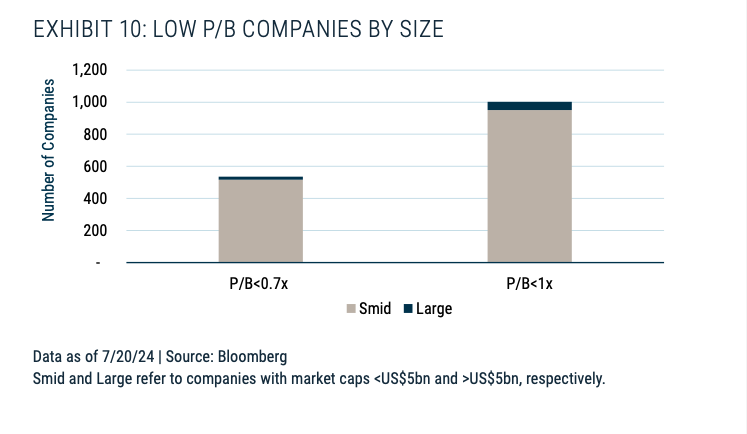

“The Tokyo Stock Exchange (TSE) efforts have lately focused on pressuring small caps to improve,” they said in a recent note, pointing to the latest policies on price-to-book ratios (P/B) and improving return on equity (ROE).

“The recent directive for companies to disclose plans to raise P/B ratios and ROE were directed especially at those companies with P/B ratios of less than 1x and ROEs of less than 8%, which are overwhelmingly represented by small and mid-caps.”

They said that Japanese small caps are likely to follow the prevailing corporate governance winds, but with a lag.

“There is an undeniable trend in corporate Japan for smaller companies to wait for larger companies to set new precedent before the small caps follow,” they explained.

“A clear example would be how corporate governance initiatives are adopted within group companies — say an automotive OEM and its suppliers.”

“The suppliers would be unlikely to make drastic reforms, especially unwinding holdings of the OEM, until the OEM had first adopted them.”

Japanese small caps have lagged their large cap counterparts over the past four years, with the MSCI Japan index is up 71.6% versus 56% from the MSCI Japan Smal Cap index.

Edwards and Bekemeyer attributed some of this to larger companies being more responsive to the TSE request to companies to disclose their plans to raise their ROE and share price.

Going forward however, in addition to corporate governance reforms, they believe small caps will benefit from other tailwinds such as a stronger yen, increasing real wages and fund flows.

They also pointed to the relative valuations of Japanese small caps as another favourable factor for the asset class.

“Although inferior EPS growth from 2022 was a drag on small cap performance, multiple compression is apparent from the time small caps began underperforming in 2018,” they said.

“As a result, Japanese small caps are trading at the largest discounts to their large cap peers over the past decade.”

As of data June 30, 2024, they note that the MSCI Japan Small Cap Index is trading on a P/E of 13.5x compared to the MSCI Japan Index P/E of 15.4x, the largest spread since 2010.

Additionally, they flagged small caps trade at a P/B of 1.1x, compared to large caps at 1.6x, the largest spread since 2007, and have a 0.5% higher dividend yield – levels unseen since 2001.

They said: “From a relative and absolute value perspective, small caps are looking extremely attractive. (At some point, valuation matters!)”

“While the yen may have been chiefly responsible for fundamental underperformance of small caps since 2021, valuation compression has been a bigger factor in their underperformance.”