It is still up for debate as to whether AI technology will translate into windfall profits for many of the “Magnificent Seven” technology firms, all of which have seen their valuations boosted by the hype surrounding artificial intelligence (AI).

Even industry behemoth Microsoft, despite its partnership with chatGPT’s creator OpenAI, does not anticipate meaningful revenue and profitability from its deployment of AI technology until 2024 or early 2025.

This means that when the market embeds certain expectations into earnings numbers, it leaves investors targeting AI as an investment theme vulnerable to potential disappointment, according to Karen Kharmandarian, chief investment officer at Thematics Asset Management.

“Beyond the attractiveness of the theme itself, how you turn that into an attractive investment proposition for clients is key – and where valuations come into play,” he told FSA.

“It’s not because you’re operating in an attractive theme that all companies are attractive from an investment perspective. Everything has a price.”

“For us, what matters is to make sure that the market doesn’t get ahead of itself and where valuations still make sense. So, valuation discipline is key.”

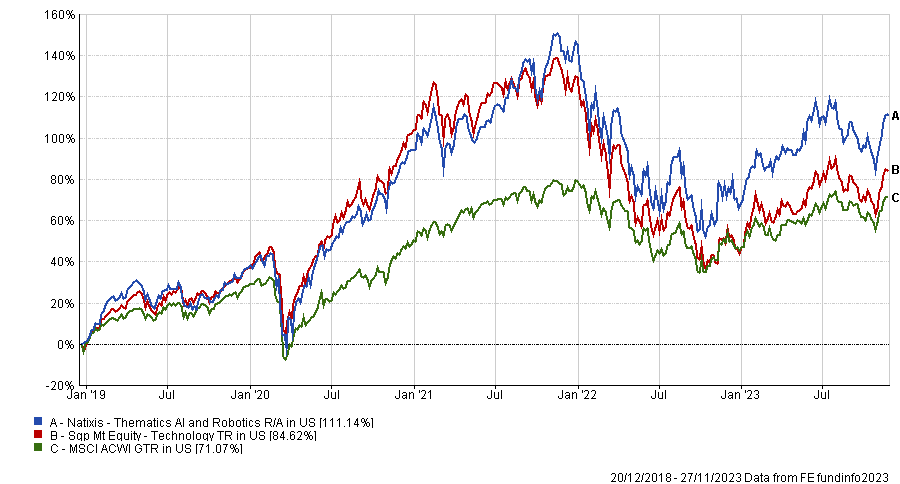

Kharmandarian is manager of the $713m Natixis Thematics AI and Robotics Fund, which is up 111.14% since it launched at the end of 2018, compared with 71.07% for the MSCI All Companies World Index over the same period.

The manager said the recent hype around AI reminds him of the dotcom bubble of the late 90s, because some AI related stocks have now reached valuations that are “unjustifiable” in his view.

“It’s going to disappoint many investors because you won’t see this AI benefit in the numbers, sometimes not even until 2024,” he said.

“I would be very selective in the companies you consider when you want to capitalise on this trend. It’s not always the most obvious companies that will benefit the most.”

While the market has largely priced in the extent to which chipmakers such as Nvidia and AMD are benefitting from the increased sales in semiconductors needed for AI computing, Kharmandarian is betting that other lesser-known stocks remain attractively valued relative to their opportunity set.

His strategy has a large position (at 3.9% of the portfolio) in Cadence Design Systems for example, which specialises in electronic design automation tools for Nvidia and AMD.

“Synopsis and Cadence together have 85% market share in electronic design automation, they command 80% gross margin, 35% to 40% operating margins, and are growing at double digits,” he said.

“Multiples aren’t cheap, but they’re not really crazy, given the growth that they have. On top of that, they have a technological moat and very strong IP, so they can defend their market share.”

He highlighted that by embedding generative AI into Cadence’s own tools they’ve improved the efficiency of engineers designing chips, which has led to the size of their contracts with Nvidia and AMD increasing by between 20% and 30%.

“You see the marginal impact that generative AI has on their profitability, which is something which is more of a concept in other companies,” he explained.

“It’s a new avenue for growth and for additional profitability for these companies that are already quite profitable intrinsically.”

Kharmandarian’s strategy is focused on providers of products and services related to AI, which is a focus that not all other AI funds share.

He said: “For example, if you invest in companies which are loosely related to AI, like Citigroup or Exxon Mobil because they use an AI algorithm either in their trading team or to hedge their commodity exposure.”

“Is it really critical for these companies in terms of their operating performance, profitability and stock price performance? Probably not.”

“When you say you provide an AI strategy, you need to have exposure to that, not a global equity product loosely related to AI.”