Each month we feature the allocation in one of the three portfolios offered by FE Advisory Asia: cautious, balanced and growth. Data is included to show how well the portfolio has done compared to the previous month and year-to-date so that readers can get a sense of performance.

Additionally, Luke Ng, senior VP of research at FE Advisory Asia, provides a concise analysis on macro events and their potential impact on the portfolio.

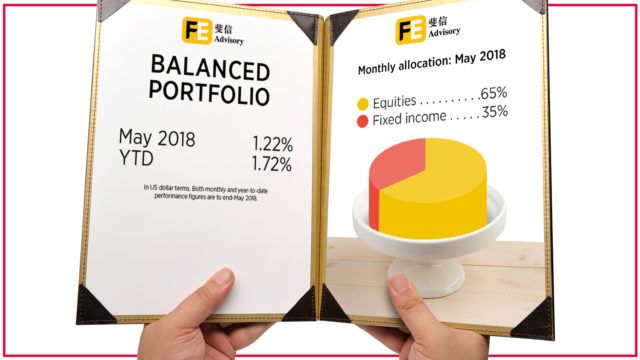

A breakdown of the Balanced portfolio at the end of May 2018.* Performance figures are in the menu image above.

Data: FE Advisory Asia

Luke Ng, FE Advisory Asia

How did the market perform in May?

May proved a mixed month for equity investors. Political events in Italy weighed on mainland European markets as the Five Star Movement and the anti-immigrant League party struggled to form a government that met with the approval of the country’s president, something that was finally achieved on 31 May. European banks and financials were hit particularly hard by the uncertainty. Economic news was mixed. Unemployment continued to fall, the first quarter growth slowed to 0.4% from 0.7% in the fourth quarter of 2017 and the PMI data hit an 18-month low.

The US was the strongest market during the month, returning about 2.5% in US dollar terms. It was helped by the relative strength of the US dollar and strong economic data showing unemployment at its lowest level since 2000, solid retail figures and an increased industrial production. This helped allay fears of a possible trade war from president Trump. Meanwhile, Japanese markets moved down amid the rhetoric from the US regarding imports, in particular, of cars, although it is in unclear how this might affect the status quo. Finally, emerging markets made a slight loss against the strong dollar.

The strengthening US dollar continues to make it tough on local currency-denominated emerging market debt, with some countries such as Argentina appearing more vulnerable than others. The political developments in Italy also drove its sovereign yield higher, with 10-years Italian yield increasing about 100 basis points during the month. As market uncertainties rise, safe assets have benefited. The 10-year US Treasury yield trended lower following an uptick last month. Overall, the Bloomberg Barclays Global Aggregate fell 0.76% in May.

How did the balanced portfolio perform?

Our balanced portfolio grew 1.22% in May in US dollar terms, faring better than both developed market and emerging market equities. The best performing holding in our portfolio was the JP Morgan Japan (Yen) Fund, which returned over 4%, despite Japanese equities recording a loss. In fact, all regional equity strategies we selected have performed well. Our US equities exposure, acquired through Legg Mason, as well as our Chinese, Asian and European exposures, all outperformed against their respective markets. Within our fixed income sleeve, our core exposure through our Fidelity holding, which invests into hard currency investment-grade bonds, also delivered positive returns.

How did you re-balance the balanced portfolio?

We have maintained our decision to slightly overweight the risk budget of our portfolio. While the US Federal Reserve has been gradually raising interest rates, efforts have also been made to shrink the inflated balance sheet. In addition, the fiscal stimulus, including the tax cut that was in place, is likely to drive US debt levels higher. Despite not moving in tandem with the US Fed, other major central banks are expected to follow the monetary-tightening footsteps of the US in the foreseeable future. With this in mind, we have taken the decision to reduce our duration risk by initiating a new strategy which focuses on short-duration, high-grade bonds. Corresponding with this move, we have trimmed our existing fixed income positions so that a similar allocation between equities and fixed income has been maintained relative to our previous re-balancing.

Within our equity sleeve, we have decided to sell our holding in US smaller companies and increase our exposure to US large cap, a strategy that is managed by Legg Mason. We believe that this will better benefit from the relative strength in US growth. We have also replaced our European equities holding with another European manager, as the former is no longer available for the Hong Kong public from June. Overall, Asia remains our favourite destination for equities due to the region’s sound structural growth opportunities and reasonable valuations.

FE Advisory Asia portfolio performance

| Jan 2018 |

Feb 2018 |

Mar 2018 |

Apr 2018 |

May 2018 |

YTD 2018 |

|

| Cautious | 1.43% | -1.58% | -0.14% | 0.06% | 0.39% | 0.13% |

| Balanced | 3.64% | -2.68% | -0.80% | 0.44% | 1.22% | 1.72% |

| Growth | 5.19% | -3.60% | -1.17% | 0.63% | 1.75% | 2.60% |