A widening US fiscal deficit, a weakening dollar and erratic policy decisions in Washington are forcing global investors to find alternatives to US assets.

Perhaps an unlikely option are Asia’s local currency bond markets, which typically offer insufficient yields to buffer sudden foreign exchange depreciation. But subdued inflation and higher real yields throughout most of the region combine to make a compelling case during a phase dramatically described as the “end of US exceptionalism”.

“For investors seeking diversification, income, and resilience, the case for Asia local currency bonds has rarely been stronger,” wrote Rong Ren Goh, portfolio manager, fixed income at Eastspring Singapore, in a recent paper.

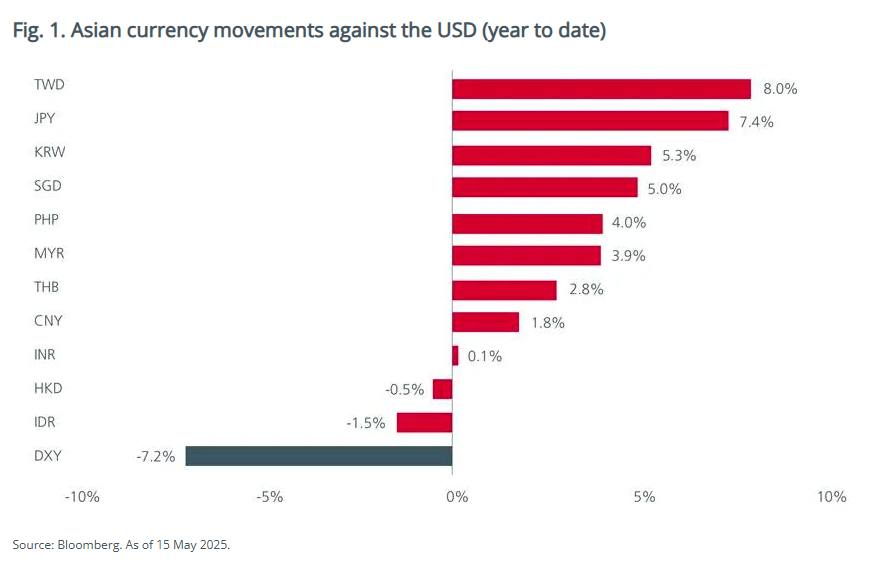

Most Asian currencies have appreciated against the dollar this year (see chart below) and are likely to strengthen further as funds continue to be repatriated out of the dollar as investors reassess the greenback’s dominance, according to Goh (main picture).

“This trend enhances the appeal of local currency bonds for foreign investors, as currency appreciation can amplify total returns,” he said. Moreover, as the dollar weakens so US assets become less appealing to non-dollar-based investors prompting them to diversify into assets with better risk-reward profiles.

Goh pointed out that Asia local currency bonds “exhibit low to moderate correlations to US Treasuries and to other major developed market peers”.

Most significantly, moderate inflation in the region gives Asian central banks room to manoeuvre

In 2025 to date, central banks in India, Indonesia, Korea, Singapore, China, Philippines and Thailand have already cut rates or eased monetary policy. More rate cuts are expected.

“With inflation under control and nominal yields still elevated, real yields in Asia are among the most attractive globally,” said Goh.

For example, real yields in Indonesia (2.9%), India (3.1%) and Philippines (4.7%) are currently higher than in the US (2.2%).

“This yield advantage is not just a function of policy rates. It reflects deeper structural strengths such as prudent fiscal management, improving credit fundamentals, and growing domestic investor bases,” Goh said.

Moreover, many of the markets also enjoy “idiosyncratic drivers such as strong domestic demand in Indonesia, Malaysia, India, South Korea and China. Meanwhile, Singapore, one of the few remaining AAA-rated government bond markets in the world, enjoys a safe haven status given its low volatility and high credit rating”.

The domestic currency bond markets have also grown, with an outstanding value of $1.34trn, comprising about 2,000 issues from more than 390 issuers. The size of the market reflects the region’s economic growth as well as regulatory reforms and increased foreign participation

Asia local currency bonds offer a “rare combination of yield, stability, and diversification,” concluded Goh.